This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The South Carolina Supreme Court has changed its mind and will not issue a ruling in a case over whether a debt collector is required to send a right-to-cure notice to a consumer under state law before filing a lawsuit to collect on an unpaid debt.

Gordon of the District Court for the District of Nevada ruled that the defendant, a debtcollection law firm, lacked the necessary minimum contacts with Nevada to establish personal jurisdiction. The background: The case stemmed from a consumercreditcarddebt judgment originally obtained in Tennessee by a creditor.

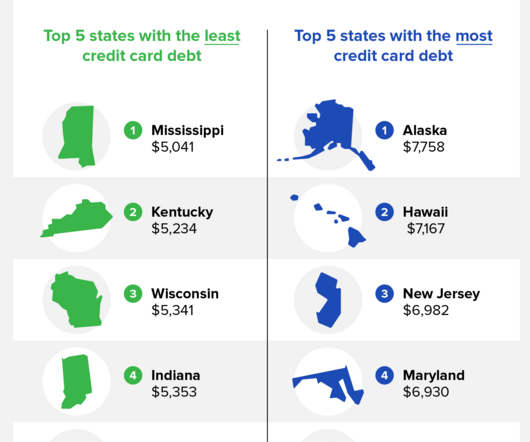

The average household creditcarddebt in America is $9,654, and the states with the largest amount of creditcarddebt are Alaska, Hawaii, and New Jersey. Between the first quarters of 2022 and 2023, The Federal Reserve Bank of New York reported that the creditcarddebt in America rose by $145 billion.

The average household creditcarddebt in America is $9,260, and the states with the largest amount of creditcarddebt are Alaska, Hawaii, and New Jersey. Between the first and final quarter of 2022 , TransUnion® reported that the average American’s creditcarddebt rose roughly $400 per person.

Today, about 61% of American households have creditcarddebt and the average creditcarddebt balance sits at $5,875. Plus, 71% of consumers expect personalized experiences, which means one-size-fits-all outreach isn’t going to cut it in collections.

We are entering a year of unknowns across the board, from potential regulatory changes to economic fluctuations to varying consumer sentiments, and theres a lot to consider as it relates to debtcollection in 2025. Whats Impacting Consumers? What Does This Mean for DebtCollection?

The Consumer Financial Protection Bureau released its fifth biennial report to Congress today on the consumercreditcard market, finding that the market’s growth over the last few years reversed course in 2020.

Mix in the fact that many consumers – enabled, in part, by historic levels of savings at least partly driven by government stimulus such as enhanced unemployment benefits – have shifted their focus to paying down their creditcarddebt, and the result is a greater than 10% decrease in the average creditcard balance and utilization of the U.S.

consumers took on $43 billion in additional creditcarddebt during the second quarter of this year, ending in June. That’s more than triple the average amount of new debt households have taken on in that period since after the Great Recession of 2007-08. Newly released data from WalletHub says U.S.

KNOXVILLE, Tennessee — The Federal Reserve Bank of New York has been tracking creditcarddebt since 1999. Creditcarddebt in the U.S. is at the highest level it’s been since then, with the total amount of debt in the third quarter of 2023 reaching around $1.08 trillion dollars. The post U.S.

With uncertainties about how the end of various pandemic-era benefits will impact consumers, it’s more important than ever for creditors and collectors to implement strategies that consider consumer situations and preferences when attempting to collect. What’s Impacting Consumers and the Industry?

Creditcard balances reached a record-setting $866 billion in the third quarter of last year, which represents a year-over-year increase of 19%. Credit balances reached a record-setting $866 billion in the third quarter of last year – and they are expected to keep climbing, the report from TransUnion said.

Does Colorado Law Protect Me From Debt Collectors? When collecting a debt from you, collection agencies must adhere to federal and state rules. Fortunately, the federal Fair DebtCollection Practices Act (FDCPA) protects all states. What is the Federal Fair DebtCollection Practices Act (FDCPA)?

