This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A District Court judge in Arizona has granted a defendant’s motion to dismiss a FairDebtCollection Practices Act case, ruling that the plaintiff failed to sufficiently establish the defendant’s status as a “debt collector” under the statute and did not plead adequate facts to support the alleged violations.

With this uptick, regulatory scrutiny may rise, leading to more complaints and lawsuits under laws like the FDCPA (FairDebtCollection Practices Act) and Regulation F due to errors in handling bankrupt debt. Translation: to CYA, you need better originalcreditor contracts.] Judge Orelia E.

Does Colorado Law Protect Me From Debt Collectors? When collecting a debt from you, collection agencies must adhere to federal and state rules. Fortunately, the federal FairDebtCollection Practices Act (FDCPA) protects all states. What is the Federal FairDebtCollection Practices Act (FDCPA)?

This can lead to wage garnishment, bank levies, or liens against your property. Wage Garnishment and Asset Seizure : If a judgment is entered against you, the creditor may be able to garnish your wages, levy your bank accounts, or place liens on your property, depending on the laws in your jurisdiction.

District Court for the District of New Jersey found that the plaintiff had not suffered an injury in fact and therefore lacked standing to assert a claim under the FairDebtCollections Practices Act (FDCPA). The plaintiff incurred a debt to a bank, which sold the account to a new creditor.

There are many kinds of debts that can be sent to collections, including: Credit card payments Student loans Medical bills Rent payments Utility payments Auto loans Personal loans Tax debt The time it takes the originalcreditor to transfer your debt to collections varies.

Portfolio Recovery buys multiple accounts with old debt from companies that have given up and “charged off” the accounts. In other words, when the originalcreditor has been unsuccessful in collecting on a debt, it will write off the debt as a loss. Make Them Prove the Debt is Yours.

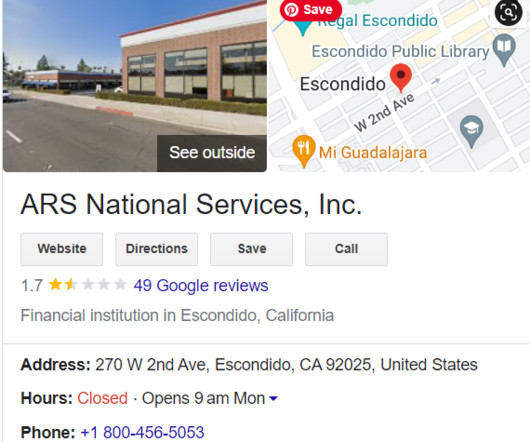

The FairDebtCollection Practices Act (FDCPA) and other laws provide you with rights and protections that you can use to fight back against such behavior. When dealing with a debt collector like ARS National Services, confirming that the debt is yours is important.

Identify Errors Compare your credit reports to your financial records, like bank statements, and verify these details: Account numbers and identity information: Make sure account numbers match your personal records and that your name, address, and contact information are accurate.

Make sure to follow through, because credit agencies can turn a simple collection into a judgment, legally garnishing wages or your bank account, you will be required to pay the full debt as well as legal fees. Debt Validation. If you can, try to settle with the originalcreditor.

In addition to requesting a written validation notice from the collector, verify with your state attorney general’s office or the Better Business Bureau that the collection agency is legitimate. The FairDebtCollection Practices Act (FDCPA) provides protection for consumers. Bank Account Draft/ACH.

If these amendments become final, New York will be an opt-in jurisdiction instead of an opt-out jurisdiction, meaning debt collectors must communicate by telephone or letter to obtain consent to text or email, even when a consumer already opted into digital communications about their account.

They collect a variety of debts including those from banks, telecommunication companies, student loan providers, college and universities, and more. Even if you pay off the debt, EOS CCA’s collection account will not disappear from your credit report. Steps to Remove EOS CCA from Your Credit Report.

If you’re unable to pay your originalcreditor, your debt may pass to a debt recovery agency, earning a collection letter and possibly a stain on your credit report. If an agreement is reached, avoid granting the company access to your bank account. CCS may haggle with you. Tips for Dealing with CCS.

The debtcollection agency will send letters, make phone calls and sometimes even visit the debtor in person to attempt to collect the debt. If the debtor still refuses to pay, the creditor may file a lawsuit and take the debtor to court.

Some debt buyers —companies that buy and try to collect very old debts—still go after borrowers and might even take them to court. If they do this knowing that the debt is past the statute of limitations, they may have violated the FairDebtCollections Practices Act. You default on that debt.

Depending on the nature of the debt and how communicative the debtor is (or isn’t), commercial debt collectors can employ other tactics like investigating other debt and performing a skip trace on the owner to establish contact. This could lead to bank account garnishment.

If you have a debt that you haven’t paid yet, you may have heard from a debt collector called CCS Offices. CCS Offices is a company that collectsdebts on behalf of originalcreditor. They do this by either purchasing the debt or collecting the payments and taking a portion for themselves.

Our rating: False There is nothing illegal about collection agencies buying debt from third parties and attempting to collect it. The post also misrepresents the protections in place to prevent harassment by debt collectors. The $1,000 maximum is also per lawsuit, not per incident as the claim asserts.

Palisades Collection LLC, also known as ASTA Funding, is a small debtcollection agency that is headquartered in Englewood Cliffs, NJ. As a third-party collector, they buy old debt from banks, credit card companies, hospitals, cell phone companies for pennies on the dollar in order to make money on the collections.

This is a way that you can get the collection entry deleted on a technicality. Under the FairDebtCollection Practices Act (FDCPA) , you have a right to request that a debt collector verify that the debt belongs to you before you make any payments on it. Never allow them direct access to your bank account.

If you have heard from a debt collector called Rausch Sturm, you are probably being pursued for an old debt. You have also probably seen them appear on your credit report as a collections account. This is because Rausch Sturm has been hired by your originalcreditor to collect the debt on their behalf.

Ask the Collection Agency to Validate the Debt. If you can’t find inaccuracies on your credit reports, write to the collection agency and ask it to validate your debt. The main issue here is that you have only 30 days to make the request after the collection agency first contacts you. AWA Collections.

Suddenly, the debt reappears on your credit report, except now it’s a zombie debt. Zombie Debts and Judgments. If the originalcreditor went to court and obtained a judgment against you for a debt, the zombie debt cycle can be more complicated. It can also seem a bit more vicious.

THE FairDebtCollection Practices Act (FDCPA) is a federal law that was enacted in 1978 by the United States Congress to protect consumers from abusive debt collectors. Note, however, that the FDCPA applies only to third party collectors who collectdebt for originalcreditors. Fremont Ave.,

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content