This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As result of FTC lawsuit, federal court issues temporary restraining order halting scheme that sent fictitious debt collection notices to consumers nationwide As a result of a Federal Trade Commission lawsuit, a federal court hastemporarily haltedthe operations and frozen the assets of a phantom debt collection scheme and its operators.

We are entering a year of unknowns across the board, from potential regulatory changes to economic fluctuations to varying consumer sentiments, and theres a lot to consider as it relates to debt collection in 2025. Whats Impacting Consumers? What Does This Mean for Debt Collection?

It’s important you verify the information contained in a debt collection affidavit before you sign it. An affidavit is sworn testimony used to support your debt collection case. Chase was one of 13 financialinstitution censured for robo-signing documents in support of debt collection suits and foreclosure.

Why does the credit repair industry exist? As long as data is being collected for credit reports, there’s room for mistakes. They could be the difference in someone qualifying for different credit lines or not. So credit repair, consumercredit and credit bureaus—they’re all tied together.

The UK’s Financial Conduct Authority (FCA) has handed out a £26m fine following poor treatment of more than 1.5 It marks the highest fine ever issued to a lender for what it deemed a breach of consumercredit rules. But those needing to collect from customers will also be facing significant regulatory scrutiny.

Read on for our take on what’s impacting consumer finances, how consumers are reacting and what else you should be considering as it relates to debt collection in 2024. What’s Impacting Consumers? What Does This Mean for Debt Collection? from a year ago. Don’t skimp on compliance.

With average consumer total spend at its highest and late payments rising significantly month-on-month and year-on-year, financialinstitutions will be particularly concerned as the focus on Consumer Duty heightens.

There are several key consumer laws that collectors should be concerned with when engaging in debt collection practices. These laws aim to protect consumers from unfair, deceptive, or abusive practices. Here are some important consumer laws that collectors should be familiar with: 1.

Today’s prescreening solutions are very manual in nature, typically involving a list processing agreement with a credit bureau. The solution integrates Equifax ConsumerCredit Information and FICO risk decision management technology with marketing campaign automation and execution. Learn more about PrescreenCentral.

Today’s prescreening solutions are very manual in nature, typically involving a list processing agreement with a credit bureau. The solution integrates Equifax ConsumerCredit Information and FICO risk decision management technology with marketing campaign automation and execution. Learn more about PrescreenCentral.

Credit Risk and FICO Score Trends? economy, credit scores, and credit risk trends were headed. government and financialinstitutions to implement significant guard rails and safety net programs for consumers such as the government stimulus, extended unemployment benefits, and payment accommodations.

On March 15, the ConsumerFinancial Protection Bureau (CFPB) issued a Request for Information (Request) seeking public comment on the business practices of data brokers and how they impact the daily lives of consumers. This data will be used to inform the CFPB’s planned rulemaking under the Fair Credit Reporting Act (FCRA).

It requires federal regulators to exclude PPP loans from asset-size calculations for the purpose of determining capital ratios, deposit insurance premiums, and other asset thresholds at those financialinstitutions. For more information, click here. For more information, click here. For more information, click here.

On January 20, 2023, California Attorney General Rob Bonta submitted a letter to the CFPB agreeing with its preliminary determination that California’s Commercial Financing Disclosures Law (CFDL) is not preempted by TILA because the CFDL only applies to commercial financing and not to consumercredit transactions within the scope of TILA.

The FTC’s Safeguards Rule requires nonbanking financialinstitutions, such as mortgage brokers, motor vehicle dealers, and payday lenders, to develop, implement, and maintain a comprehensive security program to keep their customers’ information safe. financialinstitutions. For more information, click here.

In letters dated August 1, the American Bankers Association , Consumer Bankers Association, Credit Union National Association, and National Association of Federally?Insured Insured Credit Unions (Associations), as well as the Bank Policy Institute , expressed their collective displeasure with the idea.

What’s more, unlike some fintech initiatives that assess risk based on cash flow data alone, the UltraFICO® Score presents the best of both worlds, combining cash flow data with traditional data from consumers’ credit files, along with the odds-to-score ratio that lenders understand. In her role, Ms.

