This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The background: The lawsuit was filed after the defendant, a servicing corporation, sent two letters to the plaintiff concerning his residential mortgage loan. The plaintiff, who had previously filed for Chapter7bankruptcy, had received a discharge order.

Filing Chapter7bankruptcy provides numerous Indiana residents with debt relief. Fortunately, the vast majority of Chapter7 filers are able to retain all of their property while also discharging their debts. Indiana Chapter7Bankruptcy Exemptions.

If you’re struggling with overwhelming debts, Chapter7bankruptcy could be your best option. Chapter7 is the most common form of bankruptcy for individuals and families, and it allows you to discharge many of your unsecured debts within only a few months. What is Chapter7Bankruptcy?

When a consumer in Tennessee has more debt than they can manage, bankruptcy may be the solution. Consumers commonly choose Chapter7bankruptcy, which allows them to erase certain debts, but filing for bankruptcy can impact credit scores. Chapter7bankruptcy and credit scores.

When filing for bankruptcy, you can discharge certain types of personal loans, meaning that you’re no longer legally responsible for paying off the debt. If you’re considering filing for bankruptcy, you need to know what personal loans you can discharge and which filing method best suits your financial situation.

When filing Chapter7 or Chapter 13 bankruptcy, it’s critical to understand the difference between consumer debt and non-consumer debt. If you’re considering filing Chapter7 or Chapter 13 bankruptcy, consider enlisting the help of skilled bankruptcy attorneys.

When faced with insurmountable debts, Chapter7bankruptcy can be the best way to regain control over your financial situation. Importantly, Chapter7bankruptcy provides an opportunity for a fresh start. Typically, a Chapter7bankruptcy case will conclude within six months.

A chapter7bankruptcy is one of the most common routes individuals take in discharging their debt. One thing people are often not sure of is just exactly what debts are covered under this chapter. . Chapter7bankruptcy discharges unsecured debts. personal loans (excluding a mortgage and auto loan)

At Sawin & Shea, LLC, our Chapter7Bankruptcy lawyers have helped clients just like you in the Indianapolis and surrounding areas. What is Chapter7Bankruptcy? When you file a Chapter7bankruptcy, it is only your unsecured debts that will be eligible for discharge.

Chapter7bankruptcy is also known as the “fresh start” bankruptcy. The basics of Chapter7bankruptcy. Under the blanket of Chapter7bankruptcy, you can expect to have some big bills charged off. These include tax bills, student loans, and child support.

You have made it through Chapter7bankruptcy. But how do you qualify for a mortgage loan after Chapter7bankruptcy? The post How To Qualify for a Mortgage After Chapter7Bankruptcy appeared first on Cleveland Ohio Bankruptcy Attorneys. Congratulations!

Say goodbye to credit card stresssee if Chapter7bankruptcy is your solution. Chapter7bankruptcy can help clear debt and give you a fresh start. A Greenwood Colorado bankruptcy attorney can explain your options and make sure you dont risk losing assets you want to keep.

If you are thinking of filing for Chapter7bankruptcy, below are some tips you might want to consider beforehand. It is important to review all your debts before filing for bankruptcy. You want to have a complete list so that everything can be listed in the bankruptcy proceedings. Analyze your debts.

Many people assume that because they have filed bankruptcy, their credit is ruined, and they will not be able to qualify for any loans. There are a number of steps you can take to improve your credit score and to make it likely that you can be approved for a loan. This is not true. More on both of those below.).

In this article, we will walk you through Indiana debt collection laws and some of the many exemptions that help you keep your personal, real, or intangible assets when you file for a Chapter7 in the State of Indiana. What is Chapter7Bankruptcy? The post What Can I Keep if I File For Chapter7Bankruptcy?

Chapter7bankruptcy may seem intimidating, but as you can tell from the following infographic, the steps that go into successfully completing your case are pretty straightforward. For those of you who may not be able to view the image, the text follows: Chapter7Bankruptcy Timeline. 13 bankruptcy.

