This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Consumer Financial Protection Bureau has agreed to end a lawsuit by joining industry groups in asking a federal judge to vacate its controversial rule banning the reporting of medical debt on consumercredit reports. If it does, the rule will be vacated, and the CFPB will be barred from enforcing it.

A federal judge has approved a motion allowing two individuals and two consumer advocacy organizations to intervene in the legal fight over the Consumer Financial Protection Bureaus rule banning medical debt from consumercredit reports.

Appeals Court Reverses Arbitration Ruling for Defendant in Collection Case A New Jersey Appeals Court has overturned a lower courts ruling in favor of a defendant that had granted arbitration in a collection lawsuit more than a year after the complaint had been filed and litigated. More details here.

We are entering a year of unknowns across the board, from potential regulatory changes to economic fluctuations to varying consumer sentiments, and theres a lot to consider as it relates to debt collection in 2025. Whats Impacting Consumers? What Does This Mean for Debt Collection?

For creditunions and smaller banks in North America, the challenge of how to compete with their bigger counterparts is a constant and pressing matter. Today’s prescreening solutions are very manual in nature, typically involving a list processing agreement with a credit bureau.

Today, you have six years to collect monies owed from consumercredit transactions. However, a bill approved by the New York Senate seeks to shorten the time to collectconsumercredit transactions to three years. Creditunion loan. Credit cards. Personal bank loans. Home equity loans.

Bankers are opposing any effort by the Consumer Financial Protection Bureau (CFPB or Bureau) to reduce or eliminate the late fee safe harbor, citing a potentially significant adverse impact on community banks and creditunions.

After New York Governor Andrew Cuomo signs the ConsumerCredit Fairness Act (S.153/Thomas) 153/Thomas) into law, many creditors will need to provide significant documentation in order to file a debt collection action against their non-paying consumers. The New Consumer Debt Collection Requirements.

FICO® Score 10 and 10 T provide a precise assessment of consumercredit risk on all credit product lines, including mortgages, auto loans, credit cards and personal loans. Also the backwards compatibility of FICO® Score 10 ensures more seamless lender adoption since it utilizes the same score reason codes.

For creditunions and smaller banks in North America, the challenge of how to compete with their bigger counterparts is a constant and pressing matter. Today’s prescreening solutions are very manual in nature, typically involving a list processing agreement with a credit bureau.

Federal Activities: On December 16, the Consumer Financial Protection Bureau (CFPB) issued a series of orders to five companies offering “buy now, pay later” (BNPL) credit. The CFPB is concerned about accumulating debt, regulatory arbitrage, and data harvesting in a consumercredit market already quickly changing with technology.

Experian reports that the lowest FICO credit score is 300, but no one really stays at such a low score once some financial history has been established. If you’re not in the habit of checking your credit score every month, you can hire a credit monitoring company to do the tracking for you. And that’s encouraging to think about.

The bureaus collect and store your credit information in your credit file for future reference. The bureaus collect and store your credit information in your credit file for future reference. Meaning, your behaviors can be reviewed in the future by others to determine your risk level.

In letters dated August 1, the American Bankers Association , Consumer Bankers Association, CreditUnion National Association, and National Association of Federally?Insured Insured CreditUnions (Associations), as well as the Bank Policy Institute , expressed their collective displeasure with the idea.

Despite objections from CUNA and NAFCU, the House of Representatives passed the Comprehensive Debt Collection Improvement Act on Thursday. In the letter, Nussle stated, “Lenders rely on complete and accurate credit reports when underwriting loans. Source: site. The bill, H.R. Maxine Waters (D-Calif.),

