This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Bankruptcy is a great option for many, as it can help people get back on track with their finances. Plus, these bankruptcy options also provide protection from creditors. Here are some expert tips for rebuilding your credit and finding the best credit cards after bankruptcy. You may have to start small, with a secured card.

Though bankruptcy is often one of the best ways to get out of debt, it can damage your credit score after filing. There is life after bankruptcy, and you can open new lines of credit and take out loans again after you get back on your feet. Improving Your Credit Score After Bankruptcy. Keep up with payments.

Following bankruptcy, managing credit card usage requires a strategic approach to rebuilding financial stability and creditworthiness. Some tips to help you navigate credit card use after you file for bankruptcy can be found here. Quality should take precedence over quantity when it comes to credit cards post-bankruptcy.

Incorrect Personal Information Lender Inquiries You Don’t Recognize Accounts You Never Opened Credit Utilization Goes Up Credit Score Goes Up or Down Unexpectedly Public Records You Don’t Recognize. Warning Sign 2: Lender Inquiries You Don’t Recognize. Negative public records can substantially impact your creditworthiness.

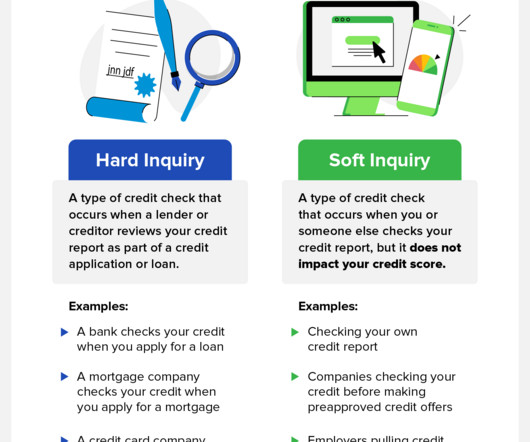

Your credit score is an important aspect of your financial health and is oftentimes used by lenders, landlords, and even employers to determine your creditworthiness. Hard inquiries , also known as hard pulls, are typically made by lenders and other financial institutions and can harm your credit score. What’s a Hard Inquiry?

Bankruptcy may appear to be a scary process, but it does not have to be. You may be able to apply for one of many different types of bankruptcy, each of which accomplishes various aims, depending on your specific situation. The federal Fair Debt Collection Practices Act (FDCPA) does not apply to the actual lender.

And now we can add mortgage lenderbankruptcies — and the rise (and fall) of “non-qualified mortgages” — to the factors aggravating an already uncertain market. They’ve previously been touted as an option for creditworthy borrowers who can’t otherwise qualify for traditional mortgage loan programs.

As lenders acknowledge the need for alternative credit data, companies are finding innovative ways to track non-traditional payments without requiring consumers to borrow money or use a credit card. What lenders use alternative credit data to grant credit? Can alternative credit data be used to improve my credit score?

Use the same formula that lenders rely on when evaluating a loan application. The result is a percentage that determines your creditworthiness – in short, if lenders believe you’ll be able to repay the loan. Start by determining how your debt compares to your income. You could afford to shoulder more liability.

Mortgage lenders use various different FICO score iterations to make lending decisions—specifically FICO 2, FICO 4 and FICO 5 scores. It’ll show you the credit score that auto, home, credit card lenders see—and more. . Bankruptcies are shown, but judgments and tax liens are no longer listed. See Your Full Credit Reports.

If you have a co-signer associated with your debt or if you are a co-signer, you need to be aware of how financial liability works and what happens when the primary debtor declares bankruptcy. Fortunately, in this blog, we’ll unpack cosigner responsibilities when it comes to bankruptcy and debt.

If you’re not missing or making late payments anymore, your creditworthiness will increase. Find a lender : Thoroughly research personal loan lenders and offers from credit unions. In this case, you can look to alternative types of debt relief, such as debt settlement or bankruptcy. Bankruptcy. Debt settlement.

Credit.com’s free credit report card tool can help you better understand your current creditworthiness and which factors you need to work on to help you improve your standing. While individual lenders may care that a credit counseling agency is repaying your accounts, FICO does not.

They let lenders access your complete credit report, which they use to assess your creditworthiness. While some lenders only look at one report, others may access all of them to get a clearer picture of your credit history. Some of the issues they’re well-versed in include: Bankruptcy. Charge offs. Collections.

Before agreeing to cosign, consider factors like the borrower’s creditworthiness and your financial situation. Lower interest rates: Lenders may offer a lower interest rate on loans with a cosigner. This could include disputing errors on your credit report or exploring legal options like a lawsuit or bankruptcy.

Failures are currently being forecast at around 900,000 businesses, with a wave of bankruptcies now predicted by the end of April, warns the Centre for Economic Performance (CEP) and the Alliance for Full Employment (AFFE). Other high-street lenders are looking at similar initiatives. Phased Changes.

This blog covers: The current landscape of consumer lending The primary advantages of LOS How can lenders meet shifting market demands The Consumer Lending Landscape The consumer lending market has shifted significantly with the rise of fintech platforms and marketplace lending.

Lenders can access reportswith consumer permissionto evaluate someone for a loan or other financial opportunity. If you have negative items on your credit history, the lender may not approve you for credit or might do so at a higher interest rate. Tradelines include credit cards, bank accounts, mortgage lenders, and other creditors.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content