This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Bankruptcy can be an overwhelming and challenging process. Understandably, this can make dealing with a bankruptcy seem impossible. However, as overwhelming as it all may seem, bankruptcy is often the best choice for many people, especially those who are struggling with crushing debt. Some criteria must be met.

Bankruptcy can be scary, but it’s important that you arm yourself with as much information as possible to navigate the process. In this article, we’ll walk you through some of the most commonly asked questions about bankruptcy, how it can affect your credit score, and how to get a bankruptcy removed. Skip to DIY Steps.

Although bankruptcy is often the only solution to get your finances back in order if you are struggling under mountains of debt, it does show up on your credit report for years, even after the bankruptcy has been discharged. You can, however, make your credit better post-filing.

There’s nothing fun about declaring bankruptcy, but those who emerge from it can be thankful for the opportunity to rebuild their personal finances without the burden of debt. Unfortunately, bankruptcy also does damage to your credit , making it difficult to get approved for credit cards and other lines of credit.

Bankruptcies, for instance, often remain on record for up to a decade. Tip: Liens and civil court judgments used to appear on credit reports, but creditbureaus no longer collect information about those types of public records. Bankruptcies are now the only public records included on credit reports.

Other Factors: Keeping a mix of different types of credit — a student loan, a couple credit cards, a car loan, and a mortgage, for example — will help your credit score some. Limiting new credit applications can help, too. But it won’t help your credit score. A Credit Report is Complex Yet Simple.

Approximately one third of consumers with a creditbureau file were contacted by at least one creditor or debt collector each year, according to a CFPB (Consumer Financial Protection Bureau) survey. Give information about a debt to a creditbureau without having informed you by phone or email first.

Remember that one of your rights is to an accurate credit report. If a collection agency reports a dead debt that can’t be collected to the creditbureau, you may be able to dispute it. Bankruptcy converts all debts covered under the plan into secure and nonsecure debts. When Judgments Turn Debt Into the Undead.

Your credit report begins with your basic details—your full name, your birth date, your current address, past addresses, and so forth. Credit reports should no longer include details about liens and judgments, but bankruptcies do still appear. Next, you’ll see an informational breakdown for each line of credit you have.

Convey a misleading sense of affiliation with or ownership of a creditbureau. The attorneys for Sawin & Shea have appeared on nearly 1,000 FDCPA cases and can help you possibly receive money before you file bankruptcy. Give the idea that you have broken the law or have done anything else wrong by not paying a debt.

When you hire Sawin & Shea for your bankruptcy, we give you a phone script that helps you handle collection calls. During your bankruptcy, bill collectors are required to follow certain rules for phone calls and other communications, and they are legally required to stop calling you. Your Bankruptcy Lawyer Looks Out for You.

Due to the fact that not all companies report to all three creditbureaus, there are often differences in the information retained by each creditbureau. Credit scoring companies like FICO rely primarily on the information contained in the credit report, which can result in a different credit score for each creditbureau.

Rent Bureau , now owned by the creditbureau Experian, electronically compiles rental data from property management companies and individual landlords. Rental agencies and alternative credit providers use the data to screen applicants and establish consumer credit scores.

Depending on the type of public record, they can end up on your credit report for as long as ten years. The court will create a public record for bankruptcies, foreclosure, or failure to pay taxes. Certain kinds of public records won’t end up on your credit report, such as divorce or probate records. Bankruptcies.

Even though all these companies review credit to determine deposit requirements, they do not report on-time payments to the creditbureau because it is not considered debt. To address these disparities, some lenders now accept credit scores like the FICO XD , which uses alternative data.

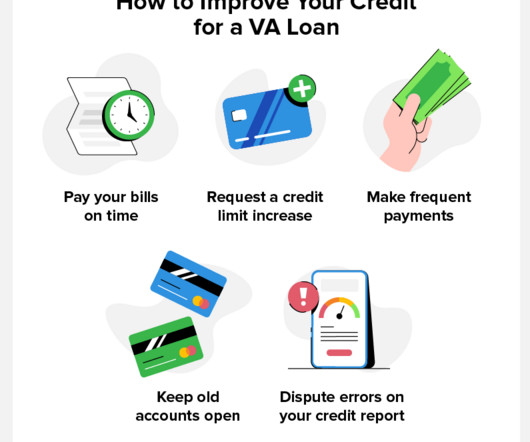

Table of Contents: What Is the Minimum Credit Score for a VA Loan? Compensating Factors Your Lender May Take Into Account Other VA Loan Requirements How to Get a VA Loan After Bankruptcy or Foreclosure Who Qualifies for a VA Loan? Here’s an overview of how to get a loan after foreclosure or bankruptcy.

If you notice any errors, you can dispute them with the creditbureau. 3: Dispute Inaccurate Repossessions Disputing inaccurate repossessions is the best way to ensure that the information in your credit report is accurate and gives lenders a clear picture of your current financial situation. Wait for the bureau to investigate.

Not only are data breaches costly because of the notification provisions, including providing creditbureau monitoring, it can be difficult for a company to survive after a breach. It is not unusual for a company to file bankruptcy after a data breach.

