This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When filing for bankruptcy, you can discharge certain types of personalloans, meaning that you’re no longer legally responsible for paying off the debt. If you’re considering filing for bankruptcy, you need to know what personalloans you can discharge and which filing method best suits your financial situation.

Everything is online these days—including personalloans. Online lenders make it easy to compare rates and terms and find the right online personalloan for your situation. Personalloans were the fastest-growing category of consumer debt in 2019 , according to a survey from J.D.

Personalloans accounted for $148 billion in consumer debt in the fourth quarter of 2020, a decline from the same period in 2019, according to credit bureau TransUnion. Personalloans are usually unsecured, meaning they don’t require collateral like a house or a car, and you can use them for almost anything.

A personalloan is money borrowed from a lender that can be used for almost any purpose, from debt consolidation to home improvement projects. Most people don’t have $5,000+ sitting in their bank accounts—that’s where personalloans come in. What Is a PersonalLoan? Why Would I Need a PersonalLoan?

Personalloans provide fast, unsecured funds that can pay for anything from home repairs to medical emergencies. Instead of requiring collateral like a house or car, many lenders prefer applicants with strong credit and high incomes. But what if you don’t meet a lender’s requirements?

Each year, tens of millions of Americans facing similar situations turn to personalloans to help ease the financial burden. With low interest for borrowers with strong credit scores, fixed rates, and a variety of lending sources to choose from, it’s easy to see why personalloans are so enticing. How PersonalLoans Work.

With the help of our research provider, Pureprofile, Finder surveyed 1,718 American adults in January 2021 to see how personalloans are being used in the US. of Americans, said they have taken out a personalloan in their lifetime. And personalloans are a popular way to fund the first few months of business.

Borrowing money costs more when you have bad credit — and your choices for a loan will be limited — which is why we have helped you narrow down your list by finding the top 6 best personalloans for bad credit. Use this time to fix your credit before applying for loans. 6 Best PersonalLoans for Bad Credit.

Whether you’re making a big purchase or just refinancing some existing debt, a personalloan could help. But comparing loan options could take days — unless you use an online marketplace like Fiona which lets you compare personalloan offers side by side within minutes. How Fiona Loans Work.

Whether you are facing unexpected costs or you simply need extra financial support, personalloans are a viable option that many people rely on. adults have an unsecured personalloan as of the third quarter of 2024. So, you’re not alone in wondering how to apply for a personalloan.

The best personalloans charge low fees and low fixed interest rates, have flexible loan amounts and terms, and have no prepayment penalties. A personalloan could let you access cash for any purpose. Since personalloans are unsecured, you’ll need an excellent credit score to get the best deal.

Paying off a credit card with a personalloan can offer the advantage of potentially lower interest rates, saving money on interest charges over time. However, the personalloan could come with origination fees or other charges that should be carefully considered. What Is a PersonalLoan?

When filing for bankruptcy, you can discharge certain types of personalloans, meaning that you’re no longer legally responsible for paying off the debt. If you’re considering filing for bankruptcy, you need to know what personalloans you can discharge and which filing method suits your financial situation.

A personalloan enables you to borrow a lump sum of money and repay it in fixed installments. While personalloans can be a useful tool, there are important factors to consider before taking one out. According to recent statistics , millions of Americans have personalloan debt, with the average loan amount being $16,931.

How to obtain a personalloan: Get a copy of your credit reports (Equifax, Experian, and TransUnion). You will need pay stubs, bank statements, and tax returns to prove this to your potential lender. Prequalify through several lenders. Compare the loan offers by examining such things as the APRs, fees, and loan terms.

If you need money now, an online personalloan can be a fast and easy way to secure funds. Whether they’re for debt consolidation, a home improvement project, or other expenses, these loans often come with low-interest rates and flexible repayment options. Ad If you're struggling to make ends meet, a PersonalLoan can help.

A personal guarantee loan is a signed agreement stating that you’re liable for a debt. For example, you may sign a personal guarantee to secure a loan for your business, and if you fail to make payments, the lender can go after both the business and your personal funds because you’re liable through the written agreement.

It works by getting one new loan and using that to pay off multiple existing creditors. You pay off multiple types of loans and credit card balances with your new consolidation loan, and you’re left with a single monthly payment to the new lender. The difference is that unsecured debts are not backed by collateral.

These loans often have low interest rates and are accessible to those with poor or nonexistent credit. That’s because you provide all of the collateral for the loan in cash, so it’s not a risk for the lender. You build credit as you pay down the loan, and you can access your balance once the loan is paid off.

A signature loan is a fixed-rate, unsecured personalloan offered by an online lender, bank or credit union. It’s called a signature loan because it’s secured by your signature instead of collateral, like a car or an investment account. The best way to. Jackie Veling writes for NerdWallet.

What Are Vacation Loan Alternatives? What Is a Vacation Loan? A vacation loan is a personalloan borrowers use to pay for transportation, hotels, and other vacation-related expenses. Typically vacation loans require no collateral and should get paid in fixed, once-a-month payments.

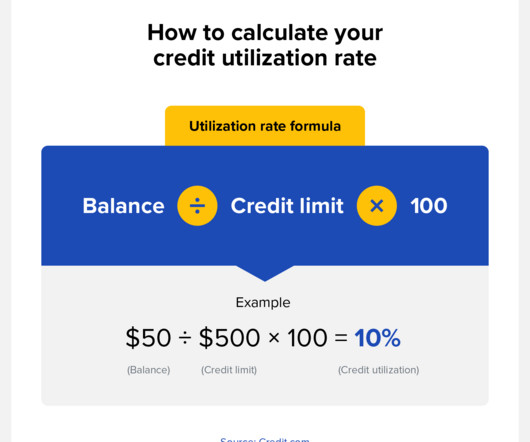

Use the same formula that lenders rely on when evaluating a loan application. The result is a percentage that determines your creditworthiness – in short, if lenders believe you’ll be able to repay the loan. Keep in mind that your ratio typically excludes mortgage and student loans.

