This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

So, what happens when you don’t pay a bill or repay a debt? The company, creditor or collectionagency has legal ways to pursue payment. The judgment creditor can then use that court judgment to try to collect money from you. Common methods include wage garnishment , property attachments and property liens.

However, if a judgment is already filed, it can diminish your ability to move until you resolve the debt. A judgment can allow a creditor to file a lien against your property or garnish your accounts, for example. Even if you do manage to leave the country, you might want to return one day. Why Won’t This Strategy Work?

This unpaid debt can lead to a serious problem for businesses: garnishment. Bank account garnishment can create serious cash flow blocks for companies of all sizes, and those cash flow problems can compound into other issues, like payroll concerns and late payments on other accounts.

Agents can simply imply threats, and that’s often enough to prompt payment, such as threatening to call your employer and set up wage garnishment arrangements. But, under federal law, a legitimate debt collector must first successfully sue you in civil court to be able to garnish your wages.

FDCPA ( Fair DebtCollection Practices Act). The Fair DebtCollection Practices Act (FDCPA) is a federal law that restricts the behavior of collectionagencies when they are attempting to collect money from individuals. The law does not apply to collecting from businesses. Garnishment.

If you’re dealing with debt and considering filing for bankruptcy, it’s a good idea to get professional legal advice on how to handle the proceedings. Credit counseling and debtmanagementagencies may be able to assist you as you work, but with so many untrustworthy schemes out there, how do you know what the right step should be?

As the fees pile up and the interest compounds, you might face a debt collector or even a civil lawsuit. The resulting court judgment remains public for seven years, and a successful lawsuit can lead to garnishment of your wages or even seizure of your assets. How Can Protect Yourself If You Need a Payday Loan?

DebtManagement Programs. Debt relief programs or debtmanagement plans are very common these days. Typically, these programs enable you to pay off all of your credit card debt in full, but through a single reduced rate payment. You should also be wary of debt relief scams. Debt Settlement.

Continued missed payments will subject you to a world of financial hurt: Your card could be frozen, you could be hassled by a collectionagency, and you might get sued. The more time you delay making a payment, the more likely you are to get calls from the credit card issuer’s internal collectionsagency.

Two of the most common are coming up with enough money to pay off the debt and negotiating a payment plan or settlement you can afford. Once you’ve accomplished these tasks, you may still be wondering how to pay collections to a debtcollectionagency. Find out how to pay collections below.

Post collection policies on your website and make them available to patients through their online accounts. Inform the billing department of all collection policies, and train billing staff as necessary. Work with Reliable Third-Party CollectionAgencies. Contract with a Trustworthy DebtCollection Provider.

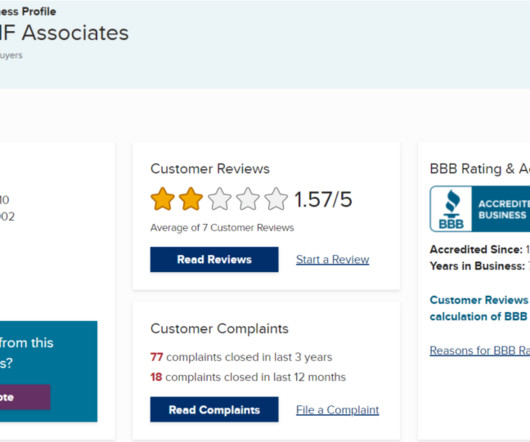

A default judgment enables DNF Associates, LLC to seize your bank account, garnish your wages, and take other damaging legal actions against you. To improve your chances of success and prevent further legal action against you, it is advisable to engage the services of a debt defense lawyer.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content