This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Filing for chapter13bankruptcy can seem like a daunting task, but it’s often the right move for those who are facing foreclosure, repossession, or have exorbitant debts. If you’re thinking of filing for chapter13bankruptcy, you may have questions regarding how it will impact your credit score.

Although sometimes borrowers can receive a forbearance or work out a repayment plan with their lenders, many are unable to reach this agreement, meaning they’re at risk of losing their homes. If you’re at risk of losing your home, Chapter13bankruptcy could be your best option. What Is Chapter13Bankruptcy?

Chapter13bankruptcy offers the option of lien stripping. If you’re filing or considering filing for Chapter13, you need to be aware of the process and advantages of lien stripping. Chapter13 lien stripping can be beneficial to your financial situation and may even help you save your home.

There are few life events as stressful as a foreclosure. However, there are ways to prevent foreclosure, even if you can’t afford your mortgage payments. In this blog, we’ll share details about loan modification, who is eligible, how to obtain one to stop foreclosure, and how a lawyer for foreclosure can help.

Chapter13bankruptcy offers the option of lien stripping. If you’re filing or considering filing for Chapter13, you need to be aware of the process and advantages of lien stripping. Chapter13 lien stripping can be beneficial to your financial situation and may even help you save your home.

It may only take a few months of missed payments to motivate your lender to foreclose on your home. Once foreclosure starts, you need to act quickly or risk losing everything you have invested in your home. After he fell behind on his mortgage, the lender eventually decided to foreclose.

When filing Chapter 7 or Chapter13bankruptcy, it’s critical to understand the difference between consumer debt and non-consumer debt. If you’re considering filing Chapter 7 or Chapter13bankruptcy, consider enlisting the help of skilled bankruptcy attorneys. What is Consumer Debt?

What you will learn from reading this article: Facts about selling your home while going through bankruptcy. Details about Chapter 7 and Chapter13Bankruptcies and your house. You will need the advice of an experienced bankruptcy attorney as soon as possible! Chapter13Bankruptcy.

When homeowners face the daunting prospect of foreclosure, understanding the defensive options available can potentially help them preserve their homes and financial stability. For example, two common types of bankruptcy , Chapter 7 and Chapter13, offer different benefits and drawbacks in the context of foreclosure.

Consider your income, assets, creditors, expenditures, and your ability to pass the means test while selecting between Chapter13 and Chapter 7. You should get legal assistance from a knowledgeable bankruptcy attorney in Denver. The United States Bankruptcy Code governs both chapter 7 and chapter13bankruptcy.

Why File for Bankruptcy with Rising Interest Rates If you’re struggling with overwhelming debts made worse by increased interest rates, you may want to consider filing for Chapter13bankruptcy. Chapter13bankruptcy organizes your debts into a repayment plan that lasts three to five years.

When you are struggling to pay your bills, there may come a point where you are faced with deciding between bankruptcy vs foreclosure. If you choose bankruptcy, there are also different options depending on whether you choose a Chapter13bankruptcy or a Chapter 7 bankruptcy.

With the COVID-19 foreclosure moratoriums over, housing foreclosures are once again on the rise nationally. In fact, in September of 2023, we saw home foreclosures on the rise by a whopping 18.4% Foreclosures in Indianapolis have also been increasingly more common. from this time last year.

Though enacting the CARES Act helped, those dealing with hefty mortgage payments and considering bankruptcy, for example, weren’t entirely clear on their options. Due to the CARES Act, lenders must allow this forbearance if borrowers meet the two conditions listed above.

If you do not qualify for a Chapter 7 bankruptcy to liquidate your debts, you may be required to pay back a significant portion of your debts under a Chapter13Bankruptcy, and still suffer the negative impact to your credit score. Auto lenders could also waive payments for those impacted by COVID-19.

It may only take a few months of missed payments to motivate your lender to foreclose on your home. Once foreclosure starts, you need to act quickly or risk losing everything you have invested in your home. After he fell behind on his mortgage, the lender eventually decided to foreclose.

If you can no longer afford the monthly payments, you can surrender your timeshare when you declare bankruptcy. In this case, the property will go back to the lender. Chapter 7 Timeshare Bankruptcies If you file for Chapter 7 bankruptcy , you might be able to keep your timeshare.

Many creditors such as mortgage servicers, auto lenders, and credit card companies are offering assistance to individuals financially affected by the pandemic. Unlike mortgage lenders, most landlords are simply not in a financial position to weather the loss of rental income due to the high expenses associated with the rental property itself.

