This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many secured creditors and equipment leasing companies have encountered defaulted debts, where the debtors and lessees retain possession of the collateral, including cars, boats, machinery, or other equipment. When Should Creditors use Replevin to Recover Collateral? Dania Bank , 321 So. 2d 83 (Fla. 4th DCA 1983).

When a borrower applies for a loan, most lenders require the borrower to pledge an asset as security for the repayment of the loan, i.e. collateral. In the event the borrower defaults, usually by failing to make loan payments, a secured creditor has a right to take possession of the collateral. 679.609, Fla. 2d 1020, 1024 (Fla.

Any secured creditor, large or small, may encounter a situation in which it is preferable to retain or recover the collateral in a transaction without having to sell the collateral itself. However, many will be unaware of the precise procedure and requirements for retaining the collateral itself. 679.609(1).

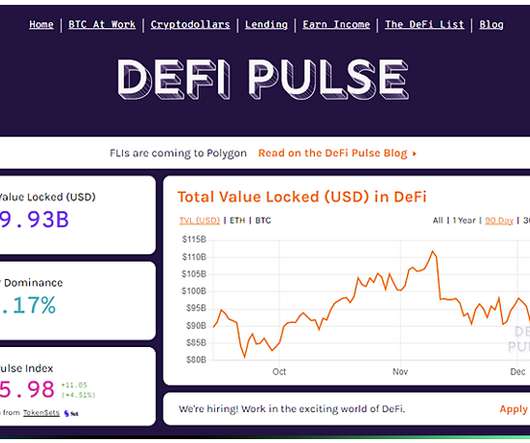

DeFi refers to Decentralized Finance; peer-to-peer financialservices on a public decentralized blockchain network, particularly Ethereum. A system that interacts buyers, sellers, borrowers, or lenders with peer-to-peer technology to access financial products or financialservices bypassing middlemen such as financial institutions.

Site visits allow lenders and CDCs to gain a first-hand impression of the borrower’s business operations, evaluate risks, and inventory the collateral. Frequent site visits help lenders and CDCs make prudent lending decisions by keeping them up-to-date with the condition of the collateral and the borrower’s business operations.

When a small business association (“SBA”) loan is converted to liquidation status, the lender must begin liquidating the collateral. The “Recoverable Value” is “the net dollar amount that a prudent lender could reasonably expect to recover by liquidating a particular piece of collateral.” See SOP 50 57. Liquidation Methods.

On November 30, crypto exchange Binance announced it has introduced a pilot program enabling banks to store trading collateral off-exchange, a move aimed at reducing counterparty risk.

How Do Property Taxes Result in Loss of Collateral? If the borrower is delinquent in paying its property taxes, a tax certificate may be sold for the past-due taxes, which could lead to a tax deed sale of the collateral. How to Get a Deficiency Judgment After a Foreclosure Sale.

When a small business association (“SBA”) loan is converted to liquidation status, the lender must begin liquidating the collateral. If the collateral is real property, the lender must liquidate all parcels of real property that has a Recoverable Value over $10,000. See SOP 50 57.

The updates expand access to collateralized intraday credit under the Policy on Payment System Risk (known as PSR policy), while providing greater clarity to institutions that streamline administrative requirements and support the launch of the FedNow℠ The final updates are substantially similar to the proposal issued in May 2021.

On July 27, the Financial Innovation and Technology for the 21st Century Act passed the House Committee on Agriculture. The bill previously passed the House Committee on FinancialServices on July 26. For more information, click here.

Before liquidating any collateral or incurring costs of litigation, Lenders and CDCs should make a good faith effort to first negotiate a “workout agreement” with the borrower. 60 calendar days), the lender/CDC must move forward with liquidating the collateral. SOP 50 57 2; SOP 50 55. See SOP 50 57 2 ; SOP 50 55.

