This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A District Court judge in Florida has denied a defendant’s motion to dismiss claims it violated the Fair DebtCollection Practices Act and the Florida ConsumerCollections Practices Act in a ruling that seems potentially problematic in terms of the definition of debtcollector and when a debt is in default.

A commercial collection agency is an agency that works to resolve debt between two businesses. Commonly known as B2B debtcollections, it’s the process of mediating financial disputes and overdue invoices owed to a commercial client. You will preserve future revenue by hiring the right commercial collection agency.

The debtcollection industry is a vital part of the US economy. Many small businesses and larger organizations rely on the expertise and efforts of third-party collection agencies every day. Want to know more about why businesses rely so much on professional debtcollection agencies ? And for good reason.

The debtcollection industry is a necessary component of the US economy. Professional collectors provide a critical service to both small businesses as well as nationwide organizations in helping them secure late payments from customers. Part of our economic machine here in this country is proper access to credit for consumers.

To say there is endless misinformation about debtcollections in the media and on the Internet would be a vast understatement. Right up front, you should know that the debtcollection industry provides critical and necessary support to not only consumers and the business community but the overall economy.

There is a lot of important work done by reputable and professional debtcollectors daily in this country. This work helps the overall economy, consumers that may be struggling with ongoing debt, and small businesses struggling to meet payroll and other expenses. The debtcollection industry touches just about everyone.

The Consumer Financial Protection Bureau (CFPB) has more to do with your debtcollection claim than you might think. Professionally, your business may deal with consumers directly or indirectly. Personally, CFPB has a lot to do with how companies approach you to collectdebt and other financial products.

More details here. WHAT THIS MEANS, FROM BRIT SUTTELL OF BARRON & NEWBURGER: This is an interesting case that was probably not well suited for a Motion to Dismiss.

Businesses throughout Florida should be aware of consumer statutes that provide remedies to consumers and impose liability to businesses, even for small technical violations. Fair DebtCollection Practices Act. For example, a debtcollector cannot: use violence or make repetitive telephone calls (15 U.S.C.

Debtcollectors can now contact consumers on social media. Here’s the background and all you need to know about what debtcollectors can and can’t do on social media. In November 2021, The CFPB made some long-awaited updates to the Fair DebtCollection Practices Act. Yes, it’s true.

In a decision that could throw the debt-collection industry into turmoil, on April 21, 2021, the Eleventh Circuit Court of Appeals released its opinion in the case Hunstein v. Preferred Collection & Mgmt. Compumail used this information to create, print, and mail a dunning letter to the consumer.

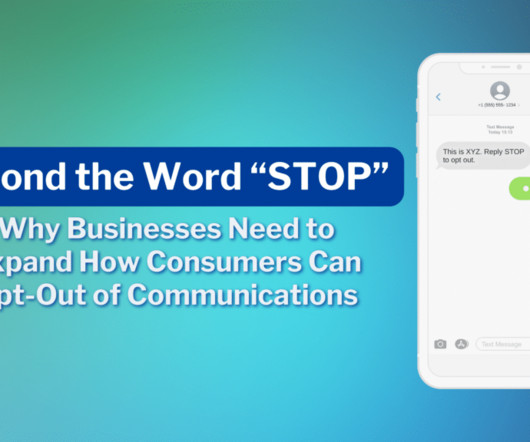

In todays digital communication landscape, businessesespecially those that use digital outreach to engage delinquent consumers to collect debtsare facing increasing pressure to ensure they respect consumers opting out of communications from a particular channel.

Business to business debtcollection can be hard to understand at first. Check out this guide on who should use commercial debtcollections. Even when you try to send customer debtcollection requests, they have fallen on black days. This type of debtcollection can be hard to understand at first.

The settlement of debts acquired by either another company or an individual is one of the most common challenges that businesses experience. Collectingdebts is time-consuming, especially if the debtor refuses to cooperate. What they can and cannot do when doing so are regulated by the Fair DebtCollection Practices Act.

