This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Filing for chapter13bankruptcy can seem like a daunting task, but it’s often the right move for those who are facing foreclosure, repossession, or have exorbitant debts. If you’re thinking of filing for chapter13bankruptcy, you may have questions regarding how it will impact your credit score.

Though every situation is different, contacting an attorney that specializes in bankruptcy can be the first step in achieving financial freedom. Will My Student Loans Be Discharged if I File for Chapter13Bankruptcy? While getting student loans fully discharged through bankruptcy is rare, it is not impossible.

While people have many bankruptcy options, typically, people only file for Chapter 7 or Chapter13bankruptcy – two of the most commonly used debt relief solutions. Here’s what you should know: What is Chapter 7 bankruptcy? What is Chapter13bankruptcy?

However, though a person can be struggling at the time they file, this does not mean it isn’t possible for their financial situation to greatly improve while they are still paying off their Chapter13bankruptcy plan. Chapter13Bankruptcy and Disposable Income. Paying Off a Chapter13Bankruptcy Early.

Filing for Chapter 7 or Chapter13Bankruptcy: Chapter 7 will wipe out (discharge) your medical debt along with other unsecured debt, but you must have low enough income to pass the means test in order to qualify for it. Chapter13bankruptcy is discussed below. We are here to help.

Chapter13bankruptcy can help consolidate your debt so you can repay it, usually over 3 to 5 years. Your monthly payments will depend on your income since the plan is income-based, and while Chapter13 can put you on the right financial path, it typically means making sacrifices in the short term. This Read More.

However, you can get rid of the financial and emotional pressure of being a debtor by filing for Chapter 7 or Chapter13bankruptcy. Both Chapters can help you start anew and discharge your debts, but they work differently. Chapter13 doesn’t work the same way. The main difference. Financial relief.

When you’re considering Chapter13bankruptcy, you’re also wondering how much of your debt you’d be obligated to pay back. Let’s take a look at a debtor’s obligations under Chapter13bankruptcy. What Is A Chapter13Bankruptcy Plan? We are ready to help.

If you have non-exempt assets that you’re wishing to keep or don’t pass the Chapter 7 means test, you’ll need to file through Chapter13. Chapter13 can make your non-dischargeable tax debts more manageable. This repayment plan pools your existing debts in order to pay back creditors, including the IRS.

Chapter13bankruptcy can wipe out most kinds of debts and leave you with a much brighter financial picture. But Chapter13 can’t discharge all types of debt you’ve taken on. Some debts will remain after your bankruptcy, although you’ll be in a much better position to handle them.

Chapter13bankruptcy offers the option of lien stripping. If you’re filing or considering filing for Chapter13, you need to be aware of the process and advantages of lien stripping. Chapter13 lien stripping can be beneficial to your financial situation and may even help you save your home.

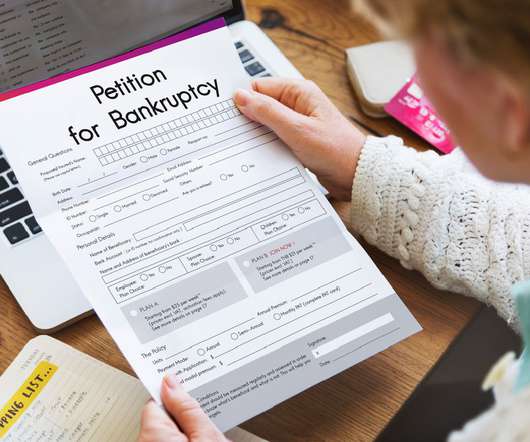

Filing for Chapter13bankruptcy can provide much-needed relief if you are overwhelmed with debt and struggling to keep up with payments. Under Chapter13, you repay a portion or all of your debt, allowing you to keep assets like your home or car. What Is Chapter13Bankruptcy?

