This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When lenders take life insurance policies as collateral for loans, they need to be aware of what needs to occur to place a claim in the event their borrower dies. Therefore, it is critical for lenders to confirm that no prior assignment exists on life insurance collateral prior to taking the collateral on as security for a loan.

Business loans that don’t require collateral come in a variety of forms, including online loans, bank loans, Small Business Administration loans, invoice financing, equipment financing and inventory financing. The article How to Get a Business Loan Without Collateral originally appeared on NerdWallet. That’s the good news.

Lenders should be cognizant about what expenses are classified by the SBA as recoverable or non-recoverable. Recoverable Expenses” are defined as SBA approved, necessary, reasonable, and customary costs incurred to collect and enforce the terms of the Loan Documents, or to preserve or dispose of collateral. See SOP 50 51 3.

Lenders are responsible for servicing and liquidating all of the 7(a) loans in their portfolio. Lenders and CDC’s must be cognizant about their responsibilities and authority in servicing and liquidating SBA loans because failure to do so properly may lead to formal enforcement actions by the SBA Office of Credit Risk Management.

When a borrower applies for a loan, most lenders require the borrower to pledge an asset as security for the repayment of the loan, i.e. collateral. In the event the borrower defaults, usually by failing to make loan payments, a secured creditor has a right to take possession of the collateral. 679.609, Fla. 2d 1020, 1024 (Fla.

Lenders must pay particular attention to subordinate liens and encumbrances prior to initiating any foreclosure action. Lenders can discover whether subordinate liens and encumbrances exist on a property by performing a title examination prior to initiating foreclosure. Subordinate Liens. York, 903 So. 2d 981, 983 (Fla. 2d DCA 2005).

If a borrower defaults on a SBA loan, the lender or CDC must assess the environmental risk of contamination before conducting any liquidation action that could result in a loss, or otherwise increase the risk of loss, due to the actual or alleged presence of contamination. What Are Environmental Risks? SOP 50 10 5(E), Appendix 2.

When a small business association (“SBA”) loan is converted to liquidation status, the lender must begin liquidating the collateral. Lenders must liquidate all personal property that has a Recoverable Value over $5,000. In Florida, the lender can choose from the following methods: UCC Sale. See SOP 50 57.

Lenders use it to assess how likely you are to pay them back. If you have a low score, the lender might consider you high-risk, charge you higher interest rates, or even deny the loan. A secured loan requires collateral (like a car or house) as a guarantee, while an unsecured loan does not but typically has higher interest rates.

Site visits allow lenders and CDCs to gain a first-hand impression of the borrower’s business operations, evaluate risks, and inventory the collateral. Frequent site visits help lenders and CDCs make prudent lending decisions by keeping them up-to-date with the condition of the collateral and the borrower’s business operations.

This may be troublesome for lenders because the property may then be sold for taxes, which will eliminate the lender’s mortgage lien. This may leave some lenders wondering how it can protect their mortgage interests, if the borrower is delinquent in paying its property taxes. How Do Property Taxes Result in Loss of Collateral?

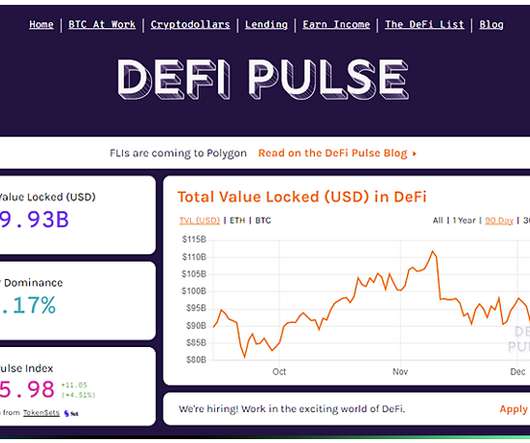

DeFi decreases the barrier of entry to financial products and services for people who are unbanked from traditional financial services because of significant reasons, such as lack of credit history, weak banking infrastructure, or limited banking hours. The statistics of the World Bank Global Findex Report, currently 1.7

When a small business association (“SBA”) loan is converted to liquidation status, the lender must begin liquidating the collateral. If the collateral is real property, the lender must liquidate all parcels of real property that has a Recoverable Value over $10,000. Is the Recoverable Value of the Property Over $10,000?

