This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Debtconsolidation may temporarily lower your credit score due to hard inquiries and changes in credit utilization, but consistent, on-time payments can help improve it over time. Carrying debt, whether its through personal loans, credit cards, mortgages, or student loans, is common in America.

If you owe multiple outstanding debts, it might be time to consider looking into a debtconsolidation loan. “Debtconsolidation essentially means combining and downsizing debts so they are easier to repay. The Most Important Factors For DebtConsolidation Loans. ” Ads by Money. .

If you owe multiple outstanding debts, it might be time to consider looking into a debtconsolidation loan. “Debtconsolidation essentially means combining and downsizing debts so they are easier to repay. The Most Important Factors For DebtConsolidation Loans. ” Ads by Money. .

The top reason Americans were borrowing in January 2021 was to get out of debt. Some 37.17% of people surveyed who reported ever taking out a personal loan said they used the funds for debtconsolidation. That is, unless your credit score is too low to qualify. of Americans with personal loans borrowed from a bank.

A personal loan is money borrowed from a lender that can be used for almost any purpose, from debtconsolidation to home improvement projects. Most people don’t have $5,000+ sitting in their bank accounts—that’s where personal loans come in. If you qualify for a loan, you’ll be issued a lump sum deposited into your bank account.

27 million Americans have personal loan debt ( TransUnion ) At the end of 2022, the average new loan amount was $8,018 ( TransUnion ) The average amount owed in personal loan debt was $11,116 at the end of 2022 ( TransUnion ) In November of 2022, personal loan interest rates were the highest they’ve been since May of 2011 ( St.

According to recent statistics , millions of Americans have personal loan debt, with the average loan amount being $16,931. Personal loans can be used for various reasons, whether for debtconsolidation, medical expenses, or home improvements. You can get a personal loan from banks, creditunions, or online lenders.

How Personal Loans Affect Your Credit Score. Personal loans are installment loans offered by a bank, creditunion, or other financial institution to an individual borrower. ConsolidatingDebt. Personal loans can help with debtconsolidation. Balance Transfer Credit Card.

Debtconsolidation allows you to take multiple debts and combine them into one, and you can do this with your credit card debt. Doing this makes managing the debt a little easier, and you may be able to get a lower interest rate. Banks, on the other hand, generally require a good credit score to qualify.

They’re great for credit card debtconsolidation, home improvement projects, major car repairs, or any other cash-heavy project. Since personal loans are unsecured, you’ll need an excellent credit score to get the best deal. Instead, profits go back to the creditunion’s members.

This contract is often sold to a bank, finance company, or creditunion that will collect your payments. “You should compare multiple rates, starting with your local creditunion. Creditunions almost always will be the cheapest place.”

But what sets these digital lenders apart from traditional banks and creditunions? Unlike traditional brick-and-mortar banks, digital lenders often boast streamlined application processes, competitive interest rates, and innovative features designed to appeal to tech-savvy consumers.

Whether they’re for debtconsolidation, a home improvement project, or other expenses, these loans often come with low-interest rates and flexible repayment options. If your main goal is to consolidatedebt, try the best debtconsolidation loans. Our Partner Get Started Best for CreditUnion Lending: PenFed.

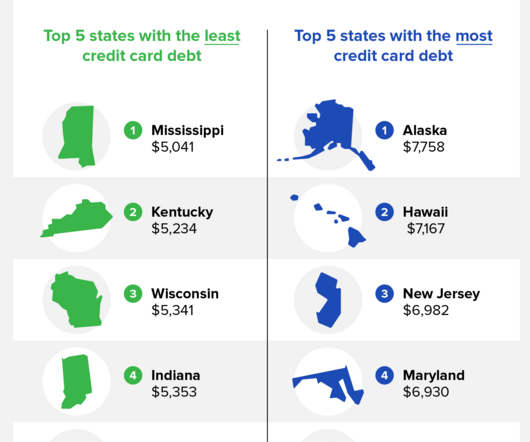

The average household credit card debt in America is $9,654, and the states with the largest amount of credit card debt are Alaska, Hawaii, and New Jersey. Between the first quarters of 2022 and 2023, The Federal Reserve Bank of New York reported that the credit card debt in America rose by $145 billion.

Types of personal loans include: Installment Plan Payday Peer-to-Peer Lending Cosigner /Guarantor DebtConsolidation Variable Rate Fixed Rate During your bankruptcy proceeding, at least a portion of these loans will be discharged, whether you borrowed from brick-and-mortar or online lenders. Unsecured loans don’t have collateral.

Average interest rates for new credit card offers Lending Tree analyzed the terms and conditions of 200 credit cards from upwards of 50 different credit card companies, banks and creditunions. Create a budget: Cutting your spending can help you have additional funds to pay down your debt.

You could qualify for a personal loan with a 560 credit score , though you can expect higher rates here, too. In some cases, working with a local creditunion can help you to get approved with slightly better rates than a bank as federal creditunions have a lower maximum APR.

How much credit card debt the average American has (and how to pay it off) The average American household now owes $7,951 in credit card debt, according to the most recent data available from the Federal Reserve Bank of New York and the U.S. Census Bureau. But that’s just the average.

Even more good news, you can be approved for a personal loan with a 620 credit score; however, it will come with higher rates. You may want to start your search with a creditunion. These financers often offer a lower APR than banks and other local lenders. Debtconsolidation loan. Installment loan.

Student Credit Cards. How To Choose the Best Credit Card. Balance Transfer Credit Cards. If you already have a large amount of high-interest credit card debt, you may be able to do a debtconsolidation into a balance transfer credit card. In most cases, you’ll be given a secured credit card.

Having a bad credit score can make it difficult to get a loan. “A bad credit score is somewhat of an indicator of your short, medium, and long-term ability to repay the loan, which is how banks make money.” The best way to improve your credit score is to focus on paying your debts off on time.

Having a bad credit score can make it difficult to get a loan. “A bad credit score is somewhat of an indicator of your short, medium, and long-term ability to repay the loan, which is how banks make money.” The best way to improve your credit score is to focus on paying your debts off on time.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content