This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Lenders should be cognizant about what expenses are classified by the SBA as recoverable or non-recoverable. Recoverable Expenses” are defined as SBA approved, necessary, reasonable, and customary costs incurred to collect and enforce the terms of the Loan Documents, or to preserve or dispose of collateral. See SOP 50 51 3.

Lenders are responsible for servicing and liquidating all of the 7(a) loans in their portfolio. Lenders and CDC’s must be cognizant about their responsibilities and authority in servicing and liquidating SBA loans because failure to do so properly may lead to formal enforcement actions by the SBA Office of Credit Risk Management.

If a borrower defaults on a SBA loan, the lender or CDC must assess the environmental risk of contamination before conducting any liquidation action that could result in a loss, or otherwise increase the risk of loss, due to the actual or alleged presence of contamination. What Are Environmental Risks? SOP 50 10 5(E), Appendix 2.

When a borrower applies for a loan, most lenders require the borrower to pledge an asset as security for the repayment of the loan, i.e. collateral. In the event the borrower defaults, usually by failing to make loan payments, a secured creditor has a right to take possession of the collateral. 679.609, Fla. 2d 1020, 1024 (Fla.

Site visits allow lenders and CDCs to gain a first-hand impression of the borrower’s business operations, evaluate risks, and inventory the collateral. Frequent site visits help lenders and CDCs make prudent lending decisions by keeping them up-to-date with the condition of the collateral and the borrower’s business operations.

When a small business association (“SBA”) loan is converted to liquidation status, the lender must begin liquidating the collateral. Lenders must liquidate all personal property that has a Recoverable Value over $5,000. In Florida, the lender can choose from the following methods: UCC Sale. See SOP 50 57.

This may be troublesome for lenders because the property may then be sold for taxes, which will eliminate the lender’s mortgage lien. This may leave some lenders wondering how it can protect their mortgage interests, if the borrower is delinquent in paying its property taxes. How Do Property Taxes Result in Loss of Collateral?

When a small business association (“SBA”) loan is converted to liquidation status, the lender must begin liquidating the collateral. If the collateral is real property, the lender must liquidate all parcels of real property that has a Recoverable Value over $10,000. Is the Recoverable Value of the Property Over $10,000?

In the event a borrower is seriously delinquent on making payments under a SBA loan, or the SBA loan is classified in liquidation status, lenders and CDCs must develop a prudent and commercially reasonable strategy to maximize their recovery on the loan. 60 calendar days), the lender/CDC must move forward with liquidating the collateral.

Unsecured loans are loans that don’t have collateral. If you fail to repay an unsecured personal loan, the lender cannot repossess your assets. Common unsecured loans include: Bank loans with no collateral. Personal loans from lenders that you know, such as acquaintances, co-workers, employers, friends, and family.

If the borrower is unable to pay the full amount owed on an SBA loan after all of the collateral has been liquidated, the borrower may submit an “offer in compromise.” All borrowers must submit their own offer in compromise to the lender or CDC. SOP 50 57 ; SOP 50 55. SOP 50 57 2; SOP 50 55. When is an Offer in Compromise Appropriate?

When a SBA loan is in liquidation status, lenders and authorized CDC liquidators are required to perform “Prudent Liquidation.” When Prudent Liquidation is complete, it’s time for the lender or authorized CDC liquidator to submit a wrap-up report to the SBA and have the loan charged-off. 120.535(b). 120.535(b). SOP 50 55.

Online lenders make it easy to compare rates and terms and find the right online personal loan for your situation. That is, the lender advances you money that you pay back with interest over a predetermined period of time. This often allows digital lenders to streamline the applications. Benefits of Online Personal Loans.

The lender can try to collect the money from you, including by suing you. Why Would a Lender Require a Personal Guarantee? Personal guarantees are all about reducing risk for the lender. If you sign one, it has two potential entities to chase to collect the loan. The benefits to the lender are pretty big.

