This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When you’re going through the process of filing Chapter 13, foreclosure cannot occur because you’re granted an automatic stay, meaning that lenders cannot pursue your debts and recover collateral, including your home. What Is Chapter 13 Bankruptcy? Can I Stop Foreclosure with Chapter 13 Bankruptcy?

When filing Chapter7 or Chapter 13 bankruptcy, it’s critical to understand the difference between consumer debt and non-consumer debt. If you’re considering filing Chapter7 or Chapter 13 bankruptcy, consider enlisting the help of skilled bankruptcy attorneys.

Your investment real estate’s outcome depends entirely on whether you file for Chapter7 or Chapter 13 bankruptcy. Investment Real Estate in Chapter7Bankruptcy. Chapter7bankruptcy is a great option for those looking to discharge eligible debts. Chapter 13 Cramdowns.

Chapter7bankruptcy may seem intimidating, but as you can tell from the following infographic, the steps that go into successfully completing your case are pretty straightforward. For those of you who may not be able to view the image, the text follows: Chapter7Bankruptcy Timeline. 13 bankruptcy.

You should get legal assistance from a knowledgeable bankruptcy attorney in Denver. The United States Bankruptcy Code governs both chapter7 and chapter 13 bankruptcy. Chapter7 (Liquidation). Advantages of Chapter7Bankruptcy. Disadvantages of Chapter7Bankruptcy.

When you are struggling to pay your bills, there may come a point where you are faced with deciding between bankruptcy vs foreclosure. If you choose bankruptcy, there are also different options depending on whether you choose a Chapter 13 bankruptcy or a Chapter7bankruptcy.

When homeowners face the daunting prospect of foreclosure, understanding the defensive options available can potentially help them preserve their homes and financial stability. For example, two common types of bankruptcy , Chapter7 and Chapter 13, offer different benefits and drawbacks in the context of foreclosure.

However, we’ve provided some basic answers below to the question, “What is the difference between Chapter7, 11, and 13 when it comes to bankruptcy?” In This Piece Understand the Types of Bankruptcy How Do You Know Which Bankruptcy Type is Right for You? What Is Chapter 11 Bankruptcy?

You must qualify to file for bankruptcy, and your income must meet an income means test. If you do not qualify for a Chapter7bankruptcy to liquidate your debts, you may be required to pay back a significant portion of your debts under a Chapter 13 Bankruptcy, and still suffer the negative impact to your credit score.

courts have nicknamed Chapter 13 bankruptcy the “wage earner’s plan.”. What Is A Chapter 13 Repayment Plan? Chapter 13 is a personal reorganization bankruptcy. In a Chapter 13 you do not have to repay most debts in full. Every Chapter 13 repayment plan is unique and is based on your individual situation.

An adjustable-rate mortgage is a home loan that features variable payments. This differs from fixed-rate mortgages, where debtors pay a set interest rate for the entirety of the loan. Chapter 13 reorganizes your debt into a three-to-five-year repayment plan. What Is an Adjustable-Rate Mortgage?

You may be considering Chapter7bankruptcy. Consulting with a Chapter7bankruptcy attorney in Boulder, CO, can help determine if it is the right solution. Our blog will provide a general overview of Chapter7bankruptcy. Filing for Chapter7bankruptcy triggers an automatic stay.

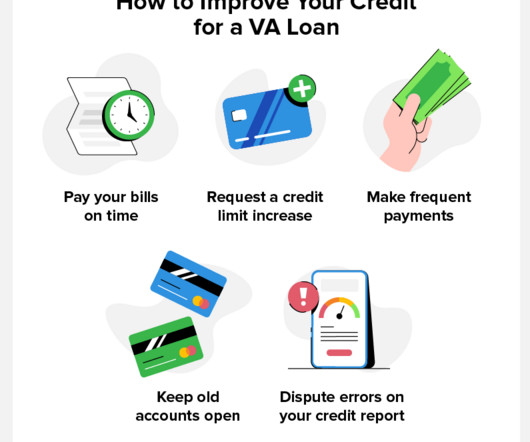

A VA home loan is a mortgage backed by the Department of Veterans Affairs (VA) for service members, veterans, and their families. The purpose of VA loans is to help veterans purchase homes with lower interest rates and better terms. Read on to learn how to get a VA loan with bad credit. What Are the Benefits of a VA Loan?

Two common loan options are conventional and FHA loans. A Federal Housing Administration loan, or FHA loan, is insured by the federal government. A conventional loan is not. The backing of the federal government makes FHA loans a bit easier to qualify for because they’re considered less risky for lenders.

Whether or not you file for bankruptcy also depends on the kind of debt you have. Bankruptcy will wipe out credit card debt, medical bills, and personal loans, but will not eliminate primary obligation debt; things like student loans, child and spousal support, and newer tax debt. What does each one mean?

So far the offers have been vague, the most likely concessions will be for your lenders on your home and cars to allow you to move a monthly payment to the end of the loan and for credit cards to temporarily reduce your interest rate. There are more tools for dealing with your mortgage than any other type of loan. Student Loans.