Lenders will usually be faced with two situations: (1) the mobile home existed at the time of the mortgage, and is identified in the mortgage documents as collateral; or (2) the mobile home did not exist at the time of the mortgage, and is not identified in the mortgage documents as collateral. (1)

These changes may include, for example, the borrower’s failure to pay taxes, which if unpaid, could become senior liens against the collateral for the SBA loan. The liquidation status must include the following: Obligors; Collateral; Workout negotiations; Recoveries and expenses incurred; Liquidation and litigation proceedings; and.

Include a recommendation of whether the loan balance should be charged-off, whether any remaining collateral should be abandoned; whether the loan should be referred to the U.S. Further collection efforts are not cost effective or practical; and. One of the following: A.

Environmental Investigations are required, for example, before a lender or CDC can acquire the title to commercial real property collateral by purchasing it at a foreclosure sale or accepting a deed-in-lieu of foreclosure, or taking over the operation of a borrower’s business that uses a hazardous substance. What Are Environmental Risks?

“Recoverable Expenses” are defined as SBA approved, necessary, reasonable, and customary costs incurred to collect and enforce the terms of the Loan Documents, or to preserve or dispose of collateral. Recoverable Expenses can be added to the principal balance of the loan. See SOP 50 51 3. lien searches; Title reports; and.

If the borrower is unable to pay the full amount owed on an SBA loan after all of the collateral has been liquidated, the borrower may submit an “offer in compromise.” An offer in compromise is appropriate when the borrower’s business has closed down and all of the collateral has been liquidated. SOP 50 57 2; SOP 50 55.

No credit check to apply *Money added to Credit Builder will be held in a secured account as collateral for your Credit Builder Visa card, which means you can spend up to this amount on your card. Most secured credit cards require an initial qualifying deposit that acts as collateral and determines your credit limit. No annual fee.

The court found that the lender properly filed a foreclosure action on both mortgages in just Pinellas County because both mortgages jointly constituted the collateral for a single loan. Flagship Cmty Bank , 96 So. 3d 452 (Fla. 2d DCA 2012) , the loan was secured by two mortgages: one in Pinellas County and the other in Hillsborough County.

If lenders want to ensure a clean foreclosure proceeding and marketable title, they must join junior lien holders and persons holding encumbrances over the collateral as parties to the litigation. Indian Lake Properties, Inc., 2d 137, 138-141 (Fla. 2d DCA 1968). Conclusion.

Davidson, a member of the House FinancialServices Committee and the Congressional Blockchain Caucus, has been active in this space, having previously introduced the Token Taxonomy Act of 2021 (H.R. 1628) and co-sponsored the Blockchain Solutions for Small Business Act (H.R. dollars, U.S.

The Court analyzed Section 542’s provisions and held that “it would be illogical for us to interpret the turnover provision as imposing an automatic duty on creditors to turn over collateral to the debtor upon learning of a bankruptcy petition.” any act to. exercise control over property of the estate.” 11 U.S.C. §

Therefore, if the foreclosing lender buys the collateral at the foreclosure sale, it should obtain title insurance because it is possible that the sale could be invalidated and the collateral returned to the borrower’s ownership. 702.036(2). When Can the Foreclosure Sale Be Invalidated? 90 CWELT-2008 LLC v. Conclusion.

The new rule specifically excludes charges based solely on a borrower’s individual behavior after the extension of credit that cannot reasonably be predicted at the time of the NM-APR disclosure, such as: Actual expenditures, including reasonable attorney fees, for legal process or proceedings to collect on a loan pursuant to statutory limitation; (..)

A few considerations include, but are certainly not limited to: requiring borrowers to obtain business interruption insurance that includes broad coverage such as pandemic coverage; requiring unconditional guarantees; requiring an assignment of rents provision; or properly securing the loan with adequate collateral.

Additionally, as briefly discussed in part 5 of this series, during the foreclosure action, lenders have options to try to preserve the value of the underlying collateral and to minimize further losses. As discussed in parts 1-4 of this series, lenders have several options prior to instituting a commercial foreclosure action.

