This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Although sometimes borrowers can receive a forbearance or work out a repayment plan with their lenders, many are unable to reach this agreement, meaning they’re at risk of losing their homes. If you’re at risk of losing your home, Chapter 13 bankruptcy could be your best option. What Is Chapter 13 Bankruptcy?

When filing Chapter7 or Chapter 13 bankruptcy, it’s critical to understand the difference between consumer debt and non-consumer debt. If you’re considering filing Chapter7 or Chapter 13 bankruptcy, consider enlisting the help of skilled bankruptcy attorneys.

If you are struggling to pay your mortgage and other bills, the good news is that the CARES Act (Coronavirus Relief and Economic Security) has extended the deadline for when the foreclosure moratorium is due to expire. You will need the advice of an experienced bankruptcy attorney as soon as possible! Chapter7Bankruptcy.

When you are struggling to pay your bills, there may come a point where you are faced with deciding between bankruptcy vs foreclosure. If you choose bankruptcy, there are also different options depending on whether you choose a Chapter 13 bankruptcy or a Chapter7bankruptcy.

You should get legal assistance from a knowledgeable bankruptcy attorney in Denver. The United States Bankruptcy Code governs both chapter7 and chapter 13 bankruptcy. Chapter7 (Liquidation). Advantages of Chapter7Bankruptcy. Disadvantages of Chapter7Bankruptcy.

When homeowners face the daunting prospect of foreclosure, understanding the defensive options available can potentially help them preserve their homes and financial stability. For example, two common types of bankruptcy , Chapter7 and Chapter 13, offer different benefits and drawbacks in the context of foreclosure.

You must qualify to file for bankruptcy, and your income must meet an income means test. If you do not qualify for a Chapter7bankruptcy to liquidate your debts, you may be required to pay back a significant portion of your debts under a Chapter 13 Bankruptcy, and still suffer the negative impact to your credit score.

If you can no longer afford the monthly payments, you can surrender your timeshare when you declare bankruptcy. In this case, the property will go back to the lender. Chapter7 Timeshare Bankruptcies If you file for Chapter7bankruptcy , you might be able to keep your timeshare.

Many creditors such as mortgage servicers, auto lenders, and credit card companies are offering assistance to individuals financially affected by the pandemic. Unlike mortgage lenders, most landlords are simply not in a financial position to weather the loss of rental income due to the high expenses associated with the rental property itself.

This is when a lender agrees to take less than the total amount owed on the real estate from the sale. Your lender has to approve the short sale and will require quite a bit of documentation and paperwork from you. Your lender has to approve the short sale and will require quite a bit of documentation and paperwork from you.

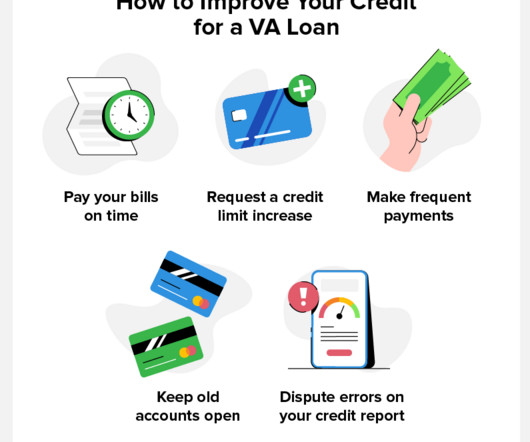

While there is no minimum requirement, most lenders prefer a credit score of 620 or above. While VA loans are typically easier to get approval for than conventional loans, private lenders still have certain requirements you must meet. VA lenders generally look for a minimum credit score of 620.

Lenders don’t necessarily continue to report activity for the entire limit. Foreclosures and Short Sales: Seven Years A foreclosure can remain on your credit reports for seven years from the date the foreclosure was filed. This allows borrowers to comparison-shop lenders.

It basically serves as a legally binding promise that the person filing for bankruptcy will resume making payments in full and on time to the creditor. Entering a reaffirmation agreement is a way that debtors in a Chapter7bankruptcy keep collateral attached to secured debt like houses or cars.

Chapter7bankruptcy , or liquidation bankruptcy, allows you to discharge all or most of your debt. Under Chapter7, most people can keep their home and car, if desired, and receive automatic court protection from creditors. Chapter7bankruptcy also stops lawsuits and wage garnishments.

When a borrower applies for a loan or credit card, the lender will assess their creditworthiness by looking at their income, credit score, and debt-to-income ratio. If the lender is concerned about the borrower’s ability to repay the debt, they may require a co-signer. Considering Filing for Bankruptcy?

Whether you’re facing foreclosure , repossession, wage garnishments, or relentless creditor harassment, our expertise in bankruptcy law can offer the protection and relief you’ve been seeking. One of our firm’s key strengths lies in our comprehensive understanding of both Chapter7 and Chapter 13 bankruptcy options.

Even after a law was passed in 2018 to prohibit creditors from reporting liens to credit bureaus , lenders can still search for judgments using public records, making it harder to get a job or a loan. If that’s not possible for you, another option is to avoid it through Chapter7 or Chapter 13 bankruptcy court.

The backing of the federal government makes FHA loans a bit easier to qualify for because they’re considered less risky for lenders. Requirements for conventional loans vary by lender, but on average you’ll need a credit score of around 640. A conventional loan is not. FHA loans do tend to be more forgiving.

This means the lender can take no property, like a house or car if you do not pay. Instead, lenders rely on your promise to pay back the money. However, because assets do not secure these debts, bankruptcy may help eliminate them. When you file for bankruptcy, you enter a legal process. What is Unsecured Debt?

What’s the Difference Between Chapter7 and Chapter 13? Put simply, Chapter7 is a liquidation while Chapter 13 is about reorganization. In the case of a Chapter7bankruptcy , the court appoints a trustee who is in charge of selling off (liquidating) a debtor’s non-exempt assets.

The following are some of the most common bankruptcy myths in Littleton, Colorado: Myth #1: Short sales and loan modifications are viable alternatives to bankruptcy. Some people hope to stay out of bankruptcy by selling their homes or requesting a loan modification. Yet, fewer than 10% of these efforts succeed.

Because debtors require sufficient cash to operate their businesses and pay for the administrative expenses of the chapter 11 process, many seek interim court approval for financing (called “debor-in-possession” or “DIP” financing) and/or the use cash collateral that is subject to a secured creditor’s lien. Walton, Jr.’s

The following list explains the differences between Chapter7 and Chapter 13 bankruptcies, which can help you determine which type would be best in certain circumstances: The main difference between Chapter7 and Chapter 13 is that the latter is more of a repayment program while the former typically involves complete liquidation of nonexempt assets.

Through a legal process called bankruptcy, some people who are unable to pay their debts can start over financially, either temporarily or permanently. Since the effects are severe and long-lasting, bankruptcy is typically seen as the last option for managing debt. Chapter7 is known as liquidation in bankruptcy legislation.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content