One reason that lenders look at credit mix is to make sure that you can be responsible with multiple types of credit. Showing that you can handle different types of credit—and multiple credit accounts at once—indicates financial reliability to potential lenders. You are not required to pay the loan in full each month.

You don’t want to spend too much and go over your utilization rate, but if you don’t use it regularly enough, the lender may close your account. This makes it very low-risk for the lender, as your payments are also adding your collateral to the savings account. The solution is to use your card to make regular, small purchases.

Its scalability and preconfigured settings enable lenders to refine their collection strategies and enhance operational efficiency, establishing the QCR Accelerator as a vital tool for meeting a wide array of needs while ensuring fast ROI and lower implementation costs.

While it is possible to get a loan with no credit through some lenders, you may face high interest rates and unfavorable terms. Luckily, there are alternative ways to get a loan with no credit history. Table of Contents: What Is a No-Credit-Check Loan? Continue reading to discover how to get a loan with no credit score.

The lender protects the borrower against foreclosure. Unsecured debt is debt without collateral. Collateral guarantees debt repayment. A mortgage or car loan secures the lender’s interest in your house. personalloans, personalloans, delinquent income tax obligations, .

Credit cards can take several days, loans can range from days to weeks, and mortgages can take weeks to a month. Lenders consider multiple factors when you apply for loans and credit cards , including your credit score and current finances. How Do I Apply for a Loan? What Are the 5 C’s of Credit Approval?

Secured debts are a type of debt backed by an asset that is used as collateral. For example, when you take out a home loan, you will be required to sign a mortgage which grants the lender a lien, or security interest against your home should you fall behind on payments. What is Secured Debt? Examples of Unsecured Debts.

In broad terms, if a debt is secured, it means it is backed up by collateral property. If a debt is unsecured, no collateral is put up as a guarantee to pay. However, it is important to note that before bankruptcy is declared, lenders can still come after you to get you to pay off the unsecured debt.

There are many types of loans for a variety of purposes, but it’s always critical to consider certain key criteria in detail before making any final decisions. Even a few small differences between lenders and the loans that they’re offering can have an impact on your finances. Maintain a Good Credit Rating.

Most credit builder loan repayment terms range between 6 and 24 months. How Do Credit Builder Loans Work? Credit builder loans work differently than regular loans. You gain access to your money after you make your final loan payment. How Are Credit Builder Loans Managed?

Briefly, unsecured debts are not backed by any collateral and include things like credit card balances and unpaid medical bills. Creditors cannot reclaim any of your property if you default on a loan. However, secured debt means the borrower has put up collateral (e.g. When Should I Consider Declaring Bankruptcy?

Entering a reaffirmation agreement is a way that debtors in a Chapter 7 bankruptcy keep collateral attached to secured debt like houses or cars. All of the original terms of the loan are back in force, including the creditor’s right to repossess the collateral if you get behind on payments in the future.

Obtaining PersonalLoans with a Cosigner Having a co-signer on a personalloan or credit card means that you associate another individual with your debt. It’s often necessary for risky or low-credit borrowers to have a co-signer in order to secure a loan or another form of debt. Considering Filing for Bankruptcy?

Building a successful startup comes with its fair share of challenges, chief amongst them being the search for loans and funding. While chasing that dream investment, startups often face a tough time trying to secure loans, primarily due to minimal or no revenue. This can make it easier to justify the loan to yourself and the lender.

These include transferring all your debt onto just one credit card as well as taking out a secured or unsecured personalloan—perhaps with the help of a professional debt consolidation company. You can combine credit card debt, car finance, personalloans, student loans, medical bills, payday loans, and other types of unsecured debt.

If you qualify for Chapter 7 bankruptcy, our attorneys can guide you through the process of eliminating unsecured debts, such as credit card balances, medical expenses, and personalloans, within a matter of months. With secured debts, your creditors have the right to seize the collateral property if you default on payments.

Unsecured debt is a type of debt that is not backed by collateral. Credit cards, medical bills, and personalloans make up most unsecured debt that bankruptcy can eliminate. These debts have no collateral, so creditors cannot take your property without going to court first. This means there is no property tied to it.

Whereas rates on credit cards can be 13-25%, average rates on personalloans are 14-18%,” says Toms. Other factors to consider include: Fees: Some lenders will charge what is called an Origination Fee, usually as a percentage of the amount owed, often around 1% to 5%. Best Debt Consolidation Loans. Lending Tree.

Whereas rates on credit cards can be 13-25%, average rates on personalloans are 14-18%,” says Toms. Other factors to consider include: Fees: Some lenders will charge what is called an Origination Fee, usually as a percentage of the amount owed, often around 1% to 5%. Best Debt Consolidation Loans. Lending Tree.

Credit Card Consolidation Loans A credit consolidation loan is a type of unsecured personalloan that comes with a set repayment period and fixed monthly payments. For a credit card consolidation loan to make sense, the interest rate needs to be lower than the interest rate for your credit cards.

The reason your credit score, or your FICO score as it’s known in the financial industry, is so important is that mortgage lenders will use it to determine how much of a risk it is to lend to you, based on your history of paying your bills on time and other factors. ” Mortgage Rates for Spouses.

This includes debts such as credit card balances, medical bills, personalloans, utility bills, back rent, mortgages, and car payments. However, if you used your home or car as a secured debt with a lender, you may need to return the property to the lender if you don’t pay as agreed.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content