Chapter13bankruptcy offers the option of lien stripping. If you’re filing or considering filing for Chapter13, you need to be aware of the process and advantages of lien stripping. Chapter13 lien stripping can be beneficial to your financial situation and may even help you save your home.

If you’re at risk of losing your home, Chapter13bankruptcy could be your best option. When you’re going through the process of filing Chapter13, foreclosure cannot occur because you’re granted an automatic stay, meaning that lenders cannot pursue your debts and recover collateral, including your home.

After filing for Chapter13bankruptcy, you give up a lot of financial control to your bankruptcy trustee. Even though you keep possession of your property, like a home, it becomes part of your Chapter13bankruptcy estate. The post Chapter13Bankruptcy: Can You Buy Or Sell A House ?

Fortunately, there's a potential remedy available: Chapter13bankruptcy. Chapter13bankruptcy, often referred to as a "wage earner's plan," allows individuals with regular income to develop a plan to repay all or part of their debts over three to five years.

When you file for a Chapter13bankruptcy in Nashville, you likely will not receive a discharge until the completion of your repayment plan. Since Chapter13 lasts for three to five years, one or more financial circumstances may arise to interfere with your repayment plan.

With that said, the vast majority of filers do not have any of their assets sold during the bankruptcy process. On the other hand, Chapter13bankruptcy is known as a reorganization bankruptcy. The debtor pays a bankruptcy trustee, who then distributes the payments to the creditors.

When filing Chapter 7 or Chapter13bankruptcy, it’s critical to understand the difference between consumer debt and non-consumer debt. If you’re considering filing Chapter 7 or Chapter13bankruptcy, consider enlisting the help of skilled bankruptcy attorneys. What is Consumer Debt?

However, if you’re struggling with multiple debts, Chapter13bankruptcy could be a great opportunity. If you are simply struggling to pay your mortgage but are not yet behind on your payment schedule by much, negotiating a loan modification may be a better option.

Filing for Chapter13bankruptcy can be both challenging and stressful. One common question that filers have regarding the Chapter13 process involves income increases and whether they affect payment plans. For experienced Chapter13bankruptcy attorneys in Indiana , contact the offices of Sawin & Shea, LLC.

It’s a smart choice to file for Chapter13bankruptcy. Your bankruptcy plan will allow you to catch up on payments and settle your debts while giving you a chance to keep your home treasured belongings. If you have a job but you’re struggling to make your payments every month, Chapter13 can help.

Bankruptcy is one of the fastest and most effective ways to find debt relief. Most consumers who follow this path will file for Chapter 7 bankruptcy or Chapter13bankruptcy. To help you understand the difference between Chapter 7 and Chapter13bankruptcy, here’s.

In 2012, the primary borrower filed for Chapter13bankruptcy protection, listing the defendant trusts as creditors for the student loans. The bankruptcy plan was confirmed, and the trusts filed proofs of claims which were not objected to by the plaintiffs.

Your investment real estate’s outcome depends entirely on whether you file for Chapter 7 or Chapter13bankruptcy. Investment Real Estate in Chapter 7 Bankruptcy. Chapter 7 bankruptcy is a great option for those looking to discharge eligible debts. Chapter13 Cramdowns.

For example, the debt limit for an individual to qualify for a Chapter13bankruptcy case will rise to $1,395,875 of secured debt, and certain exemption amounts will also increase. The total debt amount in the definition of small business debtor in Section 101(51D) will rise to $3,024,725 from $2,725,625.

One major benefit of bankruptcy is that, in Chapter13 cases, you can still keep your home or car after missing payments. After declaring a Chapter13bankruptcy, you’ll have three to five years to make up for your missed payments. Will Bankruptcy Eliminate All of My Debts?

In this blog, we discuss situations in which your employer will be notified about your bankruptcy, and we also cover whether or not you can be legally fired for declaring bankruptcy. Will My Employer Be Notified About My Bankruptcy? If a potential employer runs a background check, they’ll discover your bankruptcy.

