This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Collectionagency letters can impact debtors, depending on factors such as the debtor’s financial situation, emotional state, and knowledge of their rights and responsibilities. Here are some potential impacts: Stress and Anxiety : Receiving a letter from a collectionagency can cause significant stress and anxiety for debtors.

Once this happens, you may face serious ramifications, including wage garnishment and the offset of your federal tax refund and Social Security benefits. If the lender sells the loan to a collectionagency after you default, you’ll also face additional fees and higher interest rates. Contact Indianapolis Student Loan Lawyers.

When collecting a debt from you, collectionagencies must adhere to federal and state rules. Fortunately, the federal Fair Debt Collection Practices Act (FDCPA) protects all states. The Fair Debt Collection Practices Act (FDCPA) does not apply to original creditors or cover company obligations.

The company, creditor or collectionagency has legal ways to pursue payment. The judgment creditor can then use that court judgment to try to collect money from you. Common methods include wage garnishment , property attachments and property liens. This is known as wage garnishment. Nonwage garnishment.

This local company turned to us after seeing minimal progress with a collectionsagency and were able to receive their monies without alienating their client. When we win your case, collecting the judgment may be made easier if monies were previously frozen by way of an ex parte bank or trustee attachment. and Crest Tractor.

Have you ever been incessantly contacted by a debt collectionagency trying to get money from you? It can be difficult to understand just what exactly these agencies are legally allowed to do, and what crosses the line. The majority of debt collectors work for reputable collection companies. That’s why we’re here to help.

The debt collection process can be tricky. Collectionagencies must follow regulations strictlyor youll find your business in jeopardy. Compliance can be even harder when scammers actively try to disrupt your debt collection practices through call baiting. Are you going to garnish my wages? When is my payment due?

Bankruptcy can also stop or delay a home or mortgage foreclosure, stop collection actions, stop garnishments and lawsuits. Consult with a bankruptcy lawyer about what your debt negotiation options are. Debt collectionagencies can be thoroughly unpleasant. What Do the Various Kinds of Bankruptcy Entail?

At the same time, payday lenders will start calling you and sending letters from their lawyers. The resulting court judgment remains public for seven years, and a successful lawsuit can lead to garnishment of your wages or even seizure of your assets. They may even call your personal references.

Additionally, you can discharge a loan regardless of whether the original lender has the loan or whether the lender sold it to a collectionagency or debt buyer. Even if a creditor has initiated a wage garnishment you can still discharge the unsecured loan in Chapter 7 bankruptcy. Contact Indiana Bankruptcy Attorneys.

Contact a lawyer for your unique situation if you have questions. Each state has a law referred to as a statute of limitations that spells out the time period during which a creditor or collector may sue borrowers to collect debts. Can a CollectionAgency Report an Old Debt as New? Always respond to legal summons.

For out-of-state creditors, the commercial litigation collectionslawyers at Law Offices of Alan M. Once filed, you must wait 30 days until the execution is issued, and our attorneys can begin using our effective methods of collection to attempt to collect the monies you are owed.

It is enforced by the Federal Trade Commission , a federal agency that protects consumers and maintains fair competition in the marketplace, including debt collection attempts. The law specifically limits how and when collectionsagencies can contact you, and it allows you to dispute debts. What Does the FDCPA Apply to?

If you are drowning in debt but aren’t sure which option is right for you, it can help to consult with an experienced lawyer. If a creditor does not want to participate, they can still pursue you in all the ways allowed by law including lawsuits and wage garnishments. Debt Settlement.

And, after ordering you to repay the money, a judge could approve wage garnishment which means the court would take part of your paycheck and give it to the creditor before you even see the money! You’d may have to hire a lawyer, but if the debt is big enough this might pay off. This is usually an easy dismissal.

Relying on handshakes and oral promises may feel more natural but in commercial debt collection, it is extremely helpful to have good paperwork. A solid paper trail helps your chances of having our collectionslawyers persuade your debtor to pay, It also improves your chance at winning at trial.

Correspondence from a collectionagency often end up in the trash unread, but a letter from a debt collection attorney is more likely to prompt action by the debtor. The average consumer is far more likely to be responsive when contacted by a lawyer than by a collectionagency.

The Pew researchers found that while most businesses filing debt collection claims were represented by attorneys, only about 10% of consumers being sued had lawyers. Some think the creditor’s lawyer will steamroll over them and they do not have any real way to fight back. Fighting Back When Debt Collectors Sue.

Throughout the debt recovery process, you may be tempted to take the path of least resistance and try to either put the situation behind you or turn to a collectionsagency. The relentless collectionlawyers at the Law Offices of Alan M. These types of situations are where post-judgment collection comes into play.

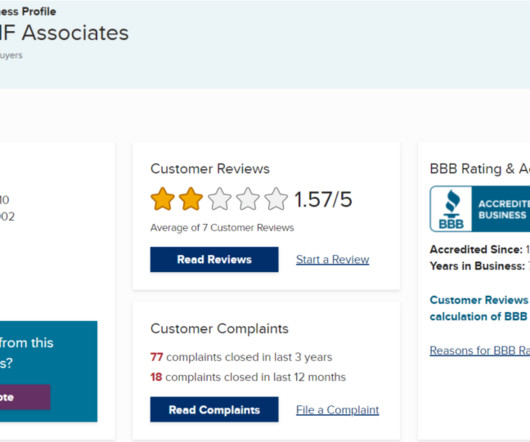

A default judgment enables DNF Associates, LLC to seize your bank account, garnish your wages, and take other damaging legal actions against you. To improve your chances of success and prevent further legal action against you, it is advisable to engage the services of a debt defense lawyer. What is DNF Associates, LLC?

Collectionagencies are passive organizations that make the same effort you were making before you brought them on board. At the end of the day, a collectionagency will collect only low-hanging fruit and tell you that there is nothing more that they can do to help you.

In addition to traditional communication methods, many debt collectionagencies also use other tactics, such as sending frequent emails and letters in an effort to motivate delinquent accounts into making payments or entering into payment arrangements.

When you file a Chapter 7 petition, you’ll receive an automatic stay protecting you from lawsuits and other collection efforts. This bankruptcy protection will prohibit a collectionagency or another creditor from recovering debt or taking action against you.

The Florida Consumer Collection Practices Act (FCCPA) and the Fair Debt Collection Practices Act (FDCPA) are two pro-consumer statutes. Accredited CollectionAgency Inc. , No. Businesses should be aware of each statute and how to defend against such claims. See, e.g., Lane v.

Debtors who have filed for bankruptcy and received their Discharge often continue to receive collection letters and phone calls from their creditors. Some creditors even go so far as to sue on these discharged debts or garnish wages and bank accounts. Some common examples include: The sale of a discharged debt to a collectionagency.

Federal loans charge high-interest rates, and if you default, the government could sell your loan to a collectionagency. When you default on a federal student loan, the government can garnish up to 15% of your wages or social security income without a court order. They can even intercept your federal tax refund.

The role of the Attorney General (AG), head of the Department of Law, is “both the People’s Lawyer and the state’s chief legal officer…serves as the guardian of the legal rights of the people of New York, its organizations, and its natural resources.”

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content