This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

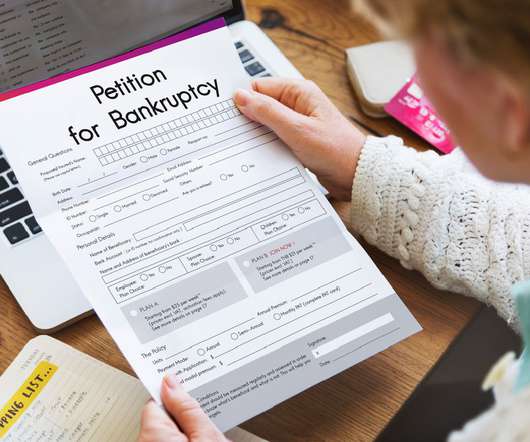

It’s no surprise then that thousands of individuals with student loan debt end up turning to bankruptcy for help. Though filing for bankruptcy may seem scary, there are many ways that it can help those drowning in debt get back on track. Will My Student Loans Be Discharged if I File for Chapter13Bankruptcy?

Filing for chapter13bankruptcy can seem like a daunting task, but it’s often the right move for those who are facing foreclosure, repossession, or have exorbitant debts. If you’re thinking of filing for chapter13bankruptcy, you may have questions regarding how it will impact your credit score.

Most people enter into bankruptcy because they are experiencing financial hardship. However, though a person can be struggling at the time they file, this does not mean it isn’t possible for their financial situation to greatly improve while they are still paying off their Chapter13bankruptcy plan.

Filing for Chapter 7 or Chapter13Bankruptcy: Chapter 7 will wipe out (discharge) your medical debt along with other unsecured debt, but you must have low enough income to pass the means test in order to qualify for it. Chapter13bankruptcy is discussed below.

People who have too much debt and can’t make payments often declare bankruptcy to help relieve them of their financial obligations. While people have many bankruptcy options, typically, people only file for Chapter 7 or Chapter13bankruptcy – two of the most commonly used debt relief solutions.

However, you can get rid of the financial and emotional pressure of being a debtor by filing for Chapter 7 or Chapter13bankruptcy. Both Chapters can help you start anew and discharge your debts, but they work differently. Chapter13 doesn’t work the same way. The main difference. Financial relief.

When you’re considering Chapter13bankruptcy, you’re also wondering how much of your debt you’d be obligated to pay back. Let’s take a look at a debtor’s obligations under Chapter13bankruptcy. What Is A Chapter13Bankruptcy Plan? What Is A Chapter13Bankruptcy Plan?

Chapter13bankruptcy can wipe out most kinds of debts and leave you with a much brighter financial picture. But Chapter13 can’t discharge all types of debt you’ve taken on. Some debts will remain after your bankruptcy, although you’ll be in a much better position to handle them. Section 523(a)(8).

If you’re struggling with overwhelming tax debts, you should consider all of your financial options , one of which is filing bankruptcyChapter13. With Chapter13, you can pool all of your debts, including some types of tax debts, into a three-to-five-year repayment plan. Does Bankruptcy Clear Tax Debt?

Bankruptcy is sometimes the best solution for those struggling with overwhelming debt. They fear that other people will find out about their bankruptcy and view them as financially irresponsible. There’s nothing wrong with filing for bankruptcy, but worrying about what other people will think is understandable. Trustee Program.

Filing for bankruptcy is an important step for many individuals looking to overcome debts. Your investment real estate’s outcome depends entirely on whether you file for Chapter 7 or Chapter13bankruptcy. Investment Real Estate in Chapter 7 Bankruptcy. Investment Real Estate in Chapter 7 Bankruptcy.

When filing Chapter 7 or Chapter13bankruptcy, it’s critical to understand the difference between consumer debt and non-consumer debt. If you’re considering filing Chapter 7 or Chapter13bankruptcy, consider enlisting the help of skilled bankruptcy attorneys. What is Consumer Debt?

Have you wondered what will happen to your credit report during and after your bankruptcy? When you’re working with a bankruptcy attorney at Sawin & Shea, one of the services we offer is reviewing your credit report. Your Credit Report as Part of Your Bankruptcy. We’re Making Sure Creditors Follow the Law.