When underwriting and servicing SBA loans, it is important for lenders and CDCs to ensure appropriate insurance coverages are in place to protect the collateral. As a condition for the loan, the SBA requires borrowers to maintain hazard insurance on all pledged collateral. 13 CFR § 120.160 ; SOP 50 10 5(K).

If a borrower is experiencing difficulties making payments on their SBA loan, they may seek relief with the lender or CDC by requesting a loan modification or deferment. Lenders have unilateral authority, however, to issue a one-time deferment that does not exceed a continuous period of three (3) monthly installments.

Unsecured loans are loans that don’t have collateral. If you fail to repay an unsecured personal loan, the lender cannot repossess your assets. Common unsecured loans include: Bank loans with no collateral. Personal loans from lenders that you know, such as acquaintances, co-workers, employers, friends, and family.

Online lenders make it easy to compare rates and terms and find the right online personal loan for your situation. That is, the lender advances you money that you pay back with interest over a predetermined period of time. This often allows digital lenders to streamline the applications. Fast Approval.

Most lenders are likely familiar with these servicing actions, and many lenders have their own requirements and procedures for handling each of them. One of the most common reasons a borrower may request an assumption is because the borrower wants to sell their business, along with all of the collateral, to some other entity.

In the event a borrower is seriously delinquent on making payments under a SBA loan, or the SBA loan is classified in liquidation status, lenders and CDCs must develop a prudent and commercially reasonable strategy to maximize their recovery on the loan. 60 calendar days), the lender/CDC must move forward with liquidating the collateral.

While a “C” average may feel middle-of-the-road on an academic scale, nailing the five C’s of credit is the key to getting business funding from banks and other financial institutions. Jackie Zimmermann is a writer at NerdWallet. Email: articles@nerdwallet.com.

A secured card is one where you put down a certain amount of money with the bank to guarantee your repayment. You are no risk to the bank because they already have your money. You will need pay stubs, bank statements, and tax returns to prove this to your potential lender. Prequalify through several lenders.

However, lenders often wonder where they should file the foreclosure action if the loan is secured by mortgaged land situated in different counties. Intercredit Bank, N.A. , Flagship Cmty Bank , 96 So. allows the lender to bring a single foreclosure action on all mortgages in just one county. 2d 863, 864 (Fla.

When a SBA loan is in liquidation status, lenders and authorized CDC liquidators are required to perform “Prudent Liquidation.” When Prudent Liquidation is complete, it’s time for the lender or authorized CDC liquidator to submit a wrap-up report to the SBA and have the loan charged-off. 120.535(b). 120.535(b). SOP 50 55.

In Florida, lenders may find themselves foreclosing on real property with a mobile home attached to the land. On the other hand, if the mobile home is not retired and the lender has a perfected lien on the mobile home, the lender must use replevin in addition to the foreclosure. Is the Mobile Home Retired?

If the borrower is unable to pay the full amount owed on an SBA loan after all of the collateral has been liquidated, the borrower may submit an “offer in compromise.” All borrowers must submit their own offer in compromise to the lender or CDC. If there are any discrepancies, the lender must investigate them.

Every month, you face a mound of credit card and bank statements (or your inbox fills up with them, and you have to write a separate check (or perform an individual internet transfer) for each of them. Every time you apply for credit, your lender performs a hard inquiry on your credit report. Don’t apply for multiple accounts at once.

Lenders need to be aware that borrowers and other lienholders can bring an action or proceeding to set aside, invalidate, or challenge the validity of a final judgment of foreclosure of a mortgage, even after the foreclosure sale. The property was acquired by a “person affiliated with” the foreclosing lender or the borrower.

As discussed in parts 1-4 of this series, lenders have several options prior to instituting a commercial foreclosure action. Additionally, as briefly discussed in part 5 of this series, during the foreclosure action, lenders have options to try to preserve the value of the underlying collateral and to minimize further losses.