Today, about 61% of American households have creditcarddebt and the average creditcarddebt balance sits at $5,875. Plus, 71% of consumers expect personalized experiences, which means one-size-fits-all outreach isn’t going to cut it in collections.

Interest rates on creditcards have risen substantially, with average interest rates going over 20% . Given the trends for the 175 million Americans with creditcards, the CFPB estimates that outstanding creditcarddebt may continue to set records and could even hit $1 trillion.

The Consumer Financial Protection Bureau has issued a series of orders to five companies offering “buy now, pay later” credit. The orders to collect information on the risks and benefits of these fast-growing loans went to Affirm, Afterpay, Klarna, PayPal, and Zip.

The report shows a slight uptick in total household debt in the second quarter of 2023, increasing by $16 billion (0.1%) to $17.06 The report is based on data from the New York Fed’s nationally representative ConsumerCredit Panel. The post Total Household Debt Reaches $17.06 trillion in the Q2 2023, marking a 4.6%

And that’s because it generally takes a few months for the effects of that event and the accompanying financial strain to start to show up in consumers’ credit reports, in the form of rising balances, credit seeking behavior, and eventually for some, missed payments. As of July 2020, U.S. FICO® Score over the coming months.

Information and data continue to be key tools at our disposal to better understand the dynamics of the last couple of years, and better navigate what lies ahead for the Canadian consumercredit environment. Average FICO® Score 10.

This is where they come into play—things like making loan and creditcard payments on time each month and maintaining a good debt usage or a credit utilization rate—the amount of debt, including creditcarddebt, you have in relation to your overall credit limit—can help you reach the credit score you’re after.

As the independent standard in credit scoring, FICO® Scores are the leading credit scores used extensively across the lending ecosystem ranging from originations, underwriting and account management to collections and asset-backed securitization. Ethan has a B.S. in management science/operations research from UC San Diego.

As the federal funds rate rose, the prime rate did, as well, and creditcard rates followed suit. Why creditcarddebt keeps rising Despite the steep cost, consumers often turn to creditcards, in part because they are more accessible than other types of loans, according to Matt Schulz, chief credit analyst at LendingTree.

The report shows total household debt increased by $109 billion (0.6%) in Q2 2024, to $17.80 The report is based on data from the New York Fed’s nationally representative ConsumerCredit Panel. It includes a one-page summary of key takeaways and their supporting data points.

The report shows total household debt increased by $184 billion (1.1%) in the first quarter of 2024, to $17.69 The report is based on data from the New York Fed’s nationally representative ConsumerCredit Panel. The Quarterly Report also includes a one-page summary of key takeaways and their supporting data points.

Chapter 7 bankruptcy offers a fresh start by eliminating most unsecured debt. This helps improve cash flow and break the cycle of high-interest debt. The automatic stay protects from most collection efforts. However, some debts like child support and tax delinquencies can still be garnished, and violations may occur.

News & World Report shows that more than eight in 10 Americans who have creditcarddebt are experiencing anywhere from a little to a lot of anxiety about it. Nearly 31% have at least $6,000 of creditcarddebt. have creditcarddebt of $10,000 or more.

Creditcard borrowing rose in November to its highest monthly level since 2004 according to latest Bank of England data. billion in all forms of consumercredit, an increase on the £700m borrowed in October, of which £1.2 Net borrowing of mortgage debt by individuals increased from £3.6 billion to £4.4

The CFPB also found that while small institutions with overdraft programs charged lower fees on average, consumer outcomes were similar to those found at larger banks. The research notes that, despite a drop in fees collected, many of the fee practices persisted during the COVID-19 pandemic. For more information, click here.

As discussed here , on July 7th the Consumer Financial Protection Bureau (CFPB), U.S. Department of Treasury (collectively, the agencies) jointly issued a Request for Information (Request) seeking public comment on medical creditcards, loans, and other financial products used to pay for health care.

