This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Filing for chapter13bankruptcy can seem like a daunting task, but it’s often the right move for those who are facing foreclosure, repossession, or have exorbitant debts. If you’re thinking of filing for chapter13bankruptcy, you may have questions regarding how it will impact your credit score.

If you’re at risk of losing your home, Chapter13bankruptcy could be your best option. When you’re going through the process of filing Chapter13, foreclosure cannot occur because you’re granted an automatic stay, meaning that lenders cannot pursue your debts and recover collateral, including your home.

There are few life events as stressful as a foreclosure. However, there are ways to prevent foreclosure, even if you can’t afford your mortgage payments. One of those methods is through a loan modification. What is foreclosure? Your lender will then notify you that you are in default and begin foreclosure proceedings.

Chapter13bankruptcy offers the option of lien stripping. If you’re filing or considering filing for Chapter13, you need to be aware of the process and advantages of lien stripping. Chapter13 lien stripping can be beneficial to your financial situation and may even help you save your home.

Filing for Chapter13bankruptcy can provide much-needed relief if you are overwhelmed with debt and struggling to keep up with payments. Under Chapter13, you repay a portion or all of your debt, allowing you to keep assets like your home or car. What Is Chapter13Bankruptcy?

When filing Chapter 7 or Chapter13bankruptcy, it’s critical to understand the difference between consumer debt and non-consumer debt. If you’re considering filing Chapter 7 or Chapter13bankruptcy, consider enlisting the help of skilled bankruptcy attorneys. What is Consumer Debt?

Chapter13bankruptcy offers the option of lien stripping. If you’re filing or considering filing for Chapter13, you need to be aware of the process and advantages of lien stripping. Chapter13 lien stripping can be beneficial to your financial situation and may even help you save your home.

Filing for Chapter13bankruptcy can help you improve your financial situation. Unfortunately, not everyone filing Chapter13 will complete the repayment process. Unfortunately, not everyone filing Chapter13 will complete the repayment process.

It’s a smart choice to file for Chapter13bankruptcy. Your bankruptcy plan will allow you to catch up on payments and settle your debts while giving you a chance to keep your home treasured belongings. If you have a job but you’re struggling to make your payments every month, Chapter13 can help.

It could even help you to save a home that is at risk of foreclosure. Certainly, filing for bankruptcy isn’t the best debt management or debt solution for all consumers. If you are simply struggling to pay your mortgage but are not yet behind on your payment schedule by much, negotiating a loan modification may be a better option.

Your investment real estate’s outcome depends entirely on whether you file for Chapter 7 or Chapter13bankruptcy. Investment Real Estate in Chapter 7 Bankruptcy. Chapter 7 bankruptcy is a great option for those looking to discharge eligible debts. Chapter13 Cramdowns.

Whether or not you file for bankruptcy also depends on the kind of debt you have. Bankruptcy will wipe out credit card debt, medical bills, and personal loans, but will not eliminate primary obligation debt; things like student loans, child and spousal support, and newer tax debt. What does each one mean?

Fortunately, Chapter13bankruptcy offers debt relief and a solution for stopping mortgage servicers from repossessing your home. An adjustable-rate mortgage is a home loan that features variable payments. This differs from fixed-rate mortgages, where debtors pay a set interest rate for the entirety of the loan.

Raising interest rates typically slows down the economy as well as the rate of inflation, but these rates have a direct impact on people’s ability to obtain new loans. Here’s what you need to know about getting a new loan and interest rate after bankruptcy. Usually, this is cents on the dollar.

Consider your income, assets, creditors, expenditures, and your ability to pass the means test while selecting between Chapter13 and Chapter 7. You should get legal assistance from a knowledgeable bankruptcy attorney in Denver. The United States Bankruptcy Code governs both chapter 7 and chapter13bankruptcy.

