This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This approach involves taking proactive measures, even when the credit is still in good standing, and the creditor has not yet taken possession of the collateral. This categorisation is pivotal in effectively monitoring the collateral portfolio and ensuring consistent practices when performing valuation calculations.

While a “C” average may feel middle-of-the-road on an academic scale, nailing the five C’s of credit is the key to getting business funding from banks and other financialinstitutions. Jackie Zimmermann is a writer at NerdWallet. Email: articles@nerdwallet.com.

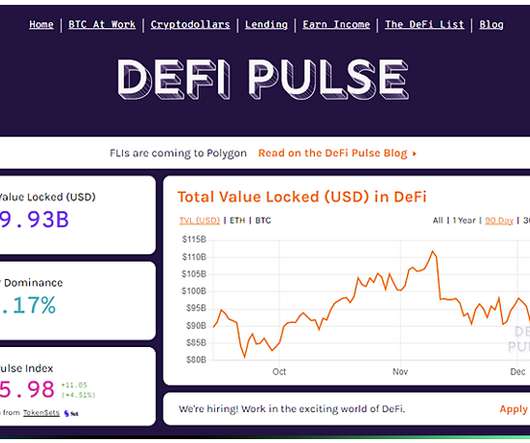

A system that interacts buyers, sellers, borrowers, or lenders with peer-to-peer technology to access financial products or financial services bypassing middlemen such as financialinstitutions. DeFi markets allow users to borrow cryptocurrencies on margin using other digital assets as collateral.

THE NEW ERA OF CONSUMER LENDING In today ’ s rapidly evolving financial landscape, the significant increase in consumer lending presents new challenges for financialinstitutions, particularly in managing collections. INTRODUCING QCR ACCELERATOR The QCR Accelerator is a collections solution developed by QUALCO.

When talking about the concept of online personal loans, it’s important to touch on the differences between secured and unsecured loans: Secured loans are those where collateral is put up to secure the loan. For instance, a home would act as collateral in a mortgage or home equity line of credit (HELOC).

Managing loan portfolios becomes a labyrinth for financialinstitutions in a financial ecosystem marked by unrelenting complexity and constant change. Consequently, financialinstitutions operate within an economy marked by contraction and sustained inflationary pressures.

Intercompany loans can have varied terms – including the amount borrowed, repayment schedule, collateral requirements, and so on. While financialinstitutions and banks factor such risk into their business model… A regular firm that lends within an intercompany loan arrangement may struggle to cope with such a financial setback.

On March 29, the New Mexico FinancialInstitutions Division of the Regulation and Licensing Department’s (NM FID) new rule on the New Mexico-Annual Percentage Rate (NM-APR) becomes effective.

No credit check to apply *Money added to Credit Builder will be held in a secured account as collateral for your Credit Builder Visa card, which means you can spend up to this amount on your card. Most secured credit cards require an initial qualifying deposit that acts as collateral and determines your credit limit. No annual fee.

Republican-appointee Commissioners Roisman and Peirce issued a statement on February 12 publicly disagreeing with Acting Chair Lee’s recent fiat discontinuing the Enforcement Division’s practice of proposing settlements that are contingent upon the Commission’s approval of waivers for collateral disqualifications arising from the settlement.

That’s because you provide all of the collateral for the loan in cash, so it’s not a risk for the lender. These are very similar to credit building loans, but they use funds you already had in savings as collateral. And if you’ve made all your payments on time, you’ve been successfully building your credit all along.

While it shouldn’t be overlooked that other criteria such as term lengths, repayment flexibility, down payments, and collateral are just as important to consider, one of the most important and obvious factors is the interest rate available with your loan. Seek Out Credit Unions or Community Banks.

Personal loans are installment loans offered by a bank, credit union, or other financialinstitution to an individual borrower. The former uses collateral, commonly in the form of your vehicle title, to secure repayment of the loan. The far more appealing choice, the unsecured personal loan, does not require any collateral.

Fair value – Hugely subjective right now, but any fair values of collateral that affect your ECL model will need to be revised as the market adjusts. Changes may impact your debt protections and customer recovery options in the event of a default.

Unsecured loans don’t have collateral. When seeking a new personal loan after bankruptcy, use legitimate lenders, such as major financialinstitutions, credit unions, or through Credit Karma. Before choosing your first personal loan, you need to understand the difference between secured and unsecured loans.

Instead of reviewing your credit history, the lender will consider other factors, such as your income and employment status or collateral, to get a secured loan. No-credit-check loans are commonly offered by payday lenders or other companies that offer extremely high interest rates or require you to put down something of value as collateral.

In his bankruptcy practice, Eric focuses on representing creditors, including financialinstitutions, special servicers, private equity groups, and other non-traditional lenders as well as other secured and unsecured creditors in state and federal court litigation, chapter 11 bankruptcy cases, and in out-of-court workouts and resolutions.

HB1027 will require registration with the commissioner of financialinstitutions for both sales-based financing providers and brokers by November 1, 2022. As a result, providers using that alternative model, which is not expressly addressed, must consider whether HB1027 applies. Who Will Be Required to Register?

Securitization is initiated when a financialinstitution pools together a group of assets. Asset-backed securities are initiated when a financialinstitution creates securities collateralized or backed by the cash flows generated from the underlying group of assets in the securitized pool.

UCC filings are the standard for placing liens against other businesses or individuals with collateralized agreements. In each of these instances, the collateral for the UCC will vary. For example, if a business is leasing equipment, the collateral for that particular UCC filing is the equipment that is being leased.

A personal loan is money borrowed from a bank, credit union, or other financialinstitution that can be used for virtually any personal expense. However, In the case of a secured loan, you’ll need collateral, such as a car or money in a savings account. What Is a Personal Loan? Do You Need a Down Payment for a Personal Loan?

