This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Banks, lenders, and other financial players are accelerating their digital transformation roadmaps, shortening years’ worth of development into mere months, in an attempt to service consumers at scale while managing the complexities of our new normal and the limitations of outdated infrastructure.

Oftentimes, individuals or businesses borrow money from a bank or lender, and unfortunately, are unable to pay the loan payments. In this event, the borrower may try to shift the blame of their inability to pay on the bank or lender, by filing a claim for negligent loan processing or underwriting, and/or breach of fiduciary duty.

When a borrower defaults on a mortgage, lenders will likely execute their right to foreclose on the property by filing a lawsuit. However, lenders are not always the successful party in the foreclosure and, to the disappointment of the lender, the lawsuit may be dismissed. Bank National Ass’n , 211 So. 2d 1004 (Fla.

However, there are important aspects of the Construction Lien Law that can directly affect the rights and obligations of lenders in numerous ways. Accordingly, lenders making construction loans or those whose loan will be secured by a mortgage on real property, must be aware of notices of commencement and their requirements under Fla.

When account owners have an account that reflects a negative balance, the lender is faced with a myriad of options and obligations with regard to the pursuit of that debt. Ocwen Loan Servicing, LLC, 8:14-CV-3214-T-35MAP, 2015 WL 12938920, at *1 (M.D. Charging Off” Uncollectable Debt. 1099-C Issuance. 1.6050P-1(b)(2)(i).

Along with taking action against more than a handful of financialservices companies in the name of consumer protection, the agency made headway on myriad other issues. Treasury’s request for information on the use of artificial intelligence in the financialservices sector.

The SBA, through the Office of Credit Risk Management (“OCRM”), monitors and oversees the activities of all its lenders and CDCs to ensure it is effectively following loan program requirements and protecting the integrity of the SBA program. There are ten grounds that may trigger an enforcement action against all SBA lenders and CDCs.

Lenders should be cognizant about what expenses are classified by the SBA as recoverable or non-recoverable. Expenses incurred by a 7(a) Lender or CDC that failed to liquidate the SBA Loan in accordance with Loan Program Requirements, including those pertaining to Liquidation or Litigation Plans. What Expenses are Recoverable. .;

This presentation was moderated by the firm’s managing partner, and is geared towards special asset departments of banks and financial institutions. This webinar addressed what is new in foreclosures, including recent developments in the law since the last foreclosure crisis and how banks can utilize the law to their advantage.

In Florida, a lender initiates a foreclosure by commencing a lawsuit in the county where the property is located. If the lender is successful, the lender will receive a final judgment of foreclosure from the court and the property will be sold at a public auction. If the Lender Was Unsuccessful, Should It Appeal?

Lenders who move for summary judgment under Florida’s new summary judgment standard will likely enjoy more favorable outcomes. The court’s more rigorous review of attempts to withstand summary judgment will change expected litigation outcomes, impact litigation strategy, and largely benefits lenders. appeared first on Jimerson Birr.

Lenders must pay particular attention to subordinate liens and encumbrances prior to initiating any foreclosure action. Lenders can discover whether subordinate liens and encumbrances exist on a property by performing a title examination prior to initiating foreclosure. Subordinate Liens. York, 903 So. 2d 981, 983 (Fla. 2d DCA 2005).

Lenders are responsible for servicing and liquidating all of the 7(a) loans in their portfolio. CDC’s are responsible for servicing 504 loans in their portfolio, but they will only be responsible for liquidating the loan based on its designation. Servicing and Liquidation Take-Over by SBA. Performance Standards.

The good news for lenders and debt collectors is that a reported 72% of consumers have a New Years resolution to pay off debt in 2025. CFPB Looks at Medical Debt, Student Loans and So Much Data Medical debt wasnt the only focus for the Consumer Financial Protection Bureau in Q4.

Troutman Pepper announced today that a nationally recognized consumer financialservices group has joined the firm from Ballard Spahr in Atlanta, New York, Philadelphia, and Salt Lake City. The industry-leading group includes partners Christopher J. Willis , Mark J. Furletti , Jeremy T. Rosenblum , Stefanie H. Cover , and Anthony C.