When homeowners face the daunting prospect of foreclosure, understanding the defensive options available can potentially help them preserve their homes and financial stability. For example, two common types of bankruptcy , Chapter 7 and Chapter13, offer different benefits and drawbacks in the context of foreclosure.

If you do not qualify for a Chapter 7 bankruptcy to liquidate your debts, you may be required to pay back a significant portion of your debts under a Chapter13Bankruptcy, and still suffer the negative impact to your credit score. Federally managed student loans received an automatic six-month payment waiver.

When you are struggling to pay your bills, there may come a point where you are faced with deciding between bankruptcy vs foreclosure. If you choose bankruptcy, there are also different options depending on whether you choose a Chapter13bankruptcy or a Chapter 7 bankruptcy.

In This Piece Understand the Types of Bankruptcy How Do You Know Which Bankruptcy Type is Right for You? What Is Chapter 11 Bankruptcy? What Is Chapter 7 Bankruptcy? What Is Chapter13Bankruptcy? Should You File for Bankruptcy? What Is Chapter13Bankruptcy?

With the COVID-19 foreclosure moratoriums over, housing foreclosures are once again on the rise nationally. In fact, in September of 2023, we saw home foreclosures on the rise by a whopping 18.4% Foreclosures in Indianapolis have also been increasingly more common. from this time last year.

have a federally backed HUD/FHA, VA, USDA, Fannie Mae, or Freddie Mac loan. *If Outside of Bankruptcy: For those not dealing with bankruptcy, the CARES Act allows those affected by the pandemic to ask for forbearance to suspend payments on their federally-backed mortgage loan for up to six months.

Because of this, filing for bankruptcy is often one of the only options you may have. Below, we’ll break down how gambling debt fits into Chapter13bankruptcy and how you can prepare if gambling bankruptcy is the next step that you need to take. Can You File for Bankruptcy Due to Gambling Debt?

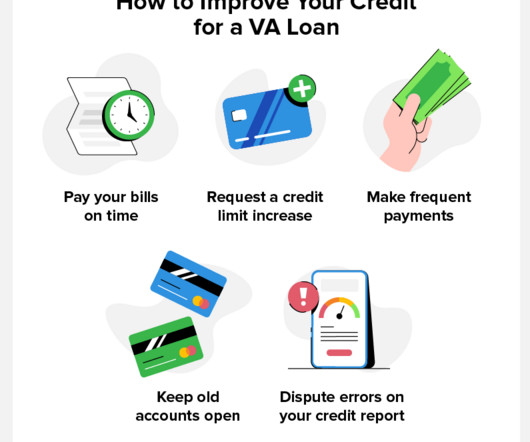

A VA home loan is a mortgage backed by the Department of Veterans Affairs (VA) for service members, veterans, and their families. The purpose of VA loans is to help veterans purchase homes with lower interest rates and better terms. Read on to learn how to get a VA loan with bad credit. What Are the Benefits of a VA Loan?

This means each spouse is only responsible for their partner’s debt if they have voluntarily joined the debt, for example by co-signing on a loan. If you file bankruptcy without your spouse, they won’t be on the hook for any debts that aren’t in their name. Ask your bankruptcy attorney about applicable exemptions.

So far the offers have been vague, the most likely concessions will be for your lenders on your home and cars to allow you to move a monthly payment to the end of the loan and for credit cards to temporarily reduce your interest rate. There are more tools for dealing with your mortgage than any other type of loan. Student Loans.

Don’t hire an out-of-state “law firm” to modify your loan – there are a number of free options you can take advantage of by contacting your loan servicer directly. The tools available to you depend on the type of mortgage loan you have, so please find the correct option below. Fannie Mae. Freddie Mac. VA-guaranteed.

Co-signers are beneficial for those seeking to obtain loans and credit cards. If you have a co-signer associated with your debt or if you are a co-signer, you need to be aware of how financial liability works and what happens when the primary debtor declares bankruptcy. Plus, being a co-signer can help a debtor build credit.

One of the most significant consequences is the damage it can cause to your credit score, making it challenging to secure loans or obtain credit in the future. If that’s not possible for you, another option is to avoid it through Chapter 7 or Chapter13bankruptcy court.

Do Bankruptcies Come in Different Types? There are officially six separate categories of bankruptcy , each designated after a specific section of federal bankruptcy law. However, Chapter 7 and Chapter13bankruptcy are the two types of bankruptcy that are most frequently filed.

Charge-Offs: Seven Years Accounts you didn’t pay, like a charged-off credit card or installment loan balance, can stay on your credit report for seven years from the date the debt was charged off. Foreclosures and Short Sales: Seven Years A foreclosure can remain on your credit reports for seven years from the date the foreclosure was filed.

Whether you’re facing foreclosure , repossession, wage garnishments, or relentless creditor harassment, our expertise in bankruptcy law can offer the protection and relief you’ve been seeking. One of our firm’s key strengths lies in our comprehensive understanding of both Chapter 7 and Chapter13bankruptcy options.

have a federally backed HUD/FHA, VA, USDA, Fannie Mae, or Freddie Mac loan. *If Outside of Bankruptcy: For those not dealing with bankruptcy, the CARES Act allows those affected by the pandemic to ask for forbearance to suspend payments on their federally-backed mortgage loan for up to six months.

Credit cards, medical bills, and personal loans make up most unsecured debt that bankruptcy can eliminate. Some debts stay with you even after bankruptcy. Student loans, child support, recent taxes, and court fines must be paid in full. Chapter 7 bankruptcy remains on credit reports for 10 years.

If you’re worried about garnishments, foreclosures , lawsuits, repossessions , or other consequences of your debt, connect with an experienced bankruptcy lawyer at Sawin & Shea as soon as possible. A bankruptcy attorney helps someone clarify and organize their finances while getting most types of debt discharged.

Chapter13bankruptcy sets up a 3-5 year repayment plan to pay back a portion of what you owe. The Pros Bankruptcy can stop foreclosures , repossessions, lawsuits, wage garnishment, utility shut-offs, and debt collection activities through its automatic stay provision.

At the Law Office of Clark Daniel Dray (debtfreecolorado), you can be sure that a bankruptcy attorney will inform and educate you about the myths about bankruptcy in Littleton, CO. These are the five most prevalent bankruptcy myths. Short sales and loan modifications are viable alternatives to bankruptcy.

A reaffirmation agreement is a document that re-obligates a debtor to repay a particular debt, such as a car loan, mortgage, or other loan type. It basically serves as a legally binding promise that the person filing for bankruptcy will resume making payments in full and on time to the creditor.

Medical bills, credit cards, payday loans, and struggling businesses – it can seem like the letters and calls from creditors will never stop. Bankruptcy filings for both individuals and businesses are on the rise. Since 2005, a debtor education course from an approved provider is mandatory for anyone who files for bankruptcy.

Many people ask, when should you file for bankruptcy? You can file for bankruptcy in two different ways: Chapter 7 and Chapter13. Filing for Chapter 7 bankruptcy centers on liquidating assets, while Chapter13bankruptcy focuses on reorganization.

Detailed information about your property, collateralized debt, other debts, contracts, codebtors, income, expenses, and financial affairs must be provided accurately in the relevant sections of the bankruptcy form. What Information Does a Bankruptcy Form Need? Two of the most typical collateralized loans are mortgages and auto loans.

Unsecured debt would include things like: Medical bills Credit card bills Utility bills Back rent Personal loans At the end of the bankruptcy process, the remaining balances for these types of unsecured debts will likely be forgiven. The two most common examples of secured debt are mortgages and auto loans.

The increase in lawsuits filed against consumers for unpaid medical debt, credit card bills, automobile loans and other collection issues comes as no surprise to attorneys and others working in the industry. However, over the past several years, the civil courts in most states have been overrun by debt collection cases against consumers.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content