This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

If you’re at risk of losing your home, Chapter13bankruptcy could be your best option. When you’re going through the process of filing Chapter13, foreclosure cannot occur because you’re granted an automatic stay, meaning that lenders cannot pursue your debts and recover collateral, including your home.

When filing Chapter7 or Chapter13bankruptcy, it’s critical to understand the difference between consumer debt and non-consumer debt. If you’re considering filing Chapter7 or Chapter13bankruptcy, consider enlisting the help of skilled bankruptcy attorneys.

Your investment real estate’s outcome depends entirely on whether you file for Chapter7 or Chapter13bankruptcy. Investment Real Estate in Chapter7Bankruptcy. Chapter7bankruptcy is a great option for those looking to discharge eligible debts. Chapter13 Cramdowns.

It’s a smart choice to file for Chapter13bankruptcy. Your bankruptcy plan will allow you to catch up on payments and settle your debts while giving you a chance to keep your home treasured belongings. If you have a job but you’re struggling to make your payments every month, Chapter13 can help.

Bankruptcy Code reserves certain opportunities for those who are least likely to be able to repay their debts any time soon. Unlike Chapter13bankruptcy, which is available to most Americans, Chapter7bankruptcy is only available to low-income filers.

What you will learn from reading this article: Facts about selling your home while going through bankruptcy. Details about Chapter7 and Chapter13Bankruptcies and your house. You will need the advice of an experienced bankruptcy attorney as soon as possible! Chapter7Bankruptcy.

You should get legal assistance from a knowledgeable bankruptcy attorney in Denver. The United States Bankruptcy Code governs both chapter7 and chapter13bankruptcy. Chapter7 (Liquidation). Such is one of the primary distinctions between Chapter7 and Chapter13bankruptcy.

If you earn a decent, steady paycheck but you’re still struggling to pay your debts on time, it may be worth considering filing for bankruptcy. Bankruptcy Code. This opportunity will allow you to benefit from the protections of the automatic stay and the issuance of a discharge at the end of the bankruptcy process.

However, we’ve provided some basic answers below to the question, “What is the difference between Chapter7, 11, and 13 when it comes to bankruptcy?” In This Piece Understand the Types of Bankruptcy How Do You Know Which Bankruptcy Type is Right for You? What Is Chapter 11 Bankruptcy?

Fortunately, Chapter13bankruptcy offers debt relief and a solution for stopping mortgage servicers from repossessing your home. Saving Your Home From Foreclosure Through Chapter13BankruptcyChapter13bankruptcy offers a solution if you’ve fallen behind on monthly mortgage payments.

If you’re in a financial bind, your best option might be to seek a fresh start through Chapter7bankruptcy. In most cases, you don’t forfeit your home when you file for Chapter7bankruptcy. What is Chapter7Bankruptcy? What if I Have More Property Than You Can Exempt in a Chapter7?

You must qualify to file for bankruptcy, and your income must meet an income means test. If you do not qualify for a Chapter7bankruptcy to liquidate your debts, you may be required to pay back a significant portion of your debts under a Chapter13Bankruptcy, and still suffer the negative impact to your credit score.

Many people keep control over their assets through the use of bankruptcy exemptions, which are special rules that allow people who are filing for a Chapter7bankruptcy to keep certain property if its value is less than the amount of the exemption. How Do I Protect My Home During Bankruptcy? This is rarely true.

When homeowners face the daunting prospect of foreclosure, understanding the defensive options available can potentially help them preserve their homes and financial stability. For example, two common types of bankruptcy , Chapter7 and Chapter13, offer different benefits and drawbacks in the context of foreclosure.

Bankruptcy will wipe out credit card debt, medical bills, and personal loans, but will not eliminate primary obligation debt; things like student loans, child and spousal support, and newer tax debt. Bankruptcy can also stop or delay a home or mortgage foreclosure, stop collection actions, stop garnishments and lawsuits.