If a borrower is experiencing difficulties making payments on their SBA loan, they may seek relief with the lender or CDC by requesting a loan modification or deferment. Borrowers must submit current financial statements, federal income tax returns for the last two years, and any additional supporting documents necessary.

If a borrower defaults on a SBA loan, the lender or CDC must assess the environmental risk of contamination before conducting any liquidation action that could result in a loss, or otherwise increase the risk of loss, due to the actual or alleged presence of contamination. SOP 50 10 5(E), Appendix 2. SOP 50 57 2 ; SOP 50 55.

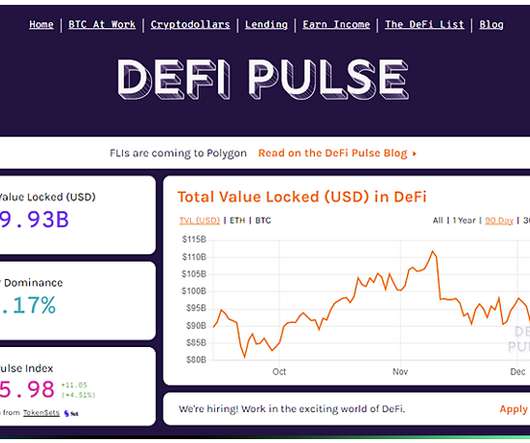

DeFi refers to Decentralized Finance; peer-to-peer financialservices on a public decentralized blockchain network, particularly Ethereum. A system that interacts buyers, sellers, borrowers, or lenders with peer-to-peer technology to access financial products or financialservices bypassing middlemen such as financial institutions.

The Consumer Financial Protection Bureau (CFPB) today ordered online lender Enova International Inc. to pay a $15 million penalty for widespread illegal conduct including withdrawing funds from customers’ bank accounts without their permission, making deceptive statements about loans, and cancelling loan extensions.

However, lenders should be aware that judges are still able to refer foreclosure lawsuits to mediation on a case-by-case basis, with or without a referral request to mediation. Although there is no longer a statewide mandatory foreclosure mediation program, lenders must be aware that they may still be required to participate in mediation.

On October 24, the Federal Reserve Board (Fed), the Federal Deposit Insurance Corporation (FDIC), and the Office of the Comptroller of the Currency (OCC) (collectively, the agencies) finally issued their long-awaited final rule modernizing how they assess lenders’ compliance under the Community Reinvestment Act (CRA).

Federal Activities: On December 8, the Office of the Comptroller of Currency (OCC) released its Semiannual Risk Perspective for Fall 2022 , which discusses major risk themes facing the federal banking system. banking system’s exposure to the crypto industry. million investment in Washington-based bank Moonstone Bank.

For banks, credit unions, and other lenders, the sudden shift to digital-only interactions has introduced a variety of internal and external challenges, as well as some opportunities. In fact, the main attrition driver for financial institutions is a poor banking app. Humanizing the Digital Experience.

The past year was one of transition in the Washington, DC policy arena as a new President, Congress and group of banking agency heads took charge of the financial legislative and regulatory policy agenda. Open Banking Begins to Take Off in the U.S. with New Rules Promulgated by the CFPB. However, 2022 should signal a change.

The FTC’s Safeguards Rule requires nonbanking financial institutions, such as mortgage brokers, motor vehicle dealers, and payday lenders, to develop, implement, and maintain a comprehensive security program to keep their customers’ information safe. For more information, click here. On October 26, Senator Cynthia M.

Confessions of judgment may no longer be permitted as part of the necessary documents when buying or selling financialservices or products to consumers in New York. The proposed bill does not currently apply to commercial lenders. Therefore, it will most likely be “business as usual” for commercial lenders and the like.

To keep you informed of recent activities, below are several of the most significant federal and state events that have influenced the Consumer FinancialServices industry over the past week: Federal Activities State Activities Federal Activities: On January 29, Acting Comptroller of the Office of the Comptroller of Currency (OCC) Michael J.