Since 1991, the number of retirees filing for bankruptcy has tripled , with 12.2% of all bankruptcies being filed by people 65 and older. Unfortunately, all of this adds up to bankruptcy—something that is already scary to deal with as is but can be even more overwhelming and frightening for seniors.

Filing for Chapter13bankruptcy can provide much-needed relief if you are overwhelmed with debt and struggling to keep up with payments. Under Chapter13, you repay a portion or all of your debt, allowing you to keep assets like your home or car. What Is Chapter13Bankruptcy?

If you’re struggling with crippling debt this holiday season, filing for bankruptcy may be your best option for getting your finances back on track. Here’s what you need to know about getting through the holidays during bankruptcy. Those who are about to file for bankruptcy should also avoid accumulating substantial debt.

In 2012, the primary borrower filed for Chapter13bankruptcy protection, listing the defendant trusts as creditors for the student loans. The bankruptcy plan was confirmed, and the trusts filed proofs of claims which were not objected to by the plaintiffs. The ruling: U.S.

Bankruptcy is a smart, legal, and effective way to wipe out a mountain of old debts. There are many reasons why people resist bankruptcy, but some are based on fiction rather than facts. Maybe you’re avoiding bankruptcy merely because of a mistaken impression about it, so let’s clear things up. Assuming It Is Rarely Needed.

Many people hold misconceptions about filing for bankruptcy. Perhaps the most common misconception is the notion that filing for bankruptcy means that you lose all of your wealth and possessions. In this article, we discuss what exemptions you can expect and what you might lose when filing for bankruptcy.

The bankruptcy process involves looking at your assets. In a Chapter 7, or liquidation bankruptcy, some of your property may not be protected, and you could lose it. Most Chapter 7 filings are what we call a “no asset” case. Understanding Indiana Bankruptcy Exemptions. Property in Chapter 7 Bankruptcy.

Are you struggling with overwhelming debt and considering bankruptcy as a way out? If so, you may have heard of Chapter 7 and 13bankruptcy. Bankruptcy is a legal process that allows individuals or businesses to eliminate or reorganize their debt. This stops virtually all collection actions from creditors.

A bankruptcy can remain on your credit report for up to ten years from the filing date of Chapter 7 bankruptcy or up to seven years from the filing date of Chapter13bankruptcy. While bankruptcy may be a last resort, there are times where filing bankruptcy might make sense.

When you file for a Chapter13bankruptcy in Nashville, you likely will not receive a discharge until the completion of your repayment plan. Since Chapter13 lasts for three to five years, one or more financial circumstances may arise to interfere with your repayment plan. Is a hardship discharge an option?

Bankruptcy can be an overwhelming and challenging process. Understandably, this can make dealing with a bankruptcy seem impossible. However, as overwhelming as it all may seem, bankruptcy is often the best choice for many people, especially those who are struggling with crushing debt. How Does Reaffirmation of Debt Work?

Filing for Chapter13bankruptcy can be both challenging and stressful. One common question that filers have regarding the Chapter13 process involves income increases and whether they affect payment plans. For experienced Chapter13bankruptcy attorneys in Indiana , contact the offices of Sawin & Shea, LLC.

Filing your taxes and filing for bankruptcy are two things that can be confusing and challenging on their own. Filing your taxes after filing for bankruptcy is not as complicated as it may seem, and if you are still confused after doing some research, you can always reach out to a bankruptcy lawyer. Tax Debt and Bankruptcy.

When filing for bankruptcy, you can discharge certain types of personal loans, meaning that you’re no longer legally responsible for paying off the debt. If you’re considering filing for bankruptcy, you need to know what personal loans you can discharge and which filing method best suits your financial situation.

Many people assume that because they have filed bankruptcy, their credit is ruined, and they will not be able to qualify for any loans. Chapter 7 bankruptcy: In this type of bankruptcy, your non-exempt assets (if any) have been liquidated to pay off a percentage of your debts. This is not true. 30% Amounts owed.