When reviewing a loan modification request, lenders and CDC’s must: Analyze the borrower’s financial documents and determine whether the borrower will be able to repay the loan if the modification request is approved; If the request impacts the collateral, analyze the recoverable value; Review the loan documents to ensure that the servicing request (..)

Asset-backed securities are initiated when a financial institution creates securities collateralized or backed by the cash flows generated from the underlying group of assets in the securitized pool. mortgage-backed securities), auto loans, and credit card balances. These asset-backed securities are then sold to investors.

The clearing and settlement process was front and center at the House FinancialServices Committee’s February 18, 2021 hearing over the GameStop (NYSE: “GME”) short-squeeze and Robinhood’s pause in GME trading. Additional Resources on the House Financial-Services Committee hearing on GameStop are here.

Furthermore, you inquired as to should a deficiency balance be realized after the sale of the collateral would Green Tree pursue Mr. & Mrs. Hagy for the amount of the deficiency. I believe this letter satisfies any and all of your concerns.

Depending on the reason, they often do not require collateral. Credit Builder Loans : Credit builder loans are offered by some financial institutions. Credit Cards Issued by a Bank, Credit Union, or other financialservices company : These are accounts backed by a major payment network, like Visa, Mastercard, or American Express.

When deciding whether to appoint a receiver, the court must consider the following facts and circumstances enumerated in the Act, together with any other relevant facts: Whether appointment of a receiver is necessary to protect the mortgaged property from waste, loss, substantial diminution in value, transfer, dissipation, or impairment; Whether the (..)

. & Loan Ass’n of Panama City, 516 So. 2d 344, 345 (Fla. 1st DCA 1987) (identifying guidelines for a court to consider when determining whether to appoint a receiver).

As a result, there's a tendency to over-compensate when lending to SMEs, due mainly to lack of viable application information, lack of industry knowledge, gaps in financial performance, or missing collateral guarantees. FICO is already helping lenders across the globe plug the trade finance gap.

1st DCA 2016) (“Appellant’s attorney, as the agent of appellant, was entitled under the statute to certify that appellant was in possession of the original note based on counsel’s review of the collateral file, which contained the original note and was provided to counsel in connection with legal proceedings to enforce the note.”).

While the bank previously accepted late payments during a “grace period,” Mercantile did not accept any late payments from the Guys after January 2008, and Mercantile eventually seized the Guys’ real property, foreclosed on other collateral, garnished their wages, and obtained a deficiency judgment against them.

The clearing and settlement process was front and center at the House FinancialServices Committee’s February 18, 2021 hearing over the GameStop (NYSE: “GME”) short-squeeze and Robinhood’s pause in GME trading. Additional Resources on the House Financial-Services Committee hearing on GameStop are here.

Creditors may now rest assured that as long as their passive retention of collateral seized prepetition is consistent with maintaining the status quo as of the petition date, they will not run afoul of the automatic stay.

The most popular posts in our Customer Development category dealt with credit card payments, open banking, trends for financialservices and small business lending — as well as FICO’s listing as a top risk management firm. Report: 2022 Trends for FinancialServices. Here are extracts from those posts. Filling the US$3.4

2547 was sponsored by House FinancialServices Committee Chairwoman Rep. Despite objections from CUNA and NAFCU, the House of Representatives passed the Comprehensive Debt Collection Improvement Act on Thursday. The bill, H.R. Maxine Waters (D-Calif.), passed the House with a 215-207 vote.

Per the notice, the lender is obligated to continue servicing PPP loans until they are: (1) paid in full; (2) forgiven in full; or (3) the SBA purchases the guaranty and provides for charge-off of the remaining balance. However, the SBA has recognized alternative procedures for unsecured PPP loans.

All these personal loans are unsecured which means you don’t have to put up collateral. That’s the whole point of the service: You fill out one application and the data goes to a variety of financialservices companies. The fees and interest you pay on your loan will go to the actual lender and not to Fiona.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content