This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When lenders take life insurance policies as collateral for loans, they need to be aware of what needs to occur to place a claim in the event their borrower dies. Therefore, it is critical for lenders to confirm that no prior assignment exists on life insurance collateral prior to taking the collateral on as security for a loan.

Conducting site visits are an important aspect of servicing SBA loans. Site visits allow lenders and CDCs to gain a first-hand impression of the borrower’s business operations, evaluate risks, and inventory the collateral. Within fifteen (15) days of the occurrence of an adverse event (i.e. SOP 50 57 2 ; SOP 50 55.

Many secured creditors and equipment leasing companies have encountered defaulted debts, where the debtors and lessees retain possession of the collateral, including cars, boats, machinery, or other equipment. Broward Bank , a creditor bank hired individuals to repossess a car from a debtor who defaulted on its secured loan with the bank.

When underwriting and servicing SBA loans, it is important for lenders and CDCs to ensure appropriate insurance coverages are in place to protect the collateral. The SBA does require some types of insurance coverages to be in place on all loans. Hazard Insurance. 13 CFR § 120.160 ; SOP 50 10 5(K). Real Estate Insurance.

When a small business association (“SBA”) loan is converted to liquidation status, the lender must begin liquidating the collateral. The “Recoverable Value” is “the net dollar amount that a prudent lender could reasonably expect to recover by liquidating a particular piece of collateral.” See SOP 50 57. Liquidation Methods.

When a borrower applies for a loan, most lenders require the borrower to pledge an asset as security for the repayment of the loan, i.e. collateral. In the event the borrower defaults, usually by failing to make loan payments, a secured creditor has a right to take possession of the collateral. 679.609, Fla.

In traditional lending and loanservicing, it is commonplace for loans to be assumed, assigned, or sold. Most lenders are likely familiar with these servicing actions, and many lenders have their own requirements and procedures for handling each of them. Assumption of SBA Loan. SOP 50 57 2 ; SOP 50 55.

When a small business association (“SBA”) loan is converted to liquidation status, the lender must begin liquidating the collateral. If the collateral is real property, the lender must liquidate all parcels of real property that has a Recoverable Value over $10,000. See SOP 50 57.

In the event a borrower is seriously delinquent on making payments under a SBA loan, or the SBA loan is classified in liquidation status, lenders and CDCs must develop a prudent and commercially reasonable strategy to maximize their recovery on the loan. 9) The signatures of the lender/CDC and all obligors on the loan.

If the borrower is unable to pay the full amount owed on an SBA loan after all of the collateral has been liquidated, the borrower may submit an “offer in compromise.” An offer in comprise allows borrowers to settle their debt on the SBA loan for less than the full amount owed. What is an Offer in Compromise?

When a SBA loan is in liquidation status, lenders and authorized CDC liquidators are required to perform “Prudent Liquidation.” When Prudent Liquidation is complete, it’s time for the lender or authorized CDC liquidator to submit a wrap-up report to the SBA and have the loan charged-off. 120.535(b). 120.535(b). SOP 50 57 2.

Lenders are responsible for servicing and liquidating all of the 7(a) loans in their portfolio. CDC’s are responsible for servicing 504 loans in their portfolio, but they will only be responsible for liquidating the loan based on its designation. Performance Standards. 120.535(a). 120.535(b). 120.535(c).

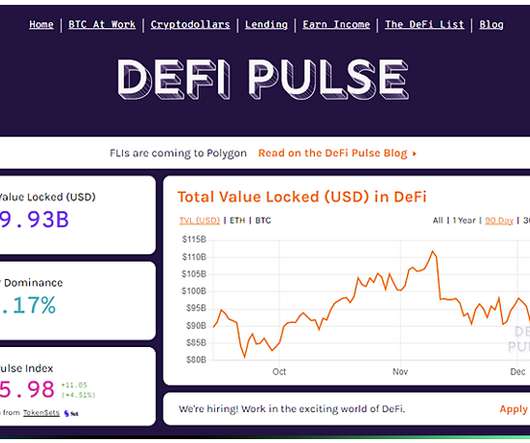

DeFi refers to Decentralized Finance; peer-to-peer financialservices on a public decentralized blockchain network, particularly Ethereum. A system that interacts buyers, sellers, borrowers, or lenders with peer-to-peer technology to access financial products or financialservices bypassing middlemen such as financial institutions.

