This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The credit and collection sector could be next. Why it matters: As collectionagencies, debt buyers, fintechs, banks, and creditunions seek to improve consumer engagement, LLMs offer a potential solution for more natural and effective communication.

The Bureaus new emphasis on tangible consumer harm, while deprioritizing areas such as medical debt and digital payments, signals a shift in enforcement priorities that may influence the regulatory landscape for many companies in the credit and collection industry.

Why it matters: For professionals in debt collectionagencies, debt buying companies, fintechs, banks, creditunions, and consumer finance firms, these findings underscore a growing vulnerability among older borrowers.

Debt collectionagencies in PR include Kinum , TSI , CICA, ILCA and Professional recoveries. Spanish and English-speaking debt collectors are required for Puerto Rico debt collection. Need a CollectionAgency in PR? Puerto Rico is one of the states that regulate the collection of fees and interest.

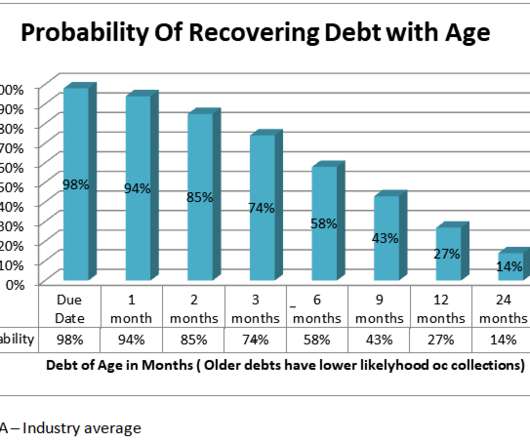

An average collectionagency will recover about 20% of the total debt assigned. Here are the most important factors which decide how much a collectionagency will collect for you: 1. Some clients may get a 100% recovery rate, for others it could very well be 0%.

As per FTC, starting June 9, 2023 all collectionagencies will be treated as financial institutions. This means all collectionagencies must secure consumer data nearly the same way as banks. Failure to comply with GLBA can have severe consequences for the collectionagency, especially the owners and/or the CEO.

Mountain America Federal CreditUnion , the plaintiff became delinquent on a credit card account with her creditunion. The creditunion then assigned the debt to a third-party collectionagency. In Hansen v. A copy of the order is available here.

What’s happening: SMS is quickly becoming a preferred communication method for banks, creditunions, collectionagencies, and fintech companies. According to the 2024 Consumer Texting Behavior Report, 84% of consumers check their texts within 15 minutes of receiving them, and 77% respond in that timeframe.

Based on clients we came across last year (2021), here is the average recovery rate we have seen, along with our collectionagency partner(s). No collectionagency publically publishes the results they achieve by industry. CreditUnions. This is purely our own experience. Recovery Rate. Transportation.

This behavior, observed in the retail world, is a crucial lesson for collectionagencies, debt buyers, fintechs, banks, and creditunions. If you don’t offer payment options that consumers want to use, 70% of them are going so shop somewhere else, according to a published report.

Credit bureaus will soon stop reporting medical debts lower than $500, remove medical line items that have been fully paid, and collectionagencies now have to wait for 1 year before medical debts can be reported. These include government rules, credit scoring models and even credit bureaus.

A District Court judge in Utah has denied a defendant’s motion to dismiss in a Fair Credit Reporting Act case, ruling that it did not conduct a reasonable investigation after the plaintiff disputed the debt because both the defendant — the original creditor — and a collectionagency were reporting the debt to the credit […] (..)

Five federal financial institution regulatory agencies in conjunction with the state bank and state creditunion regulators (collectively, agencies) are jointly issuing this statement to remind supervised institutions that U.S. dollar (USD) LIBOR panels will end on June 30, 2023.

The DCLA would prohibit a person from engaging in the business of collecting on a consumer debt in this state without a license and comply with reporting, examination, and other oversight by the California Department of Business Oversight (DBO). The DCLA would also require the DBO to respond to consumer complaints and enforce violations.