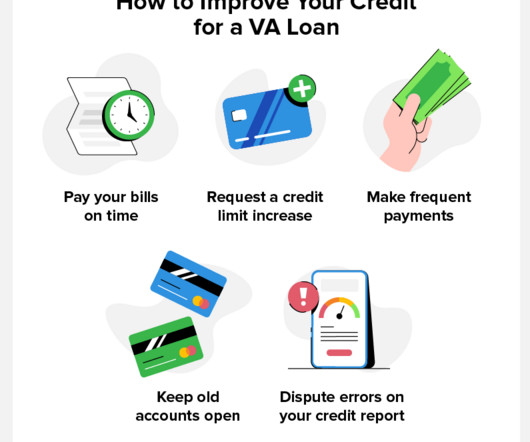

While there is no minimum requirement, most lenders prefer a credit score of 620 or above. While VA loans are typically easier to get approval for than conventional loans, private lenders still have certain requirements you must meet. VA lenders generally look for a minimum credit score of 620.

Lenders don’t necessarily continue to report activity for the entire limit. Foreclosures and Short Sales: Seven Years A foreclosure can remain on your credit reports for seven years from the date the foreclosure was filed. This allows borrowers to comparison-shop lenders.

Chapter13 , or reorganization bankruptcy, stops repossessions and foreclosures so you can save your home or investment. Like Chapter 7, it stops lawsuits and garnishments. Chapter13 can help people keep assets that might be at risk in a Chapter 7.

When a borrower applies for a loan or credit card, the lender will assess their creditworthiness by looking at their income, credit score, and debt-to-income ratio. If the lender is concerned about the borrower’s ability to repay the debt, they may require a co-signer. Considering Filing for Bankruptcy?

In the event that your loan doesn’t offer a plan or you’re not approved, a Chapter13Bankruptcy will stop a foreclosure and give you 5 years to get caught up on your mortgage arrears while potentially wiping out other debt like credit cards and medical bills. There are options available to you to prevent foreclosure.

Even after a law was passed in 2018 to prohibit creditors from reporting liens to credit bureaus , lenders can still search for judgments using public records, making it harder to get a job or a loan. If that’s not possible for you, another option is to avoid it through Chapter 7 or Chapter13bankruptcy court.

Though enacting the CARES Act helped, those dealing with hefty mortgage payments and considering bankruptcy, for example, weren’t entirely clear on their options. Due to the CARES Act, lenders must allow this forbearance if borrowers meet the two conditions listed above.

Through a legal process called bankruptcy, some people who are unable to pay their debts can start over financially, either temporarily or permanently. Since the effects are severe and long-lasting, bankruptcy is typically seen as the last option for managing debt. Do Bankruptcies Come in Different Types?

Reaffirming Debt in Chapter13BankruptcyChapter13bankruptcy involves consolidating your different forms of debt into a three-to-five-year repayment plan. There is a Chapter13 Plan that controls how various debts are treated. Next, the judge will assign a bankruptcy trustee to your case.

Whether you’re facing foreclosure , repossession, wage garnishments, or relentless creditor harassment, our expertise in bankruptcy law can offer the protection and relief you’ve been seeking. One of our firm’s key strengths lies in our comprehensive understanding of both Chapter 7 and Chapter13bankruptcy options.

The following are some of the most common bankruptcy myths in Littleton, Colorado: Myth #1: Short sales and loan modifications are viable alternatives to bankruptcy. Some people hope to stay out of bankruptcy by selling their homes or requesting a loan modification. Yet, fewer than 10% of these efforts succeed.

This means the lender can take no property, like a house or car if you do not pay. Instead, lenders rely on your promise to pay back the money. Chapter 7 bankruptcy remains on credit reports for 10 years. Unsecured Debts in Chapter13BankruptcyChapter13bankruptcy works differently.

How to know which kind you need Bankruptcy is an issue that had a lot of negative social stigma attached to it; however, nowadays, many people understand that they can use bankruptcy to resolve unpaid debt and lay the groundwork for a stronger financial future. Your lenders must agree to the alternative payment plans.

Unsecured debt would include things like: Medical bills Credit card bills Utility bills Back rent Personal loans At the end of the bankruptcy process, the remaining balances for these types of unsecured debts will likely be forgiven. A Chapter13 plan can cure arrearages on houses or cars, stopping foreclosures and repossessions.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content