“Recoverable Expenses” are defined as SBA approved, necessary, reasonable, and customary costs incurred to collect and enforce the terms of the Loan Documents, or to preserve or dispose of collateral. Recoverable Expenses can be added to the principal balance of the loan. See SOP 50 51 3. lien searches; Title reports; and.

If a borrower is experiencing difficulties making payments on their SBA loan, they may seek relief with the lender or CDC by requesting a loan modification or deferment. What is a Loan Modification? What is a Loan Modification? Re-amortization of loan payments. 7(a) Loan Modifications.

Whether you’re making a big purchase or just refinancing some existing debt, a personal loan could help. But comparing loan options could take days — unless you use an online marketplace like Fiona which lets you compare personal loan offers side by side within minutes. How Fiona Loans Work. Fiona Loan Fees.

How Do Property Taxes Result in Loss of Collateral? If the borrower is delinquent in paying its property taxes, a tax certificate may be sold for the past-due taxes, which could lead to a tax deed sale of the collateral. Continued reading: Defaulted Loans: Florida State Laws, Federal Laws and Federal Regulations.

On December 7, the Consumer Financial Protection Bureau (CFPB) released research, revealing that Reserve and National Guard members called to active duty are paying an extra $9 million in interest every year because they are not always receiving the benefit of their right-to-rate reductions under the Servicemembers Civil Relief Act (SCRA).

On December 13, the CFPB and the Federal Housing Finance Agency published updated loan-level data for public use through the National Survey of Mortgage Originations. d/b/a Premier Student Loan Center, a student-loan debt-relief company. For more information, click here. For more information, click here.

If a borrower defaults on a SBA loan, the lender or CDC must assess the environmental risk of contamination before conducting any liquidation action that could result in a loss, or otherwise increase the risk of loss, due to the actual or alleged presence of contamination. What Are Environmental Risks? SOP 50 57 2 ; SOP 50 55.

On July 27, the Financial Innovation and Technology for the 21st Century Act passed the House Committee on Agriculture. The bill previously passed the House Committee on FinancialServices on July 26. For more information, click here. For more information, click here.

However, lenders often wonder where they should file the foreclosure action if the loan is secured by mortgaged land situated in different counties. 2d DCA 2012) , the loan was secured by two mortgages: one in Pinellas County and the other in Hillsborough County. This is typically referred to as the “local action rule.” 3d 452 (Fla.

The first-half of this series evaluated considerations for lenders faced with borrowers who were unable to meet their mortgage and loan obligations. Opportunities to Gain Concessions in Loan Workouts with Existing Borrowers. to include an assignment of rents provision). Avoiding Lender Liability.

& Loan Ass’n, 214 So.2d If lenders want to ensure a clean foreclosure proceeding and marketable title, they must join junior lien holders and persons holding encumbrances over the collateral as parties to the litigation. Continued reading: Defaulted Loans: Florida State Laws, Federal Laws and Federal Regulations.

On July 15, 2021, the SBA issued its procedural notice regarding lender requests to the SBA for guaranty recovery of PPP loans. The PPP loan program has offered billions of dollars in assistance to small businesses across the country. However, many PPP borrowers have since begun defaulting on their loans.

Lenders will usually be faced with two situations: (1) the mobile home existed at the time of the mortgage, and is identified in the mortgage documents as collateral; or (2) the mobile home did not exist at the time of the mortgage, and is not identified in the mortgage documents as collateral. (1)

Basically, credit scoring models want to see that you can manage different types of financing, most notably revolving accounts, such as a credit card, and installment accounts, such as a mortgage or auto loan. You are not required to pay the loan in full each month. Depending on the reason, they often do not require collateral.

We’ve collected a list of business credit and loan resources for LGBTQIA+ business owners to help get you up and running. Qualifications for Loans/Credit for LGBTQIA+-Owned Businesses Each business loan or credit option we’ll talk about has its own list of qualifications. There are a few avenues worth exploring.