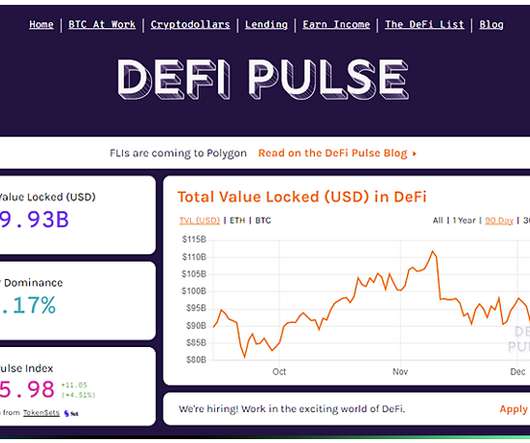

DeFi is a collective term for financial products and services that are accessible to anyone who can use Ethereum over the internet. A system that interacts buyers, sellers, borrowers, or lenders with peer-to-peer technology to access financial products or financial services bypassing middlemen such as financial institutions.

In Florida, lenders may find themselves foreclosing on real property with a mobile home attached to the land. On the other hand, if the mobile home is not retired and the lender has a perfected lien on the mobile home, the lender must use replevin in addition to the foreclosure. Is the Mobile Home Retired?

THE NEW ERA OF CONSUMER LENDING In today ’ s rapidly evolving financial landscape, the significant increase in consumer lending presents new challenges for financial institutions, particularly in managing collections.

Unfortunately, it also means that the car, truck, van or SUV that you drive to your job every day is also collateral for the loan used to purchase it. . When you fall behind on payments, the lender who financed the purchase might decide to repossess the vehicle. Bankruptcy stops foreclosure before the lender takes the vehicle.

Lenders need to be aware that borrowers and other lienholders can bring an action or proceeding to set aside, invalidate, or challenge the validity of a final judgment of foreclosure of a mortgage, even after the foreclosure sale. The property was acquired by a “person affiliated with” the foreclosing lender or the borrower.

However, lenders often wonder where they should file the foreclosure action if the loan is secured by mortgaged land situated in different counties. The court found that the lender properly filed a foreclosure action on both mortgages in just Pinellas County because both mortgages jointly constituted the collateral for a single loan.

Understanding the automatic stay's role in bankruptcy The automatic stay is a temporary order that halts actions by creditors to collect debts from the person who has declared bankruptcy. It prevents any form of harassment, foreclosure and nearly all other collection actions.

An automatic stay prevents creditors and lenders from collecting debt or collateral on protected assets. If you’re a co-signer or co-debtor on a business property, such as a rental home, the automatic stay doesn’t protect you from lenders, so they can repossess the property.

Despite objections from CUNA and NAFCU, the House of Representatives passed the Comprehensive Debt Collection Improvement Act on Thursday. While consumer groups praised the bill for its recourse for consumers harassed by debt collectors, CUNA and NAFCU saw the bill as complicating the legal relationship between consumers, members and lenders.

Unfortunately, it also means that the car, truck, van or SUV that you drive to your job every day is also collateral for the loan used to purchase it. . When you fall behind on payments, the lender who financed the purchase might decide to repossess the vehicle. Bankruptcy stops foreclosure before the lender takes the vehicle.

Sometimes, foreclosure of a commercial property is the only option available to lenders and servicers to limit losses as a result of defaults on hotel and restaurant mortgages. Parts 1-4 of this series discussed pre-foreclosure options available to lenders dealing with hotel/restaurant mortgage defaults. 702.015(4) , Fla. York, 903 So.

Security interests offer you an advantage if the buyer defaults, forcing you to pursue debt collection remedies. Consider how a bank or alternative lender works: if collateralized, a loan is made based on the collateral of a borrower. By taking security interest , you are technically taking a position as a lender.

This new legislation is likely to be important to lenders and borrowers due to the anticipated higher volume of commercial foreclosures due to economic effects of the current COVID-19 pandemic. sell, lease, license, exchange, collect, or otherwise dispose of receivership property.” § 714.02(14), of the Act.

Thus, timely debt collection is crucial for every business. Therefore, it is vital to have a robust debt collection strategy to enable you to stabilise your cash flow and acquire money from your debtors without hampering your business relationships. Collection methods are not real-time. Contacting wrong people.