At the beginning of the lockdowns a former colleague described the problem facing financialinstitutions as a ‘portfolio of good quality customers facing a temporary shock to their income, all they need is a bit of immediate assistance’.

Depending on the reason, they often do not require collateral. Credit Builder Loans : Credit builder loans are offered by some financialinstitutions. Personal Loans : Personal loans are generic installment loans that you can take out for many reasons. You put some money down in a savings account, and pay yourself back.

The Senate Banking Committee questioned Chopra on the CFPB’s oversight of financialinstitutions providing benefits under the Servicemembers Civil Relief Act (SCRA), medical debt collection, so-called “junk fees,” and the increasing popularity of buy now, pay later (BNPL) products.

financialinstitutions and corporations. On December 2, the Federal Reserve Board finalized clarifying and technical updates to its policy governing the provision of intraday credit to healthy depository institutions with accounts at the Federal Reserve Banks. The RFP industry working group is comprised of noteworthy U.S.

The clearing and settlement process was front and center at the House Financial Services Committee’s February 18, 2021 hearing over the GameStop (NYSE: “GME”) short-squeeze and Robinhood’s pause in GME trading. He has over 34 years of experience representing financialinstitutions in litigation, regulatory, and compliance matters.

On July 27, the Senate passed its version of the National Defense Authorization Act (NDAA) bill, which includes a provision that tightens oversight over financialinstitutions engaged in crypto trading and takes aim at crypto mixers and “anonymity-enhancing” crypto assets. For more information, click here.

“Banks, credit unions, and financialinstitutions use credit scores and other factors of your credit history to determine the borrower’s ability to repay the loan,” says David Haas, co-founder of PowerPay , a financial technology company that provides loans for home improvement projects.

“Banks, credit unions, and financialinstitutions use credit scores and other factors of your credit history to determine the borrower’s ability to repay the loan,” says David Haas, co-founder of PowerPay , a financial technology company that provides loans for home improvement projects.

Financialinstitutions in particular, given their central place in a nation’s economy, need to lead this digital connect. To be clear, this is not only about efficiency in lending. All of this enables businesses to invest more and expand. Many are already on the digital transformation journey and engaging in various partnerships.

Common reasons for bank account garnishment in Texas include: Private creditors: These are banks, credit unions, credit card companies, peer-to-peer lenders, hard money loan providers, and other financialinstitutions. This is submitted to the financialinstitution that will remit payment from the debtor’s bank accounts.

On December 15, the Office of the Comptroller of the Currency, along with the Federal FinancialInstitutions Examination Council, released revised procedures for how its examiners will investigate financialinstitutions for Fair Debt Collection Practices Act compliance, incorporating Regulation F changes into their review.

Financialinstitutions in particular, given their central place in a nation’s economy, need to lead this digital connect. To be clear, this is not only about efficiency in lending. All of this enables businesses to invest more and expand. Many are already on the digital transformation journey and engaging in various partnerships. “In

The clearing and settlement process was front and center at the House Financial Services Committee’s February 18, 2021 hearing over the GameStop (NYSE: “GME”) short-squeeze and Robinhood’s pause in GME trading. He has over 34 years of experience representing financialinstitutions in litigation, regulatory, and compliance matters.

All these personal loans are unsecured which means you don’t have to put up collateral. Bottom line: Your application on Fiona could lead to dozens of phone calls from a variety of financialinstitutions who know you’re in the market for a personal loan. These calls won’t go on forever.

We are committed to helping financialinstitutions deliver on their digital initiatives while meeting and exceeding customer expectations. In fact, the main attrition driver for financialinstitutions is a poor banking app. Read the full post: Report: 2022 Trends for Financial Services.

Small business loans are generally unsecured, so they are a bit riskier for financialinstitutions, but secured loans can provide confidence to lenders that may otherwise decline an application. Businesses need collateral for secured loans, which can come in different forms: Asset-backed loans. Commercial property loans.

However, while mortgages and auto loans, for example, are backed by collateral that likely eventually become a pure asset, credit card accounts are simply debt on a ledger. For example, mortgage debt would be positively correlated with the homeownership rate and home prices in respective states, which are again affected by state level income.”

Discover Personal Loans, provided by the same financialinstitution that backs Discover credit cards, offers a great loan for people who want to pay off high-interest credit card debt. A secured loan uses the vehicle (or boat or other property) as collateral which means the bank takes less risk.

Depending on the loan type, you may need to meet some financial qualifications, including: Have a healthy credit score Demonstrate a solid business history (For new businesses) share a detailed business plan Potentially offer up collateral. You must also show that you’re unable to get funds from any other financialinstitution.

PenFed was founded in 1935, making it a well-established financialinstitution. The companies on our list don’t require collateral from you to qualify for a loan. Pros Low-interest rates No origination fees Cons Must be a member to receive a loan Branches only in select locations. Protection of your money and information.

The proposed guidanceadvises on policies that financialinstitutions may implement to allow consumers to provide financialinstitutions with information that may not have been considered during an appraisal or if deficiencies are identified in the original appraisal. For more information, click here.

No Collateral Required – Personal term loans are typically unsecured, meaning you don’t need to put up any assets as collateral. With equipment financing, the equipment itself serves as collateral for the loan. If you default on your payments, the lender can seize the equipment to recoup their losses.

They don’t directly loan out funds, however; this is done by the financialinstitution. Offering collateral and paying higher rates are ways that may help you get funding with even a less-than-stellar credit history. Loans also adhere to specific guidelines that may not be influenced by whether you are a woman.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content