An Illinois federal district court recently denied a creditor-defendant’s motion for summary judgment in a Fair Credit Reporting Act (FCRA) case brought by a consumer who questioned why his debt was being reported twice — as both a tradeline with the original creditor and as a tradeline with a third-party collectionagency.

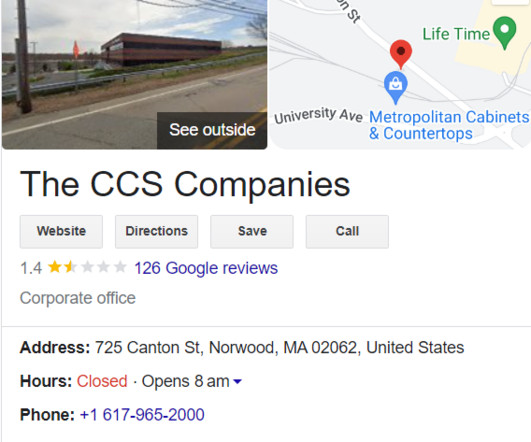

Dealing with debt collectionagencies can be unpleasant, and CCS Offices are no different. It’s common for debt collectors to purchase and sell debts, resulting in the possibility of multiple collection accounts from the same debt appearing on your credit report. Who are CCS Offices?

Once you’ve accomplished these tasks, you may still be wondering how to pay collections to a debt collectionagency. Find out how to pay collections below. The Fair Debt Collection Practices Act (FDCPA) provides protection for consumers. How Should You Pay a CollectionAgency? Verify the Debt.

On December 16, the National CreditUnion Administration — the federal regulator that oversees creditunions — announced that creditunions may partner with third-party digital asset service providers to give members access to cryptocurrencies and other digital assets. For more information, click here.

Some payday lenders are quick to report default or sell loans to a collectionsagency. Instead, look at other options, such as: Reducing your expenses Delaying paying some bills Getting a loan from a bank or creditunion Using a credit card Borrowing from family and friends Borrowing from employer.

SIMM is a full service nationally licensed ARM company providing collection solutions to the student lending, consumer lending, credit/retail card, healthcare, auto finance, creditunion and debt buying industries. Find The Best CollectionAgency For Your Business. * *. state of the art call center.

The bill also prohibits providers from: Compelling a consumer to repay by use of unsolicited telephone calls, filing a suit against the consumer, using a third-party collectionagency, or selling outstanding amounts to a third-party collector.

Notably, the law does not apply to FDIC-insured banks or savings and loan associations, creditunions, or any person authorized to make loans or extensions of credit. Using credit reports or credit scores to determine a consumer’s eligibility for EWA services. Accepting payment from a consumer via credit card.

Nearly any commercial enterprise can benefit from professional collection assistance. What does a collection attorney do? Some collectionagencies simply send threatening letters, but may not provide much follow through.

Hire a collectionagency and your invoices will always go out on time. Collectionagencies operate on a code of ethics. But a collectionagency minimizes that possibility. But a collectionagency minimizes that possibility. In 2016 alone, debt collectionagencies recovered $78.5

Experian reports that the lowest FICO credit score is 300, but no one really stays at such a low score once some financial history has been established. Other items on your credit report require more attention and follow-up. And that’s encouraging to think about. What about the ‘invisibles’?

Credit Repair. CollectionAgencies. From collections to creditunions, we treat our clients as our business partners – your success is our success. Their restricted industries are typically controversial and prone to the risky activities previously mentioned. Examples include: Cigarettes.

The bill also prohibits providers from: Compelling a consumer to repay by filing a suit against the consumer, using a third-party collectionagency, or selling outstanding amounts to a third-party collector.

You can discharge an unsecured loan whether it’s current, delinquent, or in default, even if the original lender sold it to a collectionagency or debt buyer. No-credit-check lending, such as payday and title loans, often comes with unreasonable fees and annual percentage rates (APR). Unsecured loans don’t have collateral.

They are a particularly tenacious debt collectionagency that will come after you until you pay up. Not only that, but they will wreak havoc on your credit score as well. Before contacting you for payment, a debt collector has to contact the major credit reporting agencies and open a collections account.