Use the same formula that lenders rely on when evaluating a loan application. The result is a percentage that determines your creditworthiness – in short, if lenders believe you’ll be able to repay the loan. Here’s how the typical lender classifies debt-to-income ratio: Less than 15%: Your debt load is within an affordable range.

As discussed in parts 1-4 of this series, lenders have several options prior to instituting a commercial foreclosure action. Additionally, as briefly discussed in part 5 of this series, during the foreclosure action, lenders have options to try to preserve the value of the underlying collateral and to minimize further losses.

Secured debts are a type of debt backed by an asset that is used as collateral. For example, when you take out a home loan, you will be required to sign a mortgage which grants the lender a lien, or security interest against your home should you fall behind on payments. What is Secured Debt? Examples of Unsecured Debts.

In an adversary proceeding, the collective owners of the Makaha Valley Country Club , golf courses, surrounding undeveloped land, and other related assets (the “Owners”) avoided obligations undertaken in connection with a loan extension provided by Tianjin Dinghui Hongjun Equity Investment Partnership (the “Lenders”).

Many creditors such as mortgage servicers, auto lenders, and credit card companies are offering assistance to individuals financially affected by the pandemic. Unlike mortgage lenders, most landlords are simply not in a financial position to weather the loss of rental income due to the high expenses associated with the rental property itself.

An auto loan is a type of secured debt, which means it’s backed by collateral. In financial lingo, collateral is a valuable asset used to secure a loan. If you don’t pay the loan as agreed, the lender has the right to take back—repossess—the asset, sell it, and use the proceeds to cover your debt.

In broad terms, if a debt is secured, it means it is backed up by collateral property. If a debt is unsecured, no collateral is put up as a guarantee to pay. However, it is important to note that before bankruptcy is declared, lenders can still come after you to get you to pay off the unsecured debt. What is the difference?

Many lenders give borrowers a grace period before they technically consider the payment late. Lenders consider any payment not made within this allotted time frame a late payment. Since each lender has its own terms and conditions, it’s important to read the terms of your auto loan. So, how late can you be on a car payment?

Entering a reaffirmation agreement is a way that debtors in a Chapter 7 bankruptcy keep collateral attached to secured debt like houses or cars. All of the original terms of the loan are back in force, including the creditor’s right to repossess the collateral if you get behind on payments in the future.

Fees paid to a public official relating to the extension of credit, including fees to record liens, are excluded. As to loans of $500 or less, there is also an exclusion for a fee not exceeding five percent of the total principal of the loan if that fee is not imposed on any one borrower more than one time per 12-month period.

To identify the best solution for Non-Performing Loans (NPLs) , stakeholders such as lenders, servicers, and debt collection agencies need to deploy all available tools, starting a thorough appraisal of the NPL portfolio via a dedicated Workout Unit. A significant factor to consider is regulatory compliance.

In the wake of the Global Financial Crisis, lenders in several markets were presented with an almost unprecedented increase in bad debts accompanied by a sharp drop in property prices. This program was set up to help lenders establish loan modification criteria and provide terms that would allow customers to continue to service their debt.

Types of personal loans include: Installment Plan Payday Peer-to-Peer Lending Cosigner /Guarantor Debt Consolidation Variable Rate Fixed Rate During your bankruptcy proceeding, at least a portion of these loans will be discharged, whether you borrowed from brick-and-mortar or online lenders. Unsecured loans don’t have collateral.

An “automatic stay” is imposed as of the petition date, which prevents creditors from taking any further action, such as pursuing collection activity, related to a pre-petition debt. The debtor is required to serve all known creditors with notice of the commencement of the chapter 11 case. Proof-of-Claim Bar Date.

Chapter 7 Chapter 7 bankruptcy can eliminate most unsecured debts that aren’t secured by collateral, in the way that auto and home loans are. Although there are exceptions to this general rule, Chapter 7 might not be the best option for those concerned with foreclosure, although Chapter 13 could potentially provide a more viable solution.

Complete protection from creditors – This includes wage garnishment and debt collection. The lender protects the borrower against foreclosure. Unsecured debt is debt without collateral. Collateral guarantees debt repayment. A mortgage or car loan secures the lender’s interest in your house.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content