Your investment real estate’s outcome depends entirely on whether you file for Chapter7 or Chapter 13 bankruptcy. Investment Real Estate in Chapter7Bankruptcy. Chapter7bankruptcy is a great option for those looking to discharge eligible debts.

Many college graduates in Tennessee are struggling with student loan repayments, and you might be among them. Is public service loan forgiveness for you? Is public service loan forgiveness for you? However, the program has been plagued with problems. Challenges in dealing with the program. One part of the debt puzzle.

A bankruptcy can be a good way to get your financial health back on track, but it also comes with some limitations. It may make it so it’s harder for you to get credit or loans in the future, at least for a few years. If you do need a personal loan after your Chapter7 or Chapter 13 bankruptcy, it may be possible to get it.

When faced with insurmountable debts, Chapter7bankruptcy can be the best way to regain control over your financial situation. Importantly, Chapter7bankruptcy provides an opportunity for a fresh start. Typically, a Chapter7bankruptcy case will conclude within six months.

People who have too much debt and can’t make payments often declare bankruptcy to help relieve them of their financial obligations. Otherwise, too much debt can hamper the ability to take on loans. Here’s what you should know: What is Chapter7bankruptcy? What is Chapter 13 bankruptcy?

A common question we receive from those considering bankruptcy is how it impacts personal guarantees. If you’re considering filing for bankruptcy, you need to consult with a bankruptcy attorney before signing a personal guarantee. A personal guarantee loan is a signed agreement stating that you’re liable for a debt.

You should get legal assistance from a knowledgeable bankruptcy attorney in Denver. The United States Bankruptcy Code governs both chapter7 and chapter 13 bankruptcy. Chapter7 (Liquidation). Advantages of Chapter7Bankruptcy. Disadvantages of Chapter7Bankruptcy.

Code § 525 – Protection against discriminatory treatment) it is illegal to fire someone simply because they have filed for bankruptcy. The bankruptcy would cause an automatic stay, preventing creditors from continuing to attempt to collect debts while you continue with your case.

What Is Chapter 13 Bankruptcy? You’ve likely heard about Chapter7 and Chapter 13 bankruptcy — as they are the most common types and are available to individuals — but how do they differ? If you’re eligible to file under Chapter7 and only have unsecured debts, this may be your best course of action.

However, we’ve provided some basic answers below to the question, “What is the difference between Chapter7, 11, and 13 when it comes to bankruptcy?” In This Piece Understand the Types of Bankruptcy How Do You Know Which Bankruptcy Type is Right for You? What Is Chapter 11 Bankruptcy?

If you are thinking of filing for Chapter7 or Chapter 13 bankruptcy, or if you have already filed, you may be concerned about how long the bankruptcy will stay on your credit report. The situation is more complicated with Chapter 13 bankruptcy. Create a budget and build an emergency fund.

At the same time, you may have student loan and credit card debt that is more than you can afford. If your debt has reached a crisis level, you may want to consider filing for bankruptcy. Chapter7bankruptcy may help to clear away much of the credit card and student debt that you took on while you were at school.

You must qualify to file for bankruptcy, and your income must meet an income means test. If you do not qualify for a Chapter7bankruptcy to liquidate your debts, you may be required to pay back a significant portion of your debts under a Chapter 13 Bankruptcy, and still suffer the negative impact to your credit score.

Even though bankruptcy can affect your credit score for up to a decade after you’ve filed, that doesn’t mean that you cannot get a car loan. Actually, your credit score will likely be higher after bankruptcy than before you filed. Bankruptcy gives you a chance to essentially start over and rebuild your credit again.

Chapter7bankruptcy is a great financial solution for those struggling with debt, especially unsecured debts. With Chapter7bankruptcy, you as the debtor can discharge most unsecured obligations after liquidating nonexempt assets. What Is Chapter7Bankruptcy?

Myth: Bankruptcy ruins your credit forever—or at least an entire decade. The truth: Bankruptcies are considered public records, which is how they’re reported on your credit. The public record associated with a Chapter7bankruptcy will remain on your credit report for as long as 10 years.

