This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For credit unions and smaller banks in North America, the challenge of how to compete with their bigger counterparts is a constant and pressing matter. These solutions provide great benefits once an account has been originated, however they lack effective tools for the acquisition stage of the lifecycle.

For credit unions and smaller banks in North America, the challenge of how to compete with their bigger counterparts is a constant and pressing matter. These solutions provide great benefits once an account has been originated, however they lack effective tools for the acquisition stage of the lifecycle.

On November 8, while at the Central Bank of Ireland, Federal Reserve Governor Lisa D. On November 8, the European Banking Authority issued draft guidelines defining how stablecoin issuers should structure their risk and management recovery plans concerning reserve assets. For more information, click here.

It marks the highest fine ever issued to a lender for what it deemed a breach of consumercredit rules. But more tellingly, the penalty related to the mistreatment of business and personal customers who fell behind on credit card and loan payments between 2014 and 2018 – well before many of us had even heard of COVID-19.

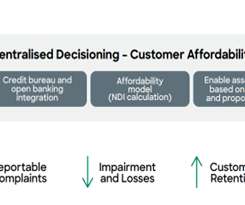

The fallout was felt around the world, with banks failing and stock markets crashing. By withdrawing the stress test, the Bank of England hopes to increase borrowing capacity for those who have, until now, been limited by it and struggled to get onto the property ladder. How FICO Can Help You Improve Affordability Assessments.

Over the past several years, we’ve helped lenders develop on-ramps to mainstream credit using alternative data for those seeking financial inclusion. Our research finds that alternative data sources that demonstrate a consumer’s ability to manage their finances are predictive of consumercredit risk.

In addition to traditional credit data, the UltraFICO Score reviews open banking or consumer permission data, such as how the consumer handles their finances which can be revealed by their checking and savings accounts. Sally holds a B.A. in statistics from the University of California at Berkeley.

During the past three decades, district courts from around the country have repeatedly held that collectors may properly inform consumers about adverse credit consequences resulting from their failure to pay. Credit Bureau of Georgia, 555 F. Financial Credit Corp. MKM Acquisitions, LLC , 241 F. See, e.g., Wright v.

On June 8, the board of governors for the Federal Reserve (the Fed), Consumer Financial Protection Bureau (CFPB), Federal Deposit Insurance Corporation (FDIC), National Credit Union Administration (NCUA), and the OCC requested public comment on proposed guidance addressing reconsiderations of value (ROV) for residential real estate transactions.

They say the chains tactics drained their bank accounts, ruined their credit and, in some cases, helped push them into bankruptcy. But for many patients, the hospital groups moves fall short of taking full responsibility for the years of real-world hardships its billing and collection practices have caused.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. On June 30, the CFPB released a blog post regarding trends of commercial reporting on consumercredit.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content