This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

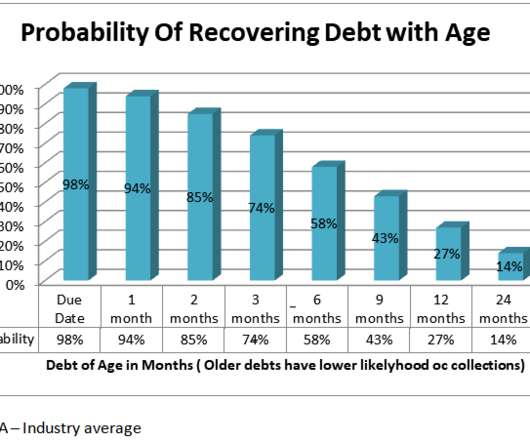

Companies will generally try to collect on their outstanding accounts internally before passing their most egregious cases on to an external debt collectionagency. Are collectionagencies effective enough to warrant their fees? Collectionagencies are experts in debt recovery. But how wise is this?

Companies will generally try to collect on their outstanding accounts internally before passing their most egregious cases on to an external debt collectionagency. Are collectionagencies effective enough to warrant their fees? Collectionagencies are experts in debt recovery. But how wise is this?

THE COMPLIANCE DIGEST IS SPONSORED BY: BK Filings Surge in 2024, Continuing Rebound from Historic Lows Total bankruptcy filings jumped 14.2% WHAT THIS MEANS, FROM LAURIE NELSON OF PAYMENT VISION: The surge in bankruptcy filings in 2024 presents both challenges and strategic opportunities.

You may feel as if no one is on your side, but you do have some protection from collectionagencies. The FTC makes sure that the FDCPA (Fair Debt Consumer Protection Act) is followed by collectionagencies. There are approximately 7,000 collectionagencies in the U.S.

Bankruptcy may appear to be a scary process, but it does not have to be. You may be able to apply for one of many different types of bankruptcy, each of which accomplishes various aims, depending on your specific situation. When collecting a debt from you, collectionagencies must adhere to federal and state rules.

Write a letter to the originalcreditor or collectionagency and ask them to remove the negative entry from your credit history as an act of goodwill. This is most effective when you’re trying to remove late payments, paid collections, or paid charge-offs. A goodwill letter is really easy to write.

Keep in mind that a creditor writing off your unpaid debt as a loss doesn’t mean you don’t owe the debt. Your creditor may sell your charged-off debt to a collectionagency for pennies on the dollar. The collectionagency may then attempt to collect the debt anew.

Due to this, the originalcreditors will reach out to you to obtain their due payments. However, if you do not pay, you could either assign the debt, sell the debt to a commercial debt collectionagency, or get sued for the commercial debt. Usually, you will have 90 to 120 days to pay.

When you hire Sawin & Shea for your bankruptcy, we give you a phone script that helps you handle collection calls. After you retain the firm, creditors must stop calling you once they have notice of our representation. How to Use Your Collection Call Script. A collection call script does two main things.

With the new rules, collectionagencies can contact consumers more frequently. They can place up to seven debt-collection phone calls per week (and under some circumstances even more), as well as send an unlimited number of text and email messages and private social media posts. But be warned, it’s 653 pages.

As a debtor, you have the following rights: Right to Privacy: Debt collectors are not allowed to share information about your debts with anyone else except your attorney or the originalcreditor. The FCA regulates debt collectionagencies and can take action if they’re found to be violating regulations.

Even when a company writes off your debt as a loss for its own accounting purposes, it still has the right to pursue collection. Unless you settle or file for certain types of bankruptcy —or the statute of limitations in your state has been reached—you’re still responsible for paying back the debt.

I consulted a bankruptcy attorney. He said filing bankruptcy should not be my first option since the amount is quite low. In California, is there a 3 or 4 years of limit by which the collectionagency can file lawsuit? 1, 2000, and it was later sent to collections, Jan. 1, 2000, is the original date of delinquency.

Finally, if the validation notice is being sent electronically, a statement explaining the consumer can dispute the debt or request originalcreditor information electronically. The Rule additionally requires the following additional prompt: “I want you to send me the name and address of the originalcreditor.”

If you have had an overdue bill move to collections, you may begin hearing from a company called ACS Inc. ACS Inc is a collectionagency that works with lenders and creditors to recover payments on defaulted loans or unpaid bills. A goodwill deletion will not work for you if you have not already paid ACS Inc for the debt.

Here’s one example of how a zombie might rise with help from a collectionagency. The original lender or collectionagency fails to collect within the statute of limitations. That collectionagency may report the debt as owed to the credit bureaus. You default on a debt.

Key Takeaways: Zombie debt arises based on collectionagencies. It may be possible to settle zombie debt with your originalcreditor. The Fair Debt Collection Practices Act (FDCPA) helps protect you from harassment. Collection activities are the most common causes of a zombie debt outbreak.

THE Fair Debt Collection Practices Act (FDCPA) is a federal law that was enacted in 1978 by the United States Congress to protect consumers from abusive debt collectors. Note, however, that the FDCPA applies only to third party collectors who collect debt for originalcreditors. Let’s use our beloved Pres.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content