The majority of people in Indiana who have thought about declaring bankruptcy likely already know how challenging it is to get student loans erased. Although it is not impossible, debtors normally need to pass the Brunner test, which establishes that repaying the student loans will put them in an unreasonably difficult position.

Filing for Chapter7bankruptcy can be an effective way to eliminate a variety of unsecured business or personal debts. Let’s take a look at some specific reasons why you may want to pursue a liquidation bankruptcy. Generally speaking, retirement funds are exempt from creditors in a bankruptcy proceeding.

You may be considering Chapter7bankruptcy. Consulting with a Chapter7bankruptcy attorney in Boulder, CO, can help determine if it is the right solution. Our blog will provide a general overview of Chapter7bankruptcy. Filing for Chapter7bankruptcy triggers an automatic stay.

Two common loan options are conventional and FHA loans. A Federal Housing Administration loan, or FHA loan, is insured by the federal government. A conventional loan is not. The backing of the federal government makes FHA loans a bit easier to qualify for because they’re considered less risky for lenders.

Court of Appeals for the Second Circuit ruled that private student loans are not explicitly exempt from a debtor’s Chapter7bankruptcy discharge. In Homadian , the borrower, after graduating from Emerson College, filed for Chapter7bankruptcy in 2007 and obtained a discharge in 2009.

However, dealing with financial hardships like bankruptcy can make that dream seem out of reach. But, Can You Buy a House After Chapter7 with a Co-Signer? If you’ve gone through a Chapter7bankruptcy , you may be wondering if homeownership is still possible for you, especially if your credit has taken a major hit.

For example, it may be harder for you to be approved for loans or credit after filing. If you need a personal loan after filing for bankruptcy , it may be approved. The amount of time it will take to get the loan depends on the type of bankruptcy you choose and how long it has been since you filed.

For example, a Chapter7 to another Chapter7bankruptcy typically has an 8-year wait time. Or, a Chapter7 to a Chapter 13 bankruptcy may require people to wait 4 years. What is liquidation bankruptcy? Liquidation bankruptcy is another name for Chapter7bankruptcy.

And student loan payments are often even a burden for senior citizens today. Unfortunately, all of this adds up to bankruptcy—something that is already scary to deal with as is but can be even more overwhelming and frightening for seniors. Pensions have also mostly disappeared or have become significantly underfunded.

Student loans are one of the primary ways graduates build up debt. Graduates may have received grants and awards to help pay for their education, but many have student loans hanging over their heads. Graduates may have received grants and awards to help pay for their education, but many have student loans hanging over their heads.

An adjustable-rate mortgage is a home loan that features variable payments. This differs from fixed-rate mortgages, where debtors pay a set interest rate for the entirety of the loan. This differs from Chapter7bankruptcy because debtors are at risk of losing their homes during the Chapter7 liquidation process.

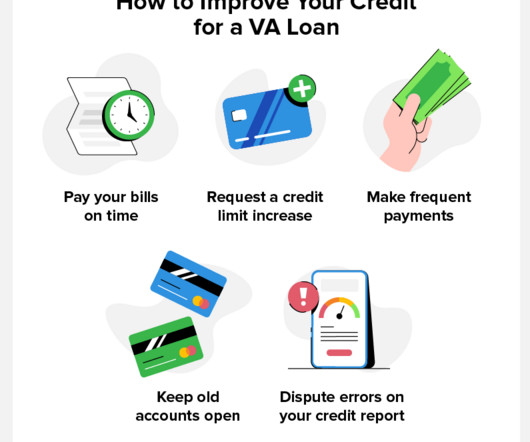

A VA home loan is a mortgage backed by the Department of Veterans Affairs (VA) for service members, veterans, and their families. The purpose of VA loans is to help veterans purchase homes with lower interest rates and better terms. Read on to learn how to get a VA loan with bad credit. What Are the Benefits of a VA Loan?

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content