This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Commercial banks may be the obvious choice, but they aren’t the only option for your mortgage. Mortgage brokers , online mortgage lenders , and creditunions also originate mortgage loans. Creditunions and other non-banks are gaining in popularity for mortgage originations. Find a Mortgage.

When account owners have an account that reflects a negative balance, the lender is faced with a myriad of options and obligations with regard to the pursuit of that debt. Lenders that charge off a debt trigger issuance of the 1099-C when their defined policy leads the lender to discontinue collection activity and discharge a debt.

The Consumer Financial Protection Bureau (CFPB)’s decision to establish supervisory powers over nonbank financial institutions will level the playing field and subject those companies to much-needed scrutiny, creditunion trade groups informed the agency Tuesday. Response From CreditUnion Trade Groups.

You can open an account with a traditional bank, set up an online bank account , or choose a neighborhood creditunion. As you’re reviewing your options, you may see some claims that creditunions are better than banks. Why is a creditunion better than a bank for some people?

Banks and creditunions that have Black leadership — based on how their executives or board members identify — tend to serve communities that are majority Black. The article 14 Mortgage Lenders Serving Black Communities originally appeared on NerdWallet. Kate Wood writes for NerdWallet. Kate Wood writes for NerdWallet.

Bank student loans are no longer available. Bank loans or take out new student loans from other banks, as well as creditunions and online lenders. When shopping for any private student loan, compare multiple lenders’ offers to ensure you get the lowest interest rate possible. The article U.S.

And her bank wouldn’t give her and her husband Larry a loan to buy a replacement home. Community Development Financial Institutions, which include banks, creditunions, loan and venture funds, are making second-chance loans where others may fear to tread. “We Other Second Chance Loans for Bad Credit Borrowers.

However, there are important aspects of the Construction Lien Law that can directly affect the rights and obligations of lenders in numerous ways. Accordingly, lenders making construction loans or those whose loan will be secured by a mortgage on real property, must be aware of notices of commencement and their requirements under Fla.

Most SBA loans are issued by banks, creditunions and other financial institutions, not the government. The best lenders have substantial experience with these small-business loans, so you get effective help during the application process and hopefully increase your chances of approval. Randa Kriss writes for NerdWallet.

According to the Federal Reserve’s 2021 Small Business Credit Survey, banks remain the most common source of credit for small businesses — compared with options such as online lenders, community development financial institutions or creditunions. Randa Kriss writes for NerdWallet.

Please join Consumer Financial Services Partner Chris Willis and his guests and colleagues James Stevens and Carlin McCrory as they discuss the consumer protection and safety and soundness sides of creditunion regulation. Transcript: Consumer Protection and Safety and Soundness Perspective of CreditUnion Regulation (PDF).

Banks and creditunions should not only routinely require, but also closely scrutinize, criminal background checks during the hiring process in order to maintain compliance with applicable regulatory schemes. The SBA regulations will apply to both banks and creditunions that process SBA loans.

Step 1: Find Out Your Credit Score The first step is to review your credit score, which is crucial in the loan approval process. Lenders use it to assess how likely you are to pay them back. If you have a low score, the lender might consider you high-risk, charge you higher interest rates, or even deny the loan.

You can refinance through a private creditunion, bank or online lender. Student loan refinancing is a financial move you make to combine all of your existing loans with a new rate and loan term. Moving forward, you will. Anna Helhoski writes for NerdWallet. Email: anna@nerdwallet.com. Twitter: @AnnaHelhoski.

Sections 521-523 of DIDMCA empower state banks, insured state and federal savings associations, and state creditunions to charge the interest allowed by the state where they are located, regardless of where the borrower is located and regardless of conflicting state law (i.e.,

When you get a mortgage, you receive your financing from a lender, such as a bank or creditunion. However, the lender may not be the institution that actually manages the loan over the long term. Taylor Getler writes for NerdWallet.

This filing comes just three days after CUNA and the National Association of Federally-Insured CreditUnions (NAFCU) sent a joint letter to the CFPB urging it to stay enforcement and implementation of the Final Rule for all covered financial institutions until after the U.S. CFPB (discussed here ).

On October 24, the Federal Reserve Board (Fed), the Federal Deposit Insurance Corporation (FDIC), and the Office of the Comptroller of the Currency (OCC) (collectively, the agencies) finally issued their long-awaited final rule modernizing how they assess lenders’ compliance under the Community Reinvestment Act (CRA).

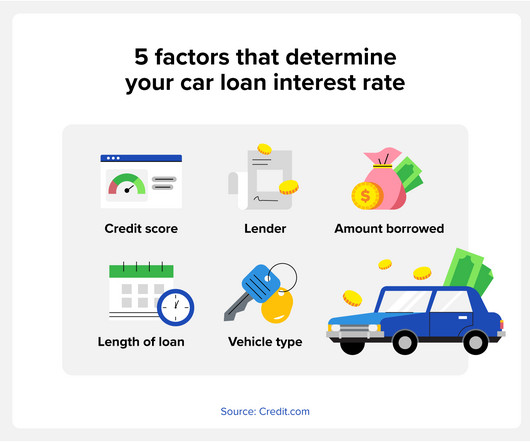

A credit score plays a large role when lenders determine vehicle interest rates, but it’s not the only factor. Credit Score Credit scores are a quick way for lenders to determine the level of risk when lending money. Different lenders may offer better rates, depending on your score.

This means that consumers with the strongest credit scores tend to have a mix of accounts. If your goal is to build or maintain great credit, you’ll want to get and keep different types of credit accounts. One reason that lenders look at credit mix is to make sure that you can be responsible with multiple types of credit.

Many loan interest rates are based on the prime rate , which is essentially the rate that banks charge their preferred customers and those with the best credit scores. This rate is largely determined by the federal funds rate, which is the rate banks charge each other. They do tend to be lower than credit card rates, though.