There are two primary types of bankruptcies that a person might file when struggling to pay their debts: Chapter 7 and Chapter13. In a Chapter13bankruptcy , the debtor agrees to a payment plan instead of having their property taken to pay creditors. Devaluing assets.

It’s a smart choice to file for Chapter13bankruptcy. Your bankruptcy plan will allow you to catch up on payments and settle your debts while giving you a chance to keep your home treasured belongings. If you have a job but you’re struggling to make your payments every month, Chapter13 can help.

If you are thinking of filing for Chapter 7 or Chapter13bankruptcy, or if you have already filed, you may be concerned about how long the bankruptcy will stay on your credit report. Credit Scores: If you had a high credit score before going into bankruptcy, you will find that it will drop by 100 or 150 points.

An emergency bankruptcy is a bankruptcy filing method that expedites the filing process to stop creditors and bill collectors from seeking debts from borrowers. Individuals can file an emergency bankruptcy, also known as a skeleton bankruptcy, under Chapter 7 and Chapter13.

You might have heard that bankruptcy gives you a clean financial slate, but that’s not exactly accurate. For those experiencing serious financial distress, bankruptcy can be a way to eventually restart. Bankruptcy is a negative item that can show up on your report and impact your credit score for years.

Bankruptcy can be an effective solution for those who are struggling with debt, but it will limit their credit options and drag down their credit score temporarily. However, the rules are a bit different for bankruptcy. Technically, a Chapter13bankruptcy could also drag down a credit score for roughly a decade.

If you’re considering filing Chapter 7 or Chapter13bankruptcy, you need to be aware of the different components of the filing process, including the role of the bankruptcy trustee. Here’s what you need to know about the bankruptcy trustee and what they will investigate. What Is a Bankruptcy Trustee?

Though enacting the CARES Act helped, those dealing with hefty mortgage payments and considering bankruptcy, for example, weren’t entirely clear on their options. However, the situation was a bit more complicated for those already in bankruptcy or considering it. What is the CARES Act?

Choosing Between Chapter 7 and 13. Are you considering bankruptcy? Whether it’s Chapter 7 or 13, you have options. Bankruptcy is a challenging, life-altering experience. . Chapters 7 and 13 of the Bankruptcy Code – Awareness. Chapter 7 (Liquidation).

If you decide to file for bankruptcy, you must next decide which type of bankruptcy is right for you. Most individuals have three options, and understanding Chapter 11 vs. Chapter13 vs. Chapter 7 is important in making the right decision. What Is Chapter 11 Bankruptcy?

One issue that you may worry about when filing for bankruptcy is whether or not it will affect your employment. In the midst of a stressful financial time when you are having to accept the idea that your finances are changing, it is normal to believe that there is a stigma attached to bankruptcy. Bankruptcy Code (11 U.S.

Filing for bankruptcy is a process. As part of that process, the bankruptcy law requires that you get a certificate that evidences you did a pre-filing counseling session with an approved agency. Debt counseling (also called credit counseling) is required before you can declare bankruptcy. Learning personal budgeting education.

If you’re married and considering bankruptcy in Indiana, you’re probably wondering whether you can file alone and how this could impact your spouse. This is one of the most common questions for bankruptcy attorneys. Yes, you can file bankruptcy without your spouse. This is good news for Indiana residents.

What you will learn from reading this article: Facts about selling your home while going through bankruptcy. Details about Chapter 7 and Chapter13Bankruptcies and your house. You will need the advice of an experienced bankruptcy attorney as soon as possible! Chapter 7 Bankruptcy.

Bankruptcy will destroy your credit and remain on your credit report for up to 10 years. In many cases, you may also lose certain secured assets like homes and cars in a liquidation to pay your creditors some of what you owe. You must qualify to file for bankruptcy, and your income must meet an income means test. Key Takeaways.

No matter who you are, bankruptcy can be an incredibly stressful process—but it doesn’t have to be. One question we get a lot from many of our clients when they are filing for bankruptcy or have already filed is, “Can I convert Chapter13 to Chapter 7?” . Do I Qualify to Convert My Chapter13 to a Chapter 7?

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content