Whether you’re facing foreclosure , repossession, wage garnishments, or relentless creditor harassment, our expertise in bankruptcy law can offer the protection and relief you’ve been seeking. One of our firm’s key strengths lies in our comprehensive understanding of both Chapter7 and Chapter 13 bankruptcy options.

If you earn a decent, steady paycheck but you’re still struggling to pay your debts on time, it may be worth considering filing for bankruptcy. Bankruptcy Code. This opportunity will allow you to benefit from the protections of the automatic stay and the issuance of a discharge at the end of the bankruptcy process.

For the lender, it’s all about the bottom line, and if they think they can get more money from a foreclosure, they won’t agree to a short sale. Even if the lender does forgive the amount of the loan not paid upon closing, you may be taxed on this money by the IRS. What if you file for Chapter7bankruptcy?

A reaffirmation agreement is a document that re-obligates a debtor to repay a particular debt, such as a car loan, mortgage, or other loan type. It basically serves as a legally binding promise that the person filing for bankruptcy will resume making payments in full and on time to the creditor.

One of the most significant consequences is the damage it can cause to your credit score, making it challenging to secure loans or obtain credit in the future. If that’s not possible for you, another option is to avoid it through Chapter7 or Chapter 13 bankruptcy court. Do You Have a Judgment Lien Against You?

Co-signers are beneficial for those seeking to obtain loans and credit cards. If you have a co-signer associated with your debt or if you are a co-signer, you need to be aware of how financial liability works and what happens when the primary debtor declares bankruptcy. Plus, being a co-signer can help a debtor build credit.

Charge-Offs: Seven Years Accounts you didn’t pay, like a charged-off credit card or installment loan balance, can stay on your credit report for seven years from the date the debt was charged off. Foreclosures and Short Sales: Seven Years A foreclosure can remain on your credit reports for seven years from the date the foreclosure was filed.

Chapter 13 bankruptcy allows people with regular income to develop debt repayment plans to discharge their eligible debts over 3 to 5 years. This is different from Chapter7bankruptcy which liquidates assets to pay back debts but does not involve a structured repayment plan.

Many people ask, when should you file for bankruptcy? You can file for bankruptcy in two different ways: Chapter7 and Chapter 13. Filing for Chapter7bankruptcy centers on liquidating assets, while Chapter 13 bankruptcy focuses on reorganization.

Credit cards, medical bills, and personal loans make up most unsecured debt that bankruptcy can eliminate. Some debts stay with you even after bankruptcy. Student loans, child support, recent taxes, and court fines must be paid in full. However, because assets do not secure these debts, bankruptcy may help eliminate them.

What’s the Difference Between Chapter7 and Chapter 13? Put simply, Chapter7 is a liquidation while Chapter 13 is about reorganization. In the case of a Chapter7bankruptcy , the court appoints a trustee who is in charge of selling off (liquidating) a debtor’s non-exempt assets.

At the Law Office of Clark Daniel Dray (debtfreecolorado), you can be sure that a bankruptcy attorney will inform and educate you about the myths about bankruptcy in Littleton, CO. These are the five most prevalent bankruptcy myths. Short sales and loan modifications are viable alternatives to bankruptcy.

If you’re worried about garnishments, foreclosures , lawsuits, repossessions , or other consequences of your debt, connect with an experienced bankruptcy lawyer at Sawin & Shea as soon as possible. A bankruptcy attorney helps someone clarify and organize their finances while getting most types of debt discharged.

This means each spouse is only responsible for their partner’s debt if they have voluntarily joined the debt, for example by co-signing on a loan. If you file bankruptcy without your spouse, they won’t be on the hook for any debts that aren’t in their name. This is good news for Indiana residents.

There are officially six separate categories of bankruptcy , each designated after a specific section of federal bankruptcy law. However, Chapter7 and Chapter 13 bankruptcy are the two types of bankruptcy that are most frequently filed. Chapter7 is known as liquidation in bankruptcy legislation.

Medical bills, credit cards, payday loans, and struggling businesses – it can seem like the letters and calls from creditors will never stop. Bankruptcy filings for both individuals and businesses are on the rise. Since 2005, a debtor education course from an approved provider is mandatory for anyone who files for bankruptcy.

Detailed information about your property, collateralized debt, other debts, contracts, codebtors, income, expenses, and financial affairs must be provided accurately in the relevant sections of the bankruptcy form. What Information Does a Bankruptcy Form Need? Two of the most typical collateralized loans are mortgages and auto loans.

Unfortunately, not everyone filing Chapter 13 will complete the repayment process. If the bankruptcy court has your Chapter 13 bankruptcy dismissed, you’ll need to refile or find another method for overcoming your debts, such as Chapter7bankruptcy.

For example, while the Bankruptcy Code allows for a DIP loan to prime the lien of an existing secured creditor, the secured creditor must receive “adequate protection” that its position will not be diminished as a result of the use of cash collateral or new financing. He can be reached at (313) 965-9038 or jwalton@fraserlawfirm.com.

The increase in lawsuits filed against consumers for unpaid medical debt, credit card bills, automobile loans and other collection issues comes as no surprise to attorneys and others working in the industry. However, over the past several years, the civil courts in most states have been overrun by debt collection cases against consumers.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content