While it doesn’t usually affect your credit score , you may want to correct information with the creditbureau if an employer you’ve never worked for is listed. Phone Numbers: You’ll see phone numbers associated with your credit accounts. That can include any of the following: Bankruptcy. Foreclosure.

Easy pre-qualification process which does not affect your credit score Choice of card image at no extra charge Less than perfect credit is okay, even with a prior bankruptcy! The Fair Credit Reporting Act also protects your right to accurate information in your credit file. Snapshot of Card Features.

You can get a free credit report each year from the three main creditbureaus—Equifax, Experian, and TransUnion—by going to www.annualcreditreport.com. Dispute negative items : If you notice any mistakes on your credit report, complain to the relevant creditbureau. Bankruptcy. Debt settlement.

How Can You Clean Your Credit Report Fast? One of the fastest ways to clean up your credit report is to challenge the accuracy of information. If you’re able to prove something is inaccurate, the creditbureau must take action to remove or correct it. How Do You Get Things Removed from Your Credit Report?

Here are a few trends that may impact how creditbureaus determine your credit score in the near future: Buy Now, Pay Later (BNPL): Also called point-of-sale (POS) installment loans, BNPL plans allow you to divide purchases into lower monthly payments, often without interest.

Check with Your Credit Card Issuer or Bank Some credit card issuers and banks will provide free credit scores to their customers. Be sure to read the terms and conditions carefully, as some creditbureaus may offer a free trial but then charge a fee if you do not cancel within a certain time frame.

Balance and credit limit errors may artificially inflate your utilization ratio, making it more difficult to qualify for loans and credit cards. Errors in data management: If a creditbureau corrects some of the information on your account, there’s nothing to prevent a creditor from making the mistake a second time.

However, it could take several years to fully restore your credit. Bad credit issues, such as late or missed payments and defaults, can remain on your credit for up to 7 years in most cases. However, bankruptcies can remain on your account for up to 10 years. Ultimately, these negative items can affect your credit score.

However, skipping a payment before getting an approved forbearance will result in a delinquency reported to the creditbureau. You increased credit card spending in a manner not typical of your prior spending history. In most cases, lenders continue to report the account as current.

Contacting the company by phone is the only way to get help, which typically includes the following: waived payments, interest, and penalties, along with suspended creditbureau reporting. In some cases, the company could extend the credit line. However, aid is not automatic or uniform. About Titan Consulting Group.

According to the Federal Reserve’s Consumer Credit report, 43.5 Not only can you not declare bankruptcy on many forms of student loan debt, but it can also harm your credit. The creditbureau Experian® shows the average student loan balance increased 91 percent between 2009 and 2022. As of September 2022, the U.S.

A good credit repair agency should start out by determining exactly which items they can help you with. Doing this typically requires a copy of a credit report from each creditbureau — TransUnion, Experian, and Equifax. The company should identify the problems causing the most damage to your score.

From there, you should file a dispute with the creditbureau(s). The Fair Credit Reporting Act requires bureaus to handle disputes with a 30-day investigation. A credit repair company is also a great asset if you’re facing any of the following: Bankruptcy. Charge offs. Debt collections. Foreclosure.

Dealing with lenders and creditbureau representatives regarding fraudulent inquiries can be a hassle. If you don’t have the time or energy to devote to disputing the entry, you may want to turn to a credit repair company. These businesses are adept at tackling big and small credit issues, including: Bankruptcy.

You’ll even get pointers for improving your credit , along with tailored offers based on your credit profile. Confronting lenders and creditbureau representatives about suspected fraud and reporting errors can be daunting. These industry experts can help you with more trying credit problems, too, such as: Bankruptcy.

Both RentGrow and the creditbureaus should help you get the inaccurate entry off your report. Hard credit inquiries can impact any one of your credit scores, or all three of them. As such, you need to dispute the inquiry with every creditbureau that is displaying the entry from RentGrow on their reports.

The Fair Credit Reporting Act protects you from inaccurate or fraudulent reporting issues, allowing you to dispute questionable entries on your report. When you file a dispute with a creditbureau, they have 30 days to investigate your claim. Bankruptcy. Charge offs. Collections-level debt. Foreclosure. Repossession.

The Fair Credit Reporting Act protects you from inaccurate or fraudulent reporting issues, allowing you to dispute questionable entries on your report. When you file a dispute with a creditbureau, they have 30 days to investigate your claim. Bankruptcy. Charge offs. Collections-level debt. Foreclosure. Repossession.

A Consumer Pulse study conducted by the creditbureau found that more than half of Americans expressed confidence about their financial health in 2023. Michele Raneri, vice president of research and consulting at TransUnion, said that despite mounting financial pressures, there’s optimism among consumers.

c) Falsely representing that they work for a creditbureau. j) Giving false credit info about you to anyone, including a creditbureau. Lawrence Bautista Yang specializes in Bankruptcy, Business, Real Estate and Civil Litigation and has successfully represented more than five thousand clients in California.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content