On March 29, the New Mexico Financial Institutions Division of the Regulation and Licensing Department’s (NM FID) new rule on the New Mexico-Annual Percentage Rate (NM-APR) becomes effective. This new rule addresses the types of charges excluded from the 36% NM-APR cap. The rule is available at N.M.

Therefore, if the foreclosing lender buys the collateral at the foreclosure sale, it should obtain title insurance because it is possible that the sale could be invalidated and the collateral returned to the borrower’s ownership. 702.036(2). When Can the Foreclosure Sale Be Invalidated? 90 CWELT-2008 LLC v. Conclusion.

However, upon notification of the death of a borrower, lenders must “promptly identify and facilitate communication with the successor in interest of the deceased borrower with respect to the property secured by the deceased borrower’s mortgage loan.” Although not required, the confirmed successor in interest may assume the loan upon consent.

Joy Denby-Peterson purchased a 2008 Corvette in July 2016, and several months later the vehicle was repossessed when Denby Peterson failed to make all of the required loan payments. Circuits in holding that a secured creditor does not have an affirmative obligation to return a debtor’s collateral immediately upon notice of the bankruptcy.

Additionally, as briefly discussed in part 5 of this series, during the foreclosure action, lenders have options to try to preserve the value of the underlying collateral and to minimize further losses. & Loan Ass’n, 516 So. One of those options is the appointment of a receiver. Carolina Portland Cement Co. Baumgartner, 128 So.

These assets can include loans, leases, and receivables—from aircraft leases to solar projects, but most frequently are commercial or residential mortgages (e.g., mortgage-backed securities), auto loans, and credit card balances. Cash flows are derived from the interest and the principal payments made by the borrowers on the loans.

Each business received a loan from Mercantile Bank Mortgage Company (“Mercantile”) through one loan officer, Pat Julien, in 2000 and 2006, respectively. Each loan was subsequently refinanced at least once through Julien. When Julien left Mercantile in 2006, the Guy’s accounts were transferred to a different loan officer.

& Loan Ass’n of Panama City, 516 So. 2d 344, 345 (Fla. 1st DCA 1987) (identifying guidelines for a court to consider when determining whether to appoint a receiver).

Zeynep Salman pointed out that in financialservices, it has brought about new appreciation for technology as well. The primary lesson from financial companies’ response to COVID-19 market trends is that financial challenges cannot be tackled in isolation. FICO Loan Origination Solution Awarded Best-In-Class.

1st DCA 2016) (“Appellant’s attorney, as the agent of appellant, was entitled under the statute to certify that appellant was in possession of the original note based on counsel’s review of the collateral file, which contained the original note and was provided to counsel in connection with legal proceedings to enforce the note.”).

2547 was sponsored by House FinancialServices Committee Chairwoman Rep. In the letter, Nussle stated, “Lenders rely on complete and accurate credit reports when underwriting loans. Prohibit certain abusive collection practices directed at service members, including threats to reduce rank or revoke security clearance.

The most popular posts in our Customer Development category dealt with credit card payments, open banking, trends for financialservices and small business lending — as well as FICO’s listing as a top risk management firm. Report: 2022 Trends for FinancialServices. Here are extracts from those posts. Filling the US$3.4

Aurora LoanServices, LLC, 163 So. The original assignor of a mortgage that has been collaterally assigned cannot bring a foreclosure action without the knowledge and consent of the assignee. 3d 639, 642 (2015). A non-holder in possession of the original note who has the rights of a holder. Servedio v. US Bank Nat.

Also, on an auto loan, there could be more than one missed payment, followed by a repossession, followed by a sale of the collateral and establishment of a deficiency balance. For example, on a credit card account, there could be several defaults, followed by charge-off, followed by additional payments.

On June 7, the CFPB released a blog discussing the fact that the pause on federal student loan interest, payments, and collections is now scheduled to end 60 days after June 30, which means borrowers will have to start making payments soon. For more information, click here. For more information, click here. For more information, click here.

Small Business Administration, in consultation with the Treasury Department, released an updated loan forgiveness application for Paycheck Protection Program (PPP) loans of $50,000 or less. Small Business Administration (SBA) released guidance on required procedures for changes of ownership in an entity that obtained a PPP loan.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content