This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When filing for bankruptcy, you can discharge certain types of personalloans, meaning that you’re no longer legally responsible for paying off the debt. If you’re considering filing for bankruptcy, you need to know what personalloans you can discharge and which filing method best suits your financial situation.

“Our digital and omnichannel solutions provide forward-thinking lending companies like SoFi the flexibility and control they need to drive the right experience, reduce costs, and improve collections and the overall member experience.” The post Katabat Platform to Support SoFi Ominchannel PersonalLoanCollections appeared first on Katabat.

When filing for bankruptcy, you can discharge certain types of personalloans, meaning that you’re no longer legally responsible for paying off the debt. If you’re considering filing for bankruptcy, you need to know what personalloans you can discharge and which filing method suits your financial situation.

Creditors give loans to millions of citizens, and thus credit companies are too busy to follow up on the debtors. For this reason, creditors are hiring debt collectionagencies to collect debts that are 60 days past the agreed period. Therefore, the agencies act as middlemen collecting any delinquent loans.

When a lender doesn’t receive payments for a line of credit, they may choose to eventually sell that credit to a debt collectionagency to get some of their money back. That line of credit will then be reported to the credit reporting bureaus as a collection account—a collections account for a credit card, personalloan, etc.—and

These collectionagencies handle hundreds of thousands of claims. There are also a lot of scam agencies that are not authorized to collect medical debt. You don’t want to pay a debt that isn’t yours or pay the wrong agency. Start by researching the collectionagency. Don’t make this mistake.

On your own, you may not receive approval on a personalloan or car loan. When you have a cosigner with a good credit score, the lender sees loaning to you as less of a risk because the cosigner is also attached to the loan. When you agree to pay off or settle the debt, you can ask for a pay-for-delete letter.

How to Improve Your Credit after Collections Debt Collections FAQ What Is Collections Debt? When you default on a payment, the company you owe may sell your debt to a third-party collectionagency. In other cases, creditors may send you to collections the day after your payment is due. or after 9 p.m.

This is important to understand in case you’re contacted by a collectionagency you don’t recognize. This can happen with credit card debt, unpaid personalloans, or even hospital bills. Some collectionagencies may try to convince you that paying off the full amount of your charge-off will restore your FICO score.

When a lender doesn’t receive payments for a line of credit, like a credit card or personalloan, they may choose to eventually sell that credit to a debt collectionagency to get some of their money back. So if you have a debt in collections, your credit score has likely taken a dip. Here’s how to do it.

TrueAccord proved more effective for late-stage collections and better aligned with online lender’s empathetic approach to financial services. For one online lender, providing online personalloans to underserved consumers was not only a core service for their business but also a key part of their company mission.

TransUnion recently released a report on the state of Collections in 2020. There are fewer third-party collectionsagencies. The number of collection firms has been in decline since 2011, from 9,400 to 7,401 in 2018. The economic downturn has not yet translated into elevated delinquency rates for consumer loans.

Personalloans: Although your family or friends who helped you out will not be thrilled to hear this, these are discharged. Payday” type loans. Collectionagency bills. It simply means that any rent that is owed from before you filed bankruptcy will be discharged.

Luckily, hiring a reliable debt collectingagency can serve you great help in cases where you find it difficult to recover your debts. Some top-notch debt collector professionals specialize in matters associated with personalloans, credit cards, and remission of payment. Legitimacy. Skip tracing system. Fees and costs.

Bankruptcy will wipe out credit card debt, medical bills, and personalloans, but will not eliminate primary obligation debt; things like student loans, child and spousal support, and newer tax debt. Bankruptcy can also stop or delay a home or mortgage foreclosure, stop collection actions, stop garnishments and lawsuits.

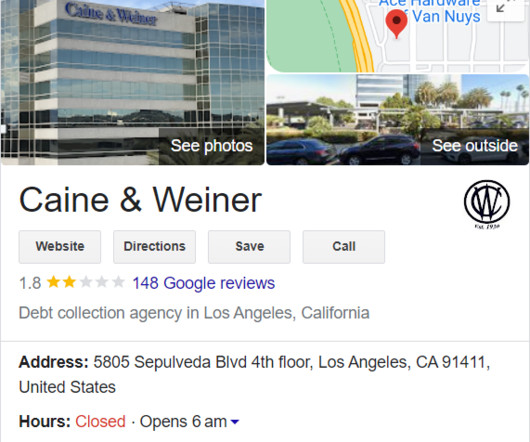

This is Caine and Weiner, a collectionagency. Contact Details Address: Caine and Weiner 5805 Sepulveda Blvd 4 th floor, Los Angeles, CA 91411, United States Phone: +1 818-902-4255 Caine and Weiner History Caine and Weiner is a debt collectionagency founded in 1930 by brothers Samuel and Morris Weiner in Los Angeles, California.

Unpaid medical debt in collections will still remain on your credit report for seven years from the original delinquency date. Any time you are contacted by a collectionagency, you have the right to written confirmation of the debt as well as the right to dispute it. Tips for Dealing with Medical Bills.