If you’re considering filing for bankruptcy, you’re not alone; roughly 375,000 people filed for bankruptcy in 2022, and home foreclosure filings rose 115% in 2022 over the number of foreclosures in 2021. To many people, the most alarming thing about filing for bankruptcy is the possibility that they will lose their home.

When you are struggling to pay your bills, there may come a point where you are faced with deciding between bankruptcy vs foreclosure. If you choose bankruptcy, there are also different options depending on whether you choose a Chapter13bankruptcy or a Chapter7bankruptcy.

Filing Again After Chapter7Bankruptcy. If you plan to file again after previously filing a Chapter7bankruptcy the following time limits apply. Filing Successive Chapter7Bankruptcy Cases. Filing Chapter13 After a Chapter7Bankruptcy.

Filing Again After Chapter7Bankruptcy. If you plan to file again after previously filing a Chapter7bankruptcy the following time limits apply. Filing Successive Chapter7Bankruptcy Cases. Filing Chapter13 After a Chapter7Bankruptcy.

Because of this, filing for bankruptcy is often one of the only options you may have. Below, we’ll break down how gambling debt fits into Chapter13bankruptcy and how you can prepare if gambling bankruptcy is the next step that you need to take. Can You File for Bankruptcy Due to Gambling Debt?

Chapter7 Timeshare Bankruptcies If you file for Chapter7bankruptcy , you might be able to keep your timeshare. Timeshares usually don’t have equity and won’t be sold by the trustee in a Chapter7bankruptcy. The lender will then ask the court for permission to foreclose on it.

Chapter7bankruptcy , or liquidation bankruptcy, allows you to discharge all or most of your debt. Under Chapter7, most people can keep their home and car, if desired, and receive automatic court protection from creditors. Chapter7bankruptcy also stops lawsuits and wage garnishments.

If that’s not possible for you, another option is to avoid it through Chapter7 or Chapter13bankruptcy court. Here’s how that works: Chapter7 If you successfully file for Chapter7bankruptcy , you receive protection from creditors and a discharge of most debt.

Some situations in which an individual may want to consider filing for emergency bankruptcy include: Wage garnishment Creditors levying your bank accounts or property An impending home foreclosure sale Imminent car repossession. It’s not always clear when it’s the right time to file for emergency bankruptcy.

This means a foreclosure, repossession, garnishment, or other action can continue against your spouse even after you’re freed of it through bankruptcy – but only if their name is on the debt. Ask your bankruptcy attorney about applicable exemptions. You’ll also need to choose between Chapter7 or Chapter13bankruptcy.

Defining the Most Common Types of Bankruptcy Before diving into bankruptcy’s implications for your nest egg, here is an explanation of the two most common types of bankruptcy. Chapter7bankruptcy or liquidation bankruptcy, allows you to discharge all or most of your debt.

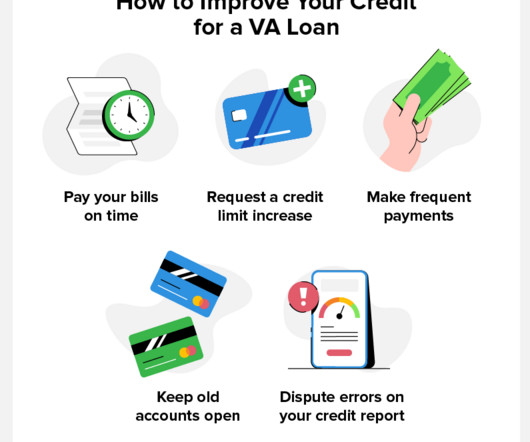

Compensating Factors Your Lender May Take Into Account Other VA Loan Requirements How to Get a VA Loan After Bankruptcy or Foreclosure Who Qualifies for a VA Loan? Here’s an overview of how to get a loan after foreclosure or bankruptcy. The waiting period for a Chapter13bankruptcy is 12 months after filing.

Cosigner Responsibilities: Bankruptcy and Debt Collection If a primary borrower declares bankruptcy, the co-signer associated with the debt may be responsible to pay back creditors, but this will depend on the type of bankruptcy that the primary debtor filed.