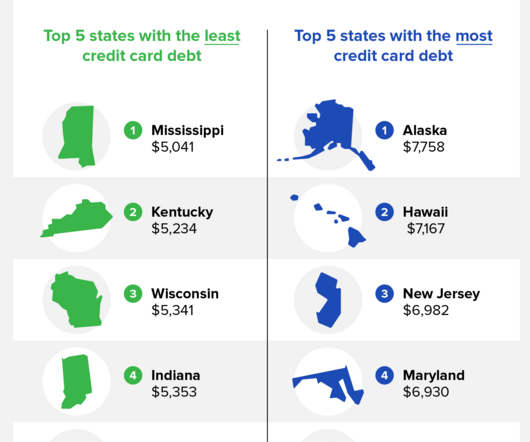

Despite the national average of Americans having over $9,000 in credit card debt per household, only 14% say they’re “very worried” about their debt. 67% of respondents said they have less than $2,000 in debt, which may indicate that only a concentrated number of people have high amounts of credit card debt.

On October 11, the Consumer Financial Protection Bureau (CFPB) issued an advisory opinion concerning consumers’ requests for information regarding their accounts with large banks and creditunions. million, allegedly collecting about $81,000 of that amount. For more information, click here.

There are some exceptions: The Military Lending Act caps interest for active duty servicemembers and dependents at 36% for consumercredit. Federally chartered creditunions have an 18% limit. Eight trade groups representing lenders such as banks and creditunions wrote a letter to Sen. For example, Sen.

The revamped survey will mean that dominant credit card issuers will be more transparent by requiring them to publish average interest rates based on credit score ranges. Small banks and creditunions will also now have a chance to have their prices displayed next to those of the largest ones.

Despite the national average of Americans having $9,000 in credit card debt per household, only 14 percent say they’re “very worried” about their debt. 67 percent of respondents said they have less than $2,000 in debt, which may indicate the national average means that a concentrated number of people have high amounts of credit card debt.

The legislation would benefit banks and creditunions with assets under $15 billion. On October 23, lawmakers in the House of Representatives introduced a bill to exclude Paycheck Protection Program (PPP) loans from regulators’ calculations of the asset size of smaller banks. For more information, click here.

The insured creditor and its affiliates do not maintain an escrow account for consumercredit transactions secured by real property or a dwelling, other than: Escrow accounts established after consummation as an accommodation to distressed consumers to assist such consumers in avoiding default or foreclosure, or.

The DFPI is aggressively exercising its new authority to regulate a large group of newly covered financial services, including debt collectors, credit reporting and credit repair agencies, debt relief agencies and others. Consumers can reach the DFPI at (866) 275-2677 or Ask.DFPI@dfpi.ca.gov.

The DFPI investigations resulted in 49 public enforcement actions, $975,000 in restitution to consumers, $547,500 in penalties, and included several “first of its kind” actions for the DFPI in debt collection, student debt relief, earned wage access, and private post-secondary education financing. Regulatory Activities.

Two trade groups the Consumer Data Industry Association (CDIA) and the Cornerstone CreditUnion League yesterday filed a lawsuit in the District Court for the Eastern District of Texas against the Consumer Financial Protection Bureau over its new rule prohibiting the inclusion of most medical debts on consumercredit reports.

A federal judge has granted a 90-day stay on the Consumer Financial Protection Bureaus new rule that would bar credit reporting agencies from including medical debt on consumercredit reports.

Covered institutions include banks, savings associations, creditunions, and mortgage companies. As the most comprehensive publicly available information on mortgage market activity, HMDA data is used by industry, consumer groups, regulators, and others to assess potential fair lending risks and for other purposes.

On June 8, the board of governors for the Federal Reserve (the Fed), Consumer Financial Protection Bureau (CFPB), Federal Deposit Insurance Corporation (FDIC), National CreditUnion Administration (NCUA), and the OCC requested public comment on proposed guidance addressing reconsiderations of value (ROV) for residential real estate transactions.

million to consumers and pay a $500,000 civil penalty for deceiving consumers with false claims about their services. That information will be posted in a registry and open to the public, including to other consumer financial protection enforcers. For more information, click here. For more information, click here.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content