The growing complexity of financial products, such as credit cards, mortgages, and student loans, has led to a surge in outstanding debts. This presents a substantial opportunity for debt collectionagencies to assist lenders in recovering unpaid debts and managing default risks.

typical Business borrowing, e.g. overdraft, bank loans, vehicle finance etc. Money invested in the business by directors or others, usually in the form of cash, personalloans, or personal guarantees. The most cost effective form to recover unpaid debts is by working with a Professional Debt CollectionAgency.

Consumer Debt Collection Basics Consumer debt collection describes debts that are owed by individuals, which can include anything from credit card balances and old utility bills to personalloans, medical debt, and mortgages.

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York , leading to a shift in consumer spending for 2024.

Some examples of debt are mortgages, credit card dues, and personalloans. Although accruing lots of debt isn’t ideal, it may sometimes be unavoidable, such as mortgage payments or student loans. They may still be responsible for paying a portion of the loan. These may include: contact from a collectionsagency.

First, collection accounts or debts leading up to your eviction do appear on your credit report. If you fell behind on rent and tried to right the situation with a personalloan that you also fell behind on, for example, that could hurt your credit.

The creditor closes your account, which could be a personalloan, credit card, revolving charge account or another debt you’ve failed to pay as promised, and it’s charged off as a bad debt. If you make payments that are less than the monthly minimum amount due, your account can still be charged off as bad debt.

FNB Omaha is not a scam or a debt collectionagency. Short for the First National Bank of Omaha, FNB National is a popular bank for several personal and professional financial services and products, including: Banking. Home loans. Auto loans. Personalloans. Student loan refinancing.

Unsecured debt would include things like: Medical bills Credit card bills Utility bills Back rent Personalloans At the end of the bankruptcy process, the remaining balances for these types of unsecured debts will likely be forgiven.

Personalloans. Payday” type loans. Collectionagency bills. Overdue utility bills: This doesn’t mean that you will be absolved of all future utility bills, but it does prevent utility companies from being able to shut off your water or electricity because of past bills. Rent that is past due.

If the lender hired a collectionagency, the same debt may appear twice on your credit file, exacerbating the problem even more. If you make on-time payments on your other credit cards and personalloans, your good payment history will start to compensate for the bad, softening the blow of the repo.

Reading Time: 4 minutes Being a debt collectionagency, we often receive queries asking for advice as to how one can get themselves out of debt. Whether you’re carrying credit card debt, personalloans, or student loans, one of the best ways to pay them down sooner is to make more than the minimum monthly payment.

The company’s highly knowledgeable debt arbitrators have spent more than a decade forming positive working relationships with several creditors and collectionagencies. It can’t tackle secured debts like auto loans and mortgages. Credit card loans. Personalloans. Collections and repossessions firms.

In many cases, debt settlement companies will wait until your creditors charge off your debt and sell it to a debt collectionagency, which the debt settlement company can then work with. Once your debt is transferred to a collectionagency, you may not be able to negotiate a good rate, and you may be more likely to get sued.

The types of credit accounts you can expect to see in this section include: Mortgages , home equity loans, and home equity lines of credit. Student Loans. Auto Loans. PersonalLoans or Other Installment Loans. This could also mean the same debt appears separately as a collectionagency account.

You can use this strategy with collectionsagencies as well. Take Out a Debt Consolidation Loan Best for: People who want to simplify their debt payments For some, taking out a debt consolidation loan is the best way to pay off credit cards because it can lower your interest and remove credit cards from the equation.

If a debt buyer or collectionagency has violated a consumer protection statute such as the Fair Debt Collection Practices Act (FDCPA)–and they often do–that provides leverage to fight back. The post Debt Collection Lawsuits Are Surging appeared first on Collection Industry News. Negotiating a payment plan.

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York, leading to a shift in consumer spending for 2024.

As adoption of AI continues, progressive debt collectionagencies will leverage information from customer interactions to enhance their collections practices and improve performance. 30-89 day delinquency rates increased by 42.9%

The first step, if you have paid the full collection account, settlement, or have been making regular on-time payments, is to mail the collectionagency a “ goodwill letter ” that explains your situation. Ask the CollectionAgency to Validate the Debt. Anything else that appears to be inaccurate.

While many Buy Now, Pay Later borrowers use the product without noticeable indications of financial stress, the report finds that Buy Now, Pay Later borrowers will more likely become active users of other types of credit products like credit cards, personalloans, and student loans.

While many Buy Now, Pay Later borrowers use the product without noticeable indications of financial stress, the report finds that Buy Now, Pay Later borrowers will more likely become active users of other types of credit products like credit cards, personalloans, and student loans.

Find out about the origin of the debt, such as credit cards, medical bills , or personalloans. This documentation can be helpful if you need to dispute charges or escalate a dispute to a credit bureau or a consumer protection agency.

Here is an extreme situation of a bad actor detailing what the New York State Attorney General would pursue a Debt collection company: Filed in 2020, the NYS Attorney General partnering with the Consumer Fraud Protection Bureau ( CFPB ) shut down a Buffalo collectionagency.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content