Some examples of consumer debt include: Personal credit card debt Store financing Home mortgages Rental furniture Personal lines of credit and bank loans Vehicle leases, which can include cars, planes, boats, and more Cosmetic-based medical debt Family or personal legal fees.

This series has provided a high-level overview of various options and considerations available to lenders during the current uncertainty surrounding lending in the hospitality industry. The first-half of this series evaluated considerations for lenders faced with borrowers who were unable to meet their mortgage and loan obligations.

A personal loan is money borrowed from a lender that can be used for almost any purpose, from debt consolidation to home improvement projects. Most people don’t have $5,000+ sitting in their bank accounts—that’s where personal loans come in. This can range anywhere from months to years, depending on the lender and your needs.

A signature loan is a fixed-rate, unsecured personal loan offered by an online lender, bank or credit union. It’s called a signature loan because it’s secured by your signature instead of collateral, like a car or an investment account. Getting approved for a signature loan will likely depend on your creditworthiness.

Sometimes, foreclosure of a commercial property is the only option available to lenders and servicers to limit losses as a result of defaults on hotel and restaurant mortgages. Parts 1-4 of this series discussed pre-foreclosure options available to lenders dealing with hotel/restaurant mortgage defaults. 702.015(4) , Fla. York, 903 So.

That’s because you provide all of the collateral for the loan in cash, so it’s not a risk for the lender. Similar to credit-builder loans, passbook or CD loans are offered by some banks to existing customers using the balance you already have in a CD or savings account. Peer-to-Peer Loans. Personal Loans. Auto Loans.

No credit check to apply *Money added to Credit Builder will be held in a secured account as collateral for your Credit Builder Visa card, which means you can spend up to this amount on your card. FICO® Scores are used by 90% of top lenders ¹Credit score calculated based on FICO® Score 8 model. or Stride Bank, N.A.,

PMI protects lenders in case you can’t make payments on your home loan. If your down payment is less than 20% of the home loan, you won’t take a financial architect to tell you that the lender owns more of your home. Indeed, the lender might have more to lose if your deal goes south. The Importance of Equity and Your Refinance.

The six month pause on payments instituted by Australian Banks was certainly not designed to accommodate the situation we now find ourselves in. Currently, banks are moving to phase 2 where their customers’ individual circumstances are discussed at length and an assessment is made on the need for ongoing support. Source: [link].

This is despite the fact that many lenders have made it more difficult to qualify for a loan. Startup costs can easily top $10,000 and the fact that these loans are typically secured with collateral makes it easier to qualify for larger amounts. of Americans with personal loans borrowed from a bank. million Americans, or 51.3%

Personal loans are installment loans offered by a bank, credit union, or other financial institution to an individual borrower. The former uses collateral, commonly in the form of your vehicle title, to secure repayment of the loan. The former uses collateral, commonly in the form of your vehicle title, to secure repayment of the loan.

While the SBA funds the loans, intermediary lenders administer them to borrowers. Eligibility requirements, interest rates, and repayment terms vary depending on each lender. Personal guarantee: Most lenders will require a personal guarantee stating that you as the owner will repay the loan if the business cannot.

Even a few small differences between lenders and the loans that they’re offering can have an impact on your finances. While market rates fluctuate regularly and there are many contributing factors that can affect the interest rate that a lender may offer you, here are a few strategies that you can apply when you’re seeking a loan.

You don’t want to spend too much and go over your utilization rate, but if you don’t use it regularly enough, the lender may close your account. Connect your bank account for automatic monthly payments. This makes it very low-risk for the lender, as your payments are also adding your collateral to the savings account.

Intercompany loans can have varied terms – including the amount borrowed, repayment schedule, collateral requirements, and so on. In summary, when two businesses are involved in an intercompany loan, the lender risks not receiving repayment if the lendee becomes insolvent and ultimately enters liquidation.

One reason that lenders look at credit mix is to make sure that you can be responsible with multiple types of credit. Showing that you can handle different types of credit—and multiple credit accounts at once—indicates financial reliability to potential lenders. Depending on the reason, they often do not require collateral.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content