This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Appeals Court Affirms Ruling Over Default Judgment The Court of Appeals for the Eighth Circuit has upheld a ruling in favor of a defendant that was sued for violating the Fair Debt Collection Practices Act, deciding that a default judgment obtained in state court is conclusive from the perspective of establishing the facts of a case.

This approach involves taking proactive measures, even when the credit is still in good standing, and the creditor has not yet taken possession of the collateral. This categorisation is pivotal in effectively monitoring the collateral portfolio and ensuring consistent practices when performing valuation calculations.

These receivables are usually B2B accounts that require commercial debt collection. A collection agency with its three-step collection process can assist businesses to recover money in an amicable manner. Need a collections agency for your business: Contact us. Written Notices sent by a Collection Agency.

When a borrower applies for a loan, most lenders require the borrower to pledge an asset as security for the repayment of the loan, i.e. collateral. In the event the borrower defaults, usually by failing to make loan payments, a secured creditor has a right to take possession of the collateral. 679.609, Fla. 2d 1020, 1024 (Fla.

Any secured creditor, large or small, may encounter a situation in which it is preferable to retain or recover the collateral in a transaction without having to sell the collateral itself. However, many will be unaware of the precise procedure and requirements for retaining the collateral itself. 679.609(1).

When a small business association (“SBA”) loan is converted to liquidation status, the lender must begin liquidating the collateral. The “Recoverable Value” is “the net dollar amount that a prudent lender could reasonably expect to recover by liquidating a particular piece of collateral.” See SOP 50 57. Liquidation Methods.

Site visits allow lenders and CDCs to gain a first-hand impression of the borrower’s business operations, evaluate risks, and inventory the collateral. Frequent site visits help lenders and CDCs make prudent lending decisions by keeping them up-to-date with the condition of the collateral and the borrower’s business operations.

THE NEW ERA OF CONSUMER LENDING In today ’ s rapidly evolving financial landscape, the significant increase in consumer lending presents new challenges for financial institutions, particularly in managing collections.

How Do Property Taxes Result in Loss of Collateral? If the borrower is delinquent in paying its property taxes, a tax certificate may be sold for the past-due taxes, which could lead to a tax deed sale of the collateral. Next, on the sale date, the tax collector will sell a tax certificate for the amount of taxes due. 197.432.

When a small business association (“SBA”) loan is converted to liquidation status, the lender must begin liquidating the collateral. If the collateral is real property, the lender must liquidate all parcels of real property that has a Recoverable Value over $10,000. See SOP 50 57.

Unsecured loans are loans that don’t have collateral. Common unsecured loans include: Bank loans with no collateral. Unlike unsecured personal loans, secured loans involve some form of collateral that the lender can repossess if the borrower fails to make payments. Payday loans. Signature loans.

Before liquidating any collateral or incurring costs of litigation, Lenders and CDCs should make a good faith effort to first negotiate a “workout agreement” with the borrower. 60 calendar days), the lender/CDC must move forward with liquidating the collateral. SOP 50 57 2; SOP 50 55. See SOP 50 57 2 ; SOP 50 55.

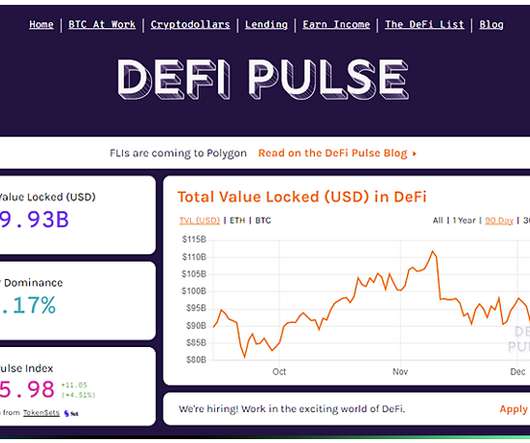

DeFi is a collective term for financial products and services that are accessible to anyone who can use Ethereum over the internet. DeFi markets allow users to borrow cryptocurrencies on margin using other digital assets as collateral. DeFi Apps are built on the Ethereum blockchain. List of contents. What is DeFi? What exactly is DeFi?