Your Credit Report as Part of Your Bankruptcy. After your Chapter 7 bankruptcy discharge or Chapter13bankruptcy period, your bankruptcy attorney will request permission to pull and review your credit report. It’s a way to make sure that you’re receiving the full benefits of your bankruptcy.

For example, the debt limit for an individual to qualify for a Chapter13bankruptcy case will rise to $1,257,850 of secured debt, and certain exemption amounts will also increase. The total debt amount in the definition of small business debtor in Section 101(51D) will rise to $2,725,625.

The good news is that we can still help you with your debts by filing a Chapter13, or reorganization, case if non-exempt assets would cause a problem in a Chapter 7 filing. In a normal Chapter13 there is no liquidation of assets. Every state handles bankruptcy exemptions differently.

Perhaps the most common misconception is the notion that filing for bankruptcy means that you lose all of your wealth and possessions. When filing for Chapter 7 or Chapter13bankruptcy, you’ll qualify for exemptions that allow you to keep some of your money and certain types of personal property.

If you are thinking of filing for Chapter 7 or Chapter13bankruptcy, or if you have already filed, you may be concerned about how long the bankruptcy will stay on your credit report. The situation is more complicated with Chapter13bankruptcy.

Bankruptcy can also stop or delay a home or mortgage foreclosure, stop collection actions, stop garnishments and lawsuits. What Do the Various Kinds of Bankruptcy Entail? There are many intricacies that set Chapter 7 and Chapter13Bankruptcy apart. What does each one mean?

If you’re not sure whether some of your purchases are considered “luxury,” consult with a Chapter 7 or Chapter13bankruptcy attorney. If you make a luxury purchase of over $600 within 90 days of filing for bankruptcy, creditors will request for the bankruptcy court to not discharge the debt.

For example, the debt limit for an individual to qualify for a Chapter13bankruptcy case will rise to $1,580,125 of secured debt, and certain exemption amounts will also increase. Other adjustments will affect consumers more than business debtors.

For example, the debt limit for an individual to qualify for a Chapter13bankruptcy case will rise to $1,580,125 of secured debt, and certain exemption amounts will also increase. Other adjustments will affect consumers more than business debtors.

For example, the debt limit for an individual to qualify for a Chapter13bankruptcy case will rise to $1,395,875 of secured debt, and certain exemption amounts will also increase. Other adjustments will affect consumers more than business debtors. Given recent inflation, these increases are larger than usual.

For example, the debt limit for an individual to qualify for a Chapter13bankruptcy case will rise to $1,395,875 of secured debt, and certain exemption amounts will also increase. Other adjustments will affect consumers more than business debtors. Given recent inflation, these increases are larger than usual.

They are worried their Chapter13 payment plan will take too long to complete. They are interested in surrendering a property that is protected and saved in Chapter13. What Are the Benefits of Converting a Chapter13Bankruptcy to a Chapter 7?

Fortunately, Chapter13bankruptcy offers debt relief and a solution for stopping mortgage servicers from repossessing your home. Saving Your Home From Foreclosure Through Chapter13BankruptcyChapter13bankruptcy offers a solution if you’ve fallen behind on monthly mortgage payments.

Differences between Chapter 7 and Chapter13Bankruptcies. With Chapter 7 bankruptcy , you may get a car loan upon receipt of your discharge notice, which can take several months. Factor into your budget costs such as registration fees, insurance, and regular maintenance like oil changes.

Why File for Bankruptcy with Rising Interest Rates If you’re struggling with overwhelming debts made worse by increased interest rates, you may want to consider filing for Chapter13bankruptcy. Chapter13bankruptcy organizes your debts into a repayment plan that lasts three to five years.

Con: Chapter 7 bankruptcy stays on your credit report for 10 years. Chapter13bankruptcy: In this type of bankruptcy, you and the bankruptcy trustee make a structured plan to pay off a percentage of your debts over a 3-5 year payment plan under the court’s protection. 30% Amounts owed.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content