“We did have a crisis,” said Brian Riley, director of credit advisory services at Mercator Advisory Group, “but because of the support that was given, it really kept the market for consumercredit steady.”. He added that card issuers behaved “a lot more rationally” in comparison with the 2007-2009 crisis.

Using the CFPB’s Making Ends Meet survey and consumercredit data, CFPB researchers found that financial conditions faced by renters and homeowners were divergent before the pandemic. The post CFPB Says Renters At Risk As Pandemic Safety Net Ends appeared first on Collection Industry News. Renters represent over 30% of U.S.

Americans borrowed a lot more money in May, according to new data from the Federal Reserve’s ConsumerCredit Report released in July. There was a 10% increase in credit use on a seasonally adjusted annual basis in May 2021. In May 2021, the total outstanding balance of consumercredit hit $4.25

A periodic survey by Bankrate found that 47% of cardholders carried debt from month to month in mid-2023, up from 39% at the end of 2021. The average card customer holds $6,088 in debt, according to a TransUnion report for the third quarter of 2023, up from $5,474 at the same time in 2022.

And that’s because it generally takes a few months for the effects of that event and the accompanying financial strain to start to show up in consumers’ credit reports, in the form of rising balances, credit seeking behavior, and eventually for some, missed payments. As of July 2020, U.S. FICO® Score over the coming months.

Circuit Court of Appeals ruled that the Fair Credit Reporting Act does not require consumercredit agencies to further investigate when a borrower disputes a debt collector’s ownership of their debt. Attorneys for the borrowers and credit agencies did not immediately reply to requests for comment on Friday.

FICO® Score At 716, Indicating Improvement In ConsumerCredit Behaviors Despite Pandemic. Ethan Dornhelm wrote: The FICO® Score is the lingua franca, or common language, for the credit scoring industry. It serves as a broad-based, independent standard measure of credit risk. Fewer consumers are actively seeking credit.

Medical debt is still a uniquely American problem. of Americans had medical debt in collections as of June 2020, according to a study from the Journal of the American Medical Association (JAMA), which analyzed consumercredit reports between January 2009 and June 2020. Source: site. An estimated 17.8%

Fico XD helps young adults, immigrants, and those with past credit challenges that resulted in closing all credit accounts. In the last 30 years, the Fair Isaac and Company, better known as FICO, changed the way the lenders evaluate consumer applications. What Factors Does the FICO XD Consider.

The FICO Blog posts last year reflected that – we wrote about everything from the impact on collections, proactive lender communications with consumers, issues with fraud, and of course, how FICO® Scores were impacted. We hope that what readers learned helped instill confidence in keeping credit flowing during uncertain times.

A hike in the federal interest rate prompts a jump in the Bank Prime Loan Rate ( prime rate ), the credit rate that banks offer to their most credit-worthy customers and off of which they base other forms of consumercredit like mortgages and consumer loans.

Issuers will likely turn off the spigot of generous incentives and easy credit in 2023 in response to a weaker economy, according to analysts. We spoke to credit experts about emerging creditcard trends, how they may impact consumers and how you can prepare. People might find themselves in more creditcarddebt.

Some lawmakers and regulators are calling for interest rate caps and lower fees on creditcards as debt levels march higher. Total creditcarddebt topped $1 trillion in the second quarter of 2023 for the first time ever. Federally chartered credit unions have an 18% limit. For example, Sen.

On October 25, the CFPB released its biennial report to Congress on the consumercreditcard market. The report found that in 2022 creditcard companies charged consumers more than $105 billion in interest and more than $25 billion in fees. For more information, click here. For more information, click here.

On May 1, the Federal Trade Commission (FTC) announced a permanent ban from debt relief telemarketing for operators of debt relief scam. The FTC charged the defendants with taking tens of millions of dollars from people by falsely promising to eliminate or substantially reduce their creditcarddebt.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content