If your objective of telling a creditor you are filing for bankruptcy is to stop collections or buy more time, you may not get what you hope for. Instead, they may rush the collection process or convince you not to declare bankruptcy, which may worsen your situation.

When talking about the concept of online personal loans, it’s important to touch on the differences between secured and unsecured loans: Secured loans are those where collateral is put up to secure the loan. For instance, a home would act as collateral in a mortgage or home equity line of credit (HELOC).

If the borrower is unable to pay the full amount owed on an SBA loan after all of the collateral has been liquidated, the borrower may submit an “offer in compromise.” An offer in compromise is appropriate when the borrower’s business has closed down and all of the collateral has been liquidated. SOP 50 57 2; SOP 50 55.

This means that lenders and authorized CDC liquidators must liquidate and conduct debt collection litigation in a “prompt, cost-effective and commercially reasonable manner, consistent with prudent lending standards, and in accordance with loan program requirements.” Further collection efforts are not cost effective or practical; and.

Instead of having to wait 30, 60, or 90 days for your customers to satisfy their invoices per your terms, you can collect the money immediately. And because your invoices provide the collateral, you don’t need to worry about putting assets in jeopardy. You Can Offload Invoice Collection Responsibilities.

The lender can try to collect the money from you, including by suing you. If you sign one, it has two potential entities to chase to collect the loan. First, the lender will attempt to collect from the business itself. Your business doesn’t have enough income or collateral. The benefits to the lender are pretty big.

Lenders and CDC’s are responsible for monitoring each SBA loan in their portfolio to mitigate the risk of loss because after the loan has closed, changes may occur that can impact the ability to administer or collect on the loan. REO and acquired personal property collateral. 120.535(a). 120.535(b).

Understanding the automatic stay's role in bankruptcy The automatic stay is a temporary order that halts actions by creditors to collect debts from the person who has declared bankruptcy. It prevents any form of harassment, foreclosure and nearly all other collection actions.

If collection agents like me are calling you, you need to reduce your debt. To avoid your account being sent to collections, you need to find ways to reduce your debt. Debts secured with collateral might make it impossible for you to run your business if you lost the equipment. Collect on unpaid invoices.

Thus, timely debt collection is crucial for every business. Therefore, it is vital to have a robust debt collection strategy to enable you to stabilise your cash flow and acquire money from your debtors without hampering your business relationships. Collection methods are not real-time. Contacting wrong people.

Lenders will usually be faced with two situations: (1) the mobile home existed at the time of the mortgage, and is identified in the mortgage documents as collateral; or (2) the mobile home did not exist at the time of the mortgage, and is not identified in the mortgage documents as collateral. (1)

Recoverable Expenses” are defined as SBA approved, necessary, reasonable, and customary costs incurred to collect and enforce the terms of the Loan Documents, or to preserve or dispose of collateral. What Expenses are Recoverable. Recoverable Expenses can be added to the principal balance of the loan. See SOP 50 51 3.

Court of Appeals for the Ninth Circuit held that a debt collector’s mistake about the time-barred status of a debt under state law can qualify as a bona fide error within the meaning of the Fair Debt Collection Practices Act. In Kaiser v.

The INCAA survey also found that medical debts were most likely to be in collections. Out of the reported debt statistics, 35% of all debts in collections were medical, which surpassed other forms of debt. 25% of debts in collections were credit card related, and 20% were student loan debts.

Environmental Investigations are required, for example, before a lender or CDC can acquire the title to commercial real property collateral by purchasing it at a foreclosure sale or accepting a deed-in-lieu of foreclosure, or taking over the operation of a borrower’s business that uses a hazardous substance. What Are Environmental Risks?

Security interests offer you an advantage if the buyer defaults, forcing you to pursue debt collection remedies. Consider how a bank or alternative lender works: if collateralized, a loan is made based on the collateral of a borrower. The borrower, in return for the loan, pledges assets or other capital to secure the loan.