You can work directly with the mortgage lender on a loan modification, or reach out to the Colorado Foreclosure Hotline for free assistance. To speak with a Colorado attorney experienced in debt relief and bankruptcy, call The Law Office of Clark Daniel Dray at (303) 900-8598 or use the tool below to scheduled a free consultation.

If you’re worried about garnishments, foreclosures , lawsuits, repossessions , or other consequences of your debt, connect with an experienced bankruptcy lawyer at Sawin & Shea as soon as possible. A bankruptcy attorney helps someone clarify and organize their finances while getting most types of debt discharged.

Whether you’re facing foreclosure , repossession, wage garnishments, or relentless creditor harassment, our expertise in bankruptcy law can offer the protection and relief you’ve been seeking. One of our firm’s key strengths lies in our comprehensive understanding of both Chapter7 and Chapter13bankruptcy options.

It basically serves as a legally binding promise that the person filing for bankruptcy will resume making payments in full and on time to the creditor. Entering a reaffirmation agreement is a way that debtors in a Chapter7bankruptcy keep collateral attached to secured debt like houses or cars.

However, because assets do not secure these debts, bankruptcy may help eliminate them. To qualify for Chapter7bankruptcy, debtors must pass a means test that compares their income to their state’s median income. When you file for bankruptcy, you enter a legal process. This means you no longer owe the money.

Many people ask, when should you file for bankruptcy? You can file for bankruptcy in two different ways: Chapter7 and Chapter13. Filing for Chapter7bankruptcy centers on liquidating assets, while Chapter13bankruptcy focuses on reorganization.

There are officially six separate categories of bankruptcy , each designated after a specific section of federal bankruptcy law. However, Chapter7 and Chapter13bankruptcy are the two types of bankruptcy that are most frequently filed. What Benefits Can I Get from Filing for Bankruptcy?

Foreclosures and Short Sales: Seven Years A foreclosure can remain on your credit reports for seven years from the date the foreclosure was filed. The same goes for a short sale, which could show up on your credit report as a charge-off, a settlement, a deed-in-lieu of foreclosure, or “settled for less than the full amount due.”

The complexities of bankruptcy law, coupled with the potential consequences of a failed case, strongly suggest seeking the assistance of a qualified bankruptcy attorney for the best possible outcome. We can help you file for Chapter13bankruptcy or Chapter7bankruptcy, depending on your needs.

Myth #2: If I file for bankruptcy, my home, car, and personal property will be taken. A planned foreclosure or repossessed property can be prevented right away with either a Chapter7bankruptcy or a Chapter13bankruptcy. Myth #3: You can never obtain a loan or a mortgage.

In short, they prepare you for the challenges that come with rebuilding your finances after bankruptcy. Understanding Chapter7 vs. Chapter13Bankruptcy There are 6 types of bankruptcy, but two of the most common types are Chapter7 and Chapter13.

How to know which kind you need Bankruptcy is an issue that had a lot of negative social stigma attached to it; however, nowadays, many people understand that they can use bankruptcy to resolve unpaid debt and lay the groundwork for a stronger financial future. Your lenders must agree to the alternative payment plans.

What’s the Difference Between Chapter7 and Chapter13? Put simply, Chapter7 is a liquidation while Chapter13 is about reorganization. In the case of a Chapter7bankruptcy , the court appoints a trustee who is in charge of selling off (liquidating) a debtor’s non-exempt assets.

Detailed information about your property, collateralized debt, other debts, contracts, codebtors, income, expenses, and financial affairs must be provided accurately in the relevant sections of the bankruptcy form. What Information Does a Bankruptcy Form Need? You can start over because of that.

You can begin gathering information right now by scheduling a free consultation with one of the experienced bankruptcy attorneys at Bond & Botes. We can alleviate your stress!

Filing for Chapter13bankruptcy can help you improve your financial situation. Unfortunately, not everyone filing Chapter13 will complete the repayment process. Unfortunately, not everyone filing Chapter13 will complete the repayment process.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content