This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

THE COMPLIANCE DIGEST IS SPONSORED BY: BK Filings Surge in 2024, Continuing Rebound from Historic Lows Total bankruptcy filings jumped 14.2% WHAT THIS MEANS, FROM LAURIE NELSON OF PAYMENT VISION: The surge in bankruptcy filings in 2024 presents both challenges and strategic opportunities. Carrington Mortg. 4th 370 (4th Cir.

Debt Relief Attorney Serving Colorado. Bankruptcy may appear to be a scary process, but it does not have to be. Dray Legal Office’s attorneys will endeavor to help you obtain a fresh start by eliminating debt and reorganizing your finances. In this article we will answer the question: What can debtcollectors do to you?

Whether you have missed a single payment somewhere along the line or are delinquent on several payments, the last thing you want is to be harassed by debtcollectors. The FDCPA applies only to debtcollectors (the third-party collection agencies), not to the original lender. Use abusive or obscene language.

Dealing with credit card debt is challenging, let alone facing a debt lawsuit.If the creditor wins the lawsuit, you may face serious financial repercussions. If you find yourself being sued by a debtcollector, you may wonder how to get a credit card lawsuit dismissed. An estimated 2.5

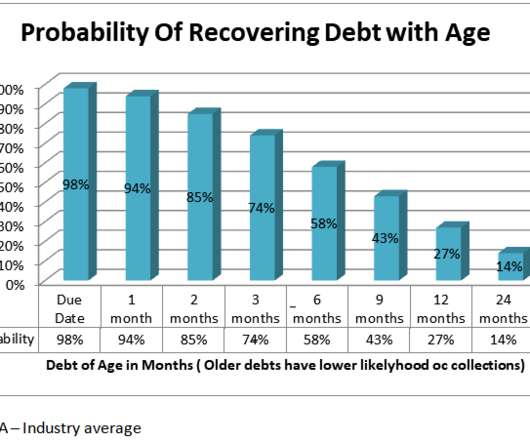

It falls to 74% collectible at three months, and by six months, only 58% of debts remain viable. At a year, there’s only a 27% chance of recovering the debt. These percentages assume skilled debtcollectors with modern collection tools at their disposal, like those found at agencies.

It falls to 74% collectible at three months, and by six months, only 58% of debts remain viable. At a year, there’s only a 27% chance of recovering the debt. These percentages assume skilled debtcollectors with modern collection tools at their disposal, like those found at agencies.

Experiencing a constant barrage of calls from debtcollectors can be overwhelming, to say the least. Many wonder, “How many times can a debtcollector call me in one day?” Harassment or Abuse: The FDCPA prohibits debtcollectors from using abusive, unfair, or deceptive practices. or after 9 p.m.,

Write a letter to the originalcreditor or collection agency and ask them to remove the negative entry from your credit history as an act of goodwill. Developing these good habits will help a lot, but let’s be clear: a major negative entry like bankruptcy, foreclosure, or repossession on your credit file will cause bad credit.

This is the federal law that protects consumers from being harassed by debtcollectors. As we’ve mentioned before, the law applies only to consumer debt, not businesses. The law also only applies to outside debtcollectors, not companies who are owed the money for product or services they provided.

Your creditor may sell your charged-off debt to a collection agency for pennies on the dollar. The collection agency may then attempt to collect the debt anew. Pro tip: Even if a debt has been charged off, consider contacting the originalcreditor to negotiate a settlement.

Under the final rule, debtcollectors must provide the consumer with certain information relating to the debt and the consumer’s rights (Validation Notice). consumer response information, such as prepared statements and prompts that the consumer may use to take certain actions, including disputing the debt.

Communications in Connection with Debt Collection) to allow debtcollectors to communicate with the deceased consumer’s spouse, parent (if the consumer is a minor), legal guardian, executor or administrator, and confirmed successor in interest (as defined Regulation X). Section 1006.2(c) This definition dovetails with 1006.6

Furnishers are banks, debtcollectors, and others that report the information that shows up on your credit report. Re-aging can occur when a debt is sold to a third-party collector and the start date on the debt’s clock is muddied and appears to be a new debt. Bankruptcies can remain for up to 10 years.

That’s what Credit.com reader Dave, who says he can’t afford to pay off the old debts he owes, asks: My credit card debt is roughly $12,000. I consulted a bankruptcy attorney. He said filing bankruptcy should not be my first option since the amount is quite low. And the collectors have stopped calling.

This leaves businesses struggling to maintain revenue while debt continues to pile up. There are 35 major bankruptcies in 2019 so far, and over two-thirds happened in retail. trillion worth of debt. When faced with mounting debt, it’s inevitable that someone will come to collect. Handling DebtCollectors.

A debtcollector is free to collect during the thirty-day period as long as it does not overshadow or contradict the consumer’s thirty-day rights. But what if the debtcollector initiates a process that is not readily stopped if the consumer makes a timely request for validation? In Scott v. Trott Law, P.C. ,

Once your debt is charged off, your creditor will send a negative report to one or more of the credit reporting agencies. It may also attempt to collect on the debt through its own collection department, by sending your account to a third-party debtcollector, or by selling the debt to a debt buyer.

Most of these complaints are in regard to violations of the Fair Debt Collection Practices Act (FDCPA). If you are having issues with ACS Inc or another debtcollector, you may consider filing a complaint against them as well. A goodwill deletion will not work for you if you have not already paid ACS Inc for the debt.

That collection agency may report the debt as owed to the credit bureaus. Suddenly, the debt reappears on your credit report, except now it’s a zombie debt. Zombie Debts and Judgments. First, judgments provide the creditor with the legal means to collect via actions such as wage garnishments or bank account liens.

Dealing with zombie debt can be extremely complicated as debtcollectors may repeatedly contact you about an account that belonged to you years ago. Much like the characters in a post-apocalyptic story, it’s possible to overcome zombie debt with the right know-how. How Does Zombie Debt Work?

THE Fair Debt Collection Practices Act (FDCPA) is a federal law that was enacted in 1978 by the United States Congress to protect consumers from abusive debtcollectors. Note, however, that the FDCPA applies only to third party collectors who collect debt for originalcreditors. Trump $45,000.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content