Specifically, the Panel is required to collect advice and recommendations from small entities or their representatives … that are likely to be subject to the regulation that the CFPB is considering proposing.” When set appropriately, late fees encourage consumers to pay on time and develop good financial management habits.

On July 27, the Senate passed its version of the National Defense Authorization Act (NDAA) bill, which includes a provision that tightens oversight over financialinstitutions engaged in crypto trading and takes aim at crypto mixers and “anonymity-enhancing” crypto assets. The amendment, led by U.S. For more information, click here.

Saxon Shirley Fri, 05/20/2022 - 06:06 by FICO expand_less Back To Top Tue, 02/07/2023 - 19:10 As the independent standard in credit scoring, FICO® Scores are the leading credit scores used extensively across the lending ecosystem. million previously “unscorable” consumer files. Read the full post 3. Read the full post 4.

Thus, those who make, procure, or advertise EWA products are not required to be licensed as a “consumer lender” by Arizona’s Department of Insurance and FinancialInstitutions. The AG’s findings apply to EWA providers working with an employer as well as those working directly with an employee.

Notably, this poll took place before the recent liquidity challenges faced by several financialinstitutions. But they view their own companies’ financial outlook more positively. 14% said the financial outlook for their company was very strong, and another 50% assessed the outlook as strong. In her role, Ms.

A Pre-Screen Firm Offer of Credit, often referred to as pre-approved credit, is a marketing strategy employed by creditors to identify potential customers for their financial products. This process involves a preliminary screening of consumercredit reports to determine if individuals meet specific criteria set by the lender.

On November 6, the Bank of England, Financial Conduct Authority, and Prudential Regulation Authority issued guidance explaining how current and proposed regulatory regimes governing “e-money, stablecoins, and tokenised bank deposits” will interact, indicating that applicable financialinstitutions will be subject to dual or triple regulation.

The COVID-19 pandemic cast a huge shadow on the financial services worldwide. The FICO Blog posts last year reflected that – we wrote about everything from the impact on collections, proactive lender communications with consumers, issues with fraud, and of course, how FICO® Scores were impacted.

While you may have applied for a loan from a popular lender or bank, their name isn’t necessarily the one that will appear on your credit report. Instead, banks, lenders, and other financialinstitutions turn to consumercredit reporting companies like CBCInnovis to vet applicants. Debt in collections.

The CFPB also released several reports shining a light on factors that may influence fair access to credit, including how medical debt affects tens of millions of consumers’ credit profiles, how people in under-resourced rural areas struggle to access financial services, and the challenges faced by justice-involved individuals and families.

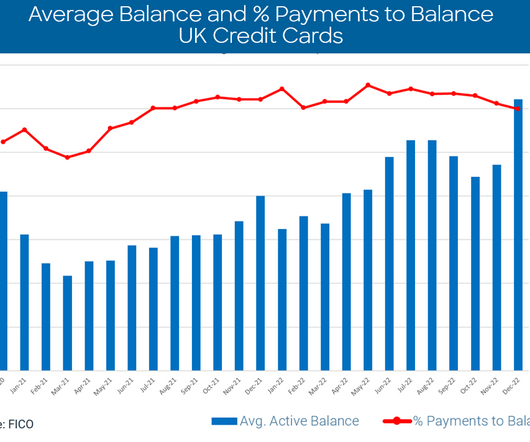

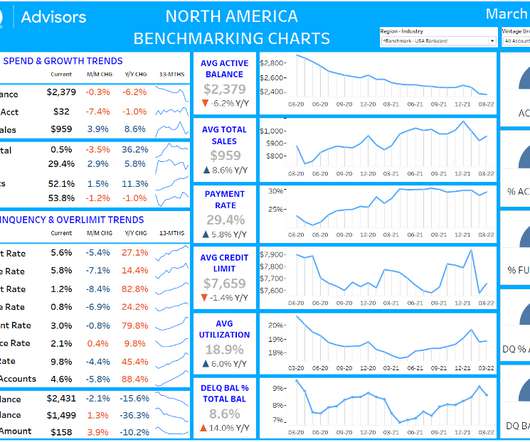

In turn, Financialinstitutions are raising interest rates on consumer debt including the 30-year fixed mortgage, up from 3.22% in January 2022 to 5.30% as of May 12th. Leanne Marshall is a Senior Strategy Consultant with FICO Advisors for North American Credit Risk Lifecycle Practice.

On October 11, the CFPB published its analysis regarding the nonsufficient fund (NSF) fee practices of a number of banks and credit unions. NSF fees are distinct from overdraft fees, which financialinstitutions charge when they pay, rather than decline, a payment when the account lacks sufficient funds.

are part of this program, where FICO Scores used by financialinstitutions are shared with consumers for free. Through that program, and many other ways for the consumers to access their FICO® Score, we offer reason codes and educational material to provide insight to the consumer on their score.

Surprisingly, the violations identified by the CFPB have very little if anything to do with credit reporting. Instead, the orders are focused on the CRAs’ marketing of credit related reporting services. According to the Consent Orders, the CRAs marketed and sold consumerscredit scores and credit related products.

The first of its kind, the strategy examines the phenomenon of financialinstitutions de-risking and its causes, and it identifies those greatest impacted. Department of the Treasury issued the 2023 De-Risking Strategy, as mandated by Congress in the Anti-Money Laundering Act of 2020. For more information, click here.

UK Credit Card Borrowing Soars to Highest Monthly Level Since 2004 Credit card borrowing in the UK soared in November to its highest monthly level since 2004 amid mounting pressure on households from the cost of living crisis. Regulators Warn Banks over Cryptocurrency Risks U.S.

The proposed guidanceadvises on policies that financialinstitutions may implement to allow consumers to provide financialinstitutions with information that may not have been considered during an appraisal or if deficiencies are identified in the original appraisal. For more information, click here.

According to the Fed, “Stablecoins that are not backed by safe and sufficiently liquid assets and are not subject to appropriate regulatory standards create risks to investors and potentially to the financial system, including susceptibility to potentially destabilizing runs.” financialinstitutions. To read more, click here.

Senate Committee on Banking held a full committee hearing, titled “Oversight of the Credit Reporting Agencies.” Chairman Sherrod Brown (D-OH) described consumercredit reports as “riddled with errors.” Brown argued that medical debt “correlates with illness,” not with credit risk. On April 27, the U.S.

The new agenda lists two items as in the “final rule stage”: Debt collection. Due in part to the “societal disruption” caused by the COVID-19 pandemic, in April 2021, the CFPB issued a notice of proposed rulemaking (NPRM) that would extend by 60 days the effective date of Part I and Part II of its final debt collection rule.

Department of the Treasury’s Community Development FinancialInstitutions Fund (CDFI Fund) opened the fiscal year 2021 funding round for the CDFI Rapid Response Program today. billion to community development financialinstitutions to help their communities respond to the economic hardships created by the COVID-19 pandemic.

Federal Activities: On September 29, the ConsumerFinancial Protection Bureau (CFPB) released its fifth biennial report to Congress on the consumercredit card market, finding that the market’s growth over the last few years reversed course in 2020. Privacy and Cybersecurity Activities. For more information, click here.

Department of the Treasury (Treasury) launched an inquiry into specialty financial products, such as medical credit cards and installment loans, that consumers can use to pay for medical care. The CFPB further alleged that the defendants made guarantees about lowering consumers’ credit card interest rates.

On April 14, the ConsumerFinancial Protection Bureau (CFPB or Bureau) published a report titled Student Loan Borrowers Potentially At-Risk when Payment Suspension Ends. Delinquencies on other credit products since the start of the pandemic. New third-party collections during the pandemic. Multiple student loan servicers.

These include modernizing Treasury’s IT systems with an elevated cybersecurity threat focus, as well as ramping up partnerships with the financial and regulatory sectors. On October 31, the Financial Crimes Enforcement Network (FinCEN) informed U.S. On October 31, the Financial Crimes Enforcement Network (FinCEN) informed U.S.

million to consumers and pay a $500,000 civil penalty for deceiving consumers with false claims about their services. That information will be posted in a registry and open to the public, including to other consumerfinancial protection enforcers. For more information, click here. For more information, click here.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content