Small Business Administration and issued by participating lenders, typically banks and creditunions. Franchisees looking to get an SBA loan can fund their business with an SBA 7(a) or SBA CDC/504 loan. These SBA loans are partially guaranteed by the U.S. Caroline Goldstein writes for NerdWallet.

In recent years, the rise of digital lenders like SoFi and Ally has transformed the lending landscape, offering borrowers new options for obtaining loans quickly and conveniently. But what sets these digital lenders apart from traditional banks and creditunions? Here are the steps to follow: 1.

This is despite the fact that many lenders have made it more difficult to qualify for a loan. While online lending has become increasingly popular, more people are going to banks than any other type of lender–regardless of gender or age. That is, unless your credit score is too low to qualify. million Americans, or 51.3%

.” About SpringFour:Founded in 2005, SpringFour is the first-of-its-kind, leading financial health fintech that empowers banks, creditunions, fintech lenders, employers, loan servicers, mortgage insurers, nonprofits, and organizations across all industries to connect consumers with vetted, local nonprofit and government financial health resources. (..)

Quick answer: You can try joining a creditunion, signing up for a starter credit card, getting a credit card through your current bank, applying for a secured credit card, becoming an authorized user on another person’s account or taking out a credit builder loan.

They all have come out with their own ways to create roadblocks for medical credit reporting. Shouldn’t all unpaid debts ( medical or otherwise), be reported to credit reports in the same way? Then let the lenders decide which one they want to consider or ignore. Now he can qualify for $500,000 loan.

Small Business Administration and issued by participating lenders, such as banks and creditunions. Like many SBA loans, SBA 7(a) loans are partially guaranteed by the U.S. SBA 7(a) loans are the most common type of SBA loan, and therefore, the 7(a) loan program is one of the main ways the SBA supports small businesses.

The following is a guest post from Dr. David L Tuyo II, president and CEO of University CreditUnion. Even a few small differences between lenders and the loans that they’re offering can have an impact on your finances. Maintain a Good Credit Rating. Get Your Free Credit Score. Set Up Automatic Payments.

Online lenders make it easy to compare rates and terms and find the right online personal loan for your situation. That is, the lender advances you money that you pay back with interest over a predetermined period of time. This often allows digital lenders to streamline the applications. Benefits of Online Personal Loans.

Lenders face a myriad of challenges these days. This makes them an ideal solution for banks and creditunions that don’t have enough data to create their own custom models but still want the flexibility to grow their portfolios responsibly. Pooled models can be licensed as “off-the-shelf” and quickly used.

The CFPB has the authority to stretch its long arm as far as the most remote corner of the United States and its territories in order to supervise and audit local banks, creditunions, payday lenders, debt collection agencies, and more.

The auto loan industry is quite a diverse one, and loan terms can vary considerably from one lender to another. Many lenders will provide 100% financing, but others may require down payment as high as 20% of the value of the vehicle. Some banks and creditunions will require a minimum credit score of 650 to make an auto loan.

A personal loan is money borrowed from a bank, creditunion or online lender that you pay back in fixed monthly payments, or installments, typically over two to seven years. Jackie Veling is a writer at NerdWallet.

n]: A financially detrimental debt arrangement that only benefits the lender. Unfortunately, while the former is pretty straightforward, there’s a lot of confusion surrounding the latter – something that shady or disreputable lenders use to their advantage. And storefront operations can run differently than online lenders.

Steps to take to raise credit score after bankruptcy: Get a secured credit card. A secured card is one where you put down a certain amount of money with the bank to guarantee your repayment. You are no risk to the bank because they already have your money. Prequalify through several lenders. This is your limit.

These legislative efforts to opt-out of DIDMCA, coupled with the influx in recent “true lender” legislation, seem to show a coordinated effort to restrict bank-model lending. Sections 521-523 are codified as § 27 of the Federal Deposit Insurance Act, § 4(g) of the Home Owners’ Loan Act and § 205 of the Federal CreditUnion Act.

Explore an Online Lender. Many investors still use banks and creditunions to finance property investments , although today we have multiple options to choose from. The lender takes the property you wish to purchase as security against the loan they offer you. Let’s delve into them: Conventional Financing.

In July 2016, the Consumer Federation of America (CFA) and VantageScore Solutions reported that most consumers—more than 80%—knew basic facts about their credit scores, including that credit scores are used by lenders to approve or deny mortgages and by credit card issuers to approve or deny credit cards.

A signature loan is a fixed-rate, unsecured personal loan offered by an online lender, bank or creditunion. It’s called a signature loan because it’s secured by your signature instead of collateral, like a car or an investment account. Getting approved for a signature loan will likely depend on your creditworthiness.

This code can mean two different things: You don’t have enough accounts for lenders or credit scoring models to effectively gauge your risk as a borrower. Even if you’ve paid your bills on time, if you only have one credit card that’s been open three months, that’s not enough information for many lenders.

In a major victory for small business lenders, yesterday the U.S. The court stated the purpose of § 1071 of the Dodd-Frank Act, “is the equal application of lending laws to all credit applicants to avoid disparate outcomes, and it presumes uniform application to all covered financial institutions absent exemption by the Bureau.

Only become an authorized user if you are both committed to practicing smart credit-building habits. Credit Builder Loans. Credit builder loans aren’t widely publicized, but they are a great way to build credit without a credit card. Some lenders offer unsecured personal loans to individuals with no or bad credit.

The Act imposes sweeping changes and contains broad language, leaving the state’s lenders and borrowers with an uncertain future. With respect to loan products under the MLA, lenders cannot charge interest and fees that, when added together, would exceed a 36% MAPR. [3].

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content