Winning your case in court is often the easy part of the legal debt collection process; it’s collecting your payment post-judgment where things get challenging and require a bit of strategy. When that does not happen, we pursue collateral approaches. Cohen LLC come into play. Finding Your Debtor’s Assets.

By choosing to enlist the help of a debt collection law firm you can take advantage of a number of different debt collection options to assist in the collection of monies owed to you. Collection attorneys work as a “legal” agency. Most collection attorneys will handle all phases of the debt collection process.

The experienced collection attorneys at the Law Offices of Alan M. Collection agencies are passive organizations that make the same effort you were making before you brought them on board. Why Hire a Collections Attorney? An experienced collections attorney will do more than merely advise you on what you need to do.

This paperwork starts your Chapter 7 case and pauses most collection efforts against you. This means you are no longer legally responsible for them, and creditors cant try to collect from you. File Your Bankruptcy Petition Once youve completed credit counseling, youll need to file a petition with the bankruptcy court in your area.

In broad terms, if a debt is secured, it means it is backed up by collateral property. If a debt is unsecured, no collateral is put up as a guarantee to pay. They may use collection agencies , or they may sue you (asking the court to garnish wages, take an asset, or put a lien on your home). What is the difference?

To identify the best solution for Non-Performing Loans (NPLs) , stakeholders such as lenders, servicers, and debt collection agencies need to deploy all available tools, starting a thorough appraisal of the NPL portfolio via a dedicated Workout Unit. A significant factor to consider is regulatory compliance.

An automatic stay prevents creditors and lenders from collecting debt or collateral on protected assets. When it comes to filing Chapter 13, your consumer and non-consumer debt classifications determine what is and isn’t protected by an automatic stay. With consumer debts, co-debtors receive the protection of an automatic stay.

When faced with this dilemma, don’t further waste your time and efforts chasing your debtor, spend your time making money and leave your bad debt recovery to the experienced and aggressive collections attorneys at the Law Offices of Alan M. The relentless collection lawyers at the Law Offices of Alan M. Cohen LLC. . Sheriff Sales.

The court found that the lender properly filed a foreclosure action on both mortgages in just Pinellas County because both mortgages jointly constituted the collateral for a single loan. Flagship Cmty Bank , 96 So. 3d 452 (Fla. 2d DCA 2012) , the loan was secured by two mortgages: one in Pinellas County and the other in Hillsborough County.

Secured debts are a type of debt backed by an asset that is used as collateral. To enforce secured debts, your creditors may repossess your car or other vehicles, they may foreclose on your mortgage, or levy against other property you have either pledged as collateral or that is subject to an involuntary lien. What is Secured Debt?

The new rule specifically excludes charges based solely on a borrower’s individual behavior after the extension of credit that cannot reasonably be predicted at the time of the NM-APR disclosure, such as: Actual expenditures, including reasonable attorney fees, for legal process or proceedings to collect on a loan pursuant to statutory limitation; (..)

Therefore, if the foreclosing lender buys the collateral at the foreclosure sale, it should obtain title insurance because it is possible that the sale could be invalidated and the collateral returned to the borrower’s ownership. 702.036(2). When Can the Foreclosure Sale Be Invalidated? 90 CWELT-2008 LLC v. Conclusion.

Credit cards are unsecured loans, meaning you do not have to put down collateral to use the money. We can help you collect the money that others owe you, so that you do not have to rely on credit cards. Businesses often use credit cards in the same ways that people do in their personal lives. This is not necessarily a bad thing.

Consult with an attorney experienced in commercial debt collection to assess the viability of your case and guide you through the legal process. These actions can help secure the debt by leveraging their assets as collateral. Credit reporting: Report the debt to credit bureaus as a delinquent account.

It does include things like credit card payments, auto loans, medical bills, personal and payday loans, and any other collections you’re being assessed. Or you resorted to a loan using your car as collateral. Keep in mind that your ratio typically excludes mortgage and student loans. You could afford to shoulder more liability.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content