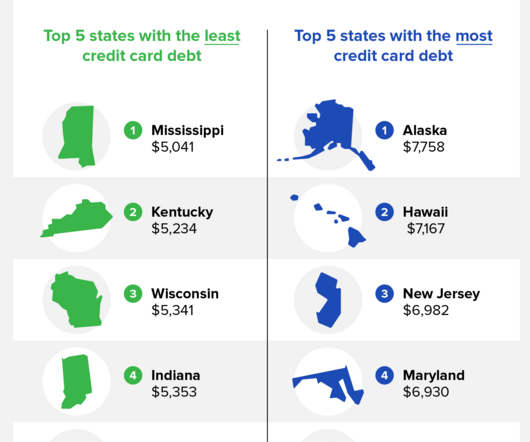

Despite the national average of Americans having over $9,000 in credit card debt per household, only 14% say they’re “very worried” about their debt. 67% of respondents said they have less than $2,000 in debt, which may indicate that only a concentrated number of people have high amounts of credit card debt.

SIMM is a full service nationally licensed ARM and BPO company providing collection solutions and customer engagement to the student lending, consumer lending, credit/retail card, healthcare, auto finance, creditunion and debt buying industries. Its headquarters is located in Delaware in a 32,000 sq.

ConServe is a debt collectionagency that may contact you regarding unpaid debts. They are notoriously difficult to work with, and their presence on your credit report can mean trouble for your score in the long run. I recommend Sky Blue to anyone looking for a high-quality credit repair company. Ask Sky Blue for Help.

Despite the national average of Americans having $9,000 in credit card debt per household, only 14 percent say they’re “very worried” about their debt. 67 percent of respondents said they have less than $2,000 in debt, which may indicate the national average means that a concentrated number of people have high amounts of credit card debt.

Payment history mostly pertains to debts from mortgages, loans, and credit cards. However, after several missed payments on services like your phone, internet, and medical bills, those accounts can be turned over to a debt collectionagency and placed on your credit report. Collections.

The advisory provides a list of steps a consumer can take to ensure that they have the full benefit of those funds by protecting them from bank and creditunion setoffs if the consumer’s account is overdrawn. For more information, click here. The bill has been engrossed to the house for its consideration.

CICA CollectionAgency, a First Circuit case in which the CFPB has filed an amicus brief. In that case, after an individual filed for bankruptcy, a debt collector sent the consumer a collection letter that said the consumer could be sued if they did not pay the debt — a process the CFPB believes is against the law.

Their assistance can help you clean up your credit report and begin to rebuild your credit score. Originally founded in 2008, Rausch Sturm is a medium-sized debt collectionagency out of Brookfield, WI. Ask Sky Blue for Help. What is Rausch Sturm?

Common reasons for bank account garnishment in Texas include: Private creditors: These are banks, creditunions, credit card companies, peer-to-peer lenders, hard money loan providers, and other financial institutions. This debt can include anything from credit cards to past due balances on office space.

Accredited CollectionAgency Inc. , No. As such, a number of courts have declined to award damages for emotional distress where the plaintiff’s testimony was not supported by medical bills. See, e.g., Lane v. 6:13-CV-530-ORL-18, 2014 WL 1685677, at *8 (M.D.

On June 8, the board of governors for the Federal Reserve (the Fed), Consumer Financial Protection Bureau (CFPB), Federal Deposit Insurance Corporation (FDIC), National CreditUnion Administration (NCUA), and the OCC requested public comment on proposed guidance addressing reconsiderations of value (ROV) for residential real estate transactions.

The bill subsumes debt buyers into the definition of “collectionagency,” subjecting debt buyers to regulation by the state’s CollectionAgency Board. Accordingly, debt buyers will be required to obtain licenses from the board to conduct collections or act as a debt collector.

The bill subsumes debt buyers into the definition of “collectionagency,” subjecting debt buyers to regulation by the state’s CollectionAgency Board. Accordingly, debt buyers will be required to obtain licenses from the board to conduct collections or act as a debt collector.

Why it matters: While the CFPB claims this will increase credit scores and expand access to low-cost mortgages, the plaintiffs in both lawsuits argue the rule oversteps legal boundaries and creates significant disruptions for lenders, creditunions, and healthcare providers.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content