On March 15, the Federal Reserve announced that the FedNow Service will start operating in July. financial system during a conference held by the Independent Community Bankers of America. For more information, click here. For more information, click here. On March 14, Federal Reserve Governor Michelle W. Lanham, et al.

In reviewing a loan file after a default by a borrower, lenders should evaluate whether the loan includes an acceleration clause and whether the loan is secured by any personal guaranties. Part 2 of this series analyzed pre-foreclosure loss mitigation options for lenders dealing with hotel/restaurant mortgage defaults.

Senator Lummis, a vocal supporter of Bitcoin, has been more critical of stablecoins, particularly Tether, and has opposed central bank digital currencies. The report found that the CFPB’s Office of Supervision Examinations (OSE) does not have a formal policy that requires bank examiners to rotate assignments in a specified time frame.

CFS Partner Lori Sommerfield brings more than two decades of experience in representing a wide range of banks, financial institutions, and financialservices companies in fair lending and responsible banking regulatory compliance. Transcript: CFPB’s Section 1071 Final Rule (Part 1): A General Overview

On November 22, the Federal Reserve Board, the Federal Deposit Insurance Corporation, and the Office of the Comptroller of the Currency announced that the comment period on their long-term debt proposed rule to improve the resolvability of large banks and enhance financial stability, will be extended until January 16, 2024.

On August 30, the Federal Reserve Bank of Kansas City published an overview of the Bitcoin ATM (BTM) industry. banking system, to reduce the costs and impacts of large bank resolution, and to support the rapid and orderly resolution of their holding companies. For more information, click here. For more information, click here.

Origination is just the initial phase of the long and complex mortgage lifecycle, which begins with a lender qualifying a borrower and then providing the funds used to purchase a new property or refinance an existing property. The lender then holds the mortgage on its balance sheet or sells the mortgage on the secondary market to investors.

On December 1, the House of Representatives approved a resolution to repeal a Consumer Financial Protection Bureau (CFPB) rule that mandated banks to gather data on loan applications from women-owned, minority-owned, and small businesses to help lenders identify business development needs and opportunities. on June 5-7, 2024.

On May 26, the European Central Bank published two reports on its market research and prototyping exercise, which were both conducted as part of the investigation phase of the digital euro project. The CFPB alleges that the bank failed to properly manage and respond to customers’ credit card disputes and fraud claims.

Policy Predictions for FinancialServices Companies. Open banking, BNPL, cybersecurity and AI will all be under the microscope for regulators and policymakers, but not all areas will see major action in 2023. The CFPB's New Open Banking Proposal Will Accelerate Exciting Product Innovations. Four 2023 U.S. FICO Admin.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. House of Representatives passed seven bipartisan bills introduced by House FinancialServices Committee members.

On September 15, the Financial Crimes Enforcement Network (FinCEN) assessed a $15 million civil money penalty against Bancrédito International Bank and Trust Corporation (Bancrédito) for willful violations of the Bank Secrecy Act and its implementing regulations. commercial banks and savings associations of $13.7

On August 1, the Board of Governors of the Federal Reserve System (the Fed) delivered to Congress its Cybersecurity and Financial System Resilience Report (report). Banks reported that lending standards are currently on the tighter end of the range for all loan categories. For more information, click here.

However, lenders often wonder where they should file the foreclosure action if the loan is secured by mortgaged land situated in different counties. Intercredit Bank, N.A. , Flagship Cmty Bank , 96 So. allows the lender to bring a single foreclosure action on all mortgages in just one county. 2d 863, 864 (Fla.

When a lender obtains a final judgment of foreclosure from the court, the mortgaged property is sold at public auction and, if bought by someone other than the foreclosing lender, the proceeds are applied to the debt owed by the delinquent borrower. Compass Bank , 164 So. Liberty Bank , 87 So. 702.06, Fla. 702.06, Fla.

Dream First Bank, National Association, has agreed to assume all the deposits of Heartland and almost all of Heartland’s failed bank assets. Dream First Bank, National Association, has agreed to assume all the deposits of Heartland and almost all of Heartland’s failed bank assets. For more information, click here.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. Troutman Pepper has developed a dedicated COVID-19 Resource Center to guide clients through this unprecedented global health challenge.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content