Does the Consumer Financial Protection Bureau (CFPB) have the power to tell debtcollectors to turn over their attorney-client privileged communications? Thus, the Bureau effectively believes it can obtain the privileged documents of any debtcollector in the country. The answer may depend on who you ask.

When your debt goes into collections, it’s important to straighten things out quickly. If BYL Collections has been contacting you, the information below can help you move forward. How Does BYL Collection Services Work? Based in Westchester, Pennsylvania, BYL is a third-party collections agency that was founded in 1998.

There are a number of new developments in New York State legislation that will change New York debtcollection law and likely impact your receivables and collection claims, and ultimately your bottom line. There is one change that is most significant and, if you are working with consumers, will directly affect you.

The Consumer Financial Protection Bureau (CFPB) today took action against a medical debtcollector, Commonwealth Financial Systems, for illegally trying to collect unverified medical debts after consumers disputed the validity of the debts. WASHINGTON, D.C. – Read today’s order.

The Florida ConsumerCollection Practices Act (FCCPA) is a pro-consumer statute. Unlike the FDCPA, which only applies to debtcollectors, the FCCPA applies to all persons or businesses collectingconsumerdebts.

Section 1692(f) of the FDCPA prohibits a debtcollector from using unfair or unconscionable means to collect any debt, and enumerates specific examples of prohibited conduct. Among other things, the term “debtcollector” does not include “any person collecting or attempting to collect any debt owed or due.

If you are a collection professional working for a creditor, debt buyer, collection agency or collection law firm, and you have not yet added the website for the Consumer Financial Protection Bureau (CFPB) to the favorites on your web browser, it is high time that you do so.

Enloe Section 1692a(3) defines a consumer as any natural person obligated or allegedly obligated to pay a consumerdebt. The final debtcollection rule interprets the definition of a consumer to include deceased natural consumers, as well. Debt Validation Notice. By Caren D.

After receiving notice of representation, the defendant sent five billing notifications to the plaintiff and made six telephone calls attempting to collect on the $5 monthly payment. This same evidence also supported findings that the plaintiff was financially vulnerable and that the defendant had engaged in repeated collection activity.

Court of Appeals for the Eleventh Circuit recently held that periodic statements required by the federal Truth in Lending Act may violate the federal Fair DebtCollection Practices Act if they are not truthful and fair. Source: site. A copy of the opinion in Lamirand, et al v. Fay Servicing, LLC is available at: Link to Opinion.

Attorneys and other entities that regularly engage in collection work for community associations may be subject to the requirements of the Fair DebtCollection Practices Act, 15 U.S.C. as well as analogous state laws governing the consumercollection process. The issue in Ho v.

Federal Activities: On July 1, the Consumer Financial Protection Bureau (CFPB or Bureau) released a new complaint bulletin covering several areas of concern on relief provided in response to the COVID-19 pandemic, including the Centers for Disease Control and Prevention (CDC) eviction moratorium. For more information, click here.

Financial institutions, servicers, lenders, and debtcollectors must stay up-to-date on evolving federal and state laws stemming from the COVID-19 pandemic, as such laws impact all facets of consumer loan servicing and debtcollection.

The plaintiff claimed that this late-hour email violated both the FDCPA and the Florida ConsumerCollection Practices Act (FCCPA), which restrict communications with consumers outside certain hours. Specifically, under both acts, a debtcollector may not communicate with a consumer between 9 p.m.

Established by the Economic Growth, Regulatory Relief, and Consumer Protection Act, IPAC consists of 21 members, who serve staggered three-year terms and bring professional backgrounds in insurance accounting, actuarial science, academia, insurance regulation, and policyholder advocacy. For more information, click here.

The new law limits a collection agency’s ability to collect on medical debt. The proposed amendments include changing the definition of medical debt, allowing medical debtors to initiate contact and make voluntary payments, and preventing certain written communications from being sent via certified mail.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content