This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

This year, the challenges of managing delinquencies and navigating an uncertain economy will compound, making it imperative for companies to critically think about their strategy to collect from consumers in debt. What are we seeing in consumercredit trends today? Of course, one leading indicator is demand for credit.

We are entering a year of unknowns across the board, from potential regulatory changes to economic fluctuations to varying consumer sentiments, and theres a lot to consider as it relates to debt collection in 2025. Whats Impacting Consumers? What Does This Mean for Debt Collection?

Financialservices companies are using AI to assist with many business processes, including underwriting decisions, consumercredit approval, servicing and collections, loss mitigation programs, customer interaction on websites and mobile apps via chatbots, and in detecting fraud.

2020 was a transformative year for the consumerfinancialservices world. We hope you find this helpful as you navigate the evolving consumerfinancialservices landscape. Access full report here.

2021 was a transformative year for the consumerfinancialservices world. To access the report and view a message from ConsumerFinancialServices Practice Group Leader, Michael Lacy, and learn about our complementary webinar offerings, please click here. We hope this report brings you value.

We are pleased to share our annual review of regulatory and legal developments in the consumerfinancialservices industry. With active federal and state legislatures, consumerfinancialservices providers faced a challenging 2023. To download and share our report, please click here.

One revision now requires hospitals to complete a screening process to determine whether a particular patient is eligible for charity care before taking certain action, such as enrolling the patient in a payment plan or referring the account to in-house or third-party collections, on the patient’s account. For more information, click here.

On October 26, a House FinancialServices subcommittee drafted legislative proposals related to the buy now, pay later (BNPL) and earned wage access (EWA) market. On October 25, the CFPB released its biennial report to Congress on the consumercredit card market. financial institutions.

On July 27, the Financial Innovation and Technology for the 21st Century Act passed the House Committee on Agriculture. The bill previously passed the House Committee on FinancialServices on July 26. Per the report, examiners found multiple instances of unfair or abusive acts or practices by servicers.

District Court for the Western District of Texas, also stipulated that the DOE would destroy any information already collected and will follow notice-and-comment procedures for future data collection. toward the plaintiff’s litigation expenses and will publish a new Federal Register notice for proposed information collection.

On May 26, the CFPB issued a blog post regarding credit reporting disputes and requirements that furnishers must satisfy when handling a dispute. SF 2922 contains a work-from-home provision, allowing collection agency staff to continue working remotely. For more information, click here. For more information, click here.

The CFPB also found that while small institutions with overdraft programs charged lower fees on average, consumer outcomes were similar to those found at larger banks. The research notes that, despite a drop in fees collected, many of the fee practices persisted during the COVID-19 pandemic. For more information, click here.

The bill would amend Title 18 of the District of Columbia Official Code to allow, among other things, for the collection of personal property by affidavit. On October 7, Newsom approved SB 362, which will impose regulations on data brokers by allowing consumers to request the deletion of their personal data that was collected.

On October 25, the administrator of Colorado’s Uniform ConsumerCredit Code issued an order extending the requirements of sections (4) and (5) of SB-211 and restricting the use of extraordinary collection activities to collect debt or satisfy judgments in Colorado until February 1, 2021.

Federal Activities: On December 16, the ConsumerFinancial Protection Bureau (CFPB) issued a series of orders to five companies offering “buy now, pay later” (BNPL) credit. Department of Education’s decision to terminate its federal student loan contracts with private collection agencies. For more information, click here.

The defendants will be permanently banned from the merchant cash advance and debt collection industries, and they must pay $675,000 to settle FTC charges that they used deceptive and illegal means to seize assets from small businesses, nonprofits, and religious organizations. For more information, click here.

On December 29, 2021, the California Court of Appeals upheld a lower court ruling, prohibiting a company from collecting on $38 million of unpaid debt as consumers were not provided statutory notice of the risks of cosigning a consumercredit contract. For more information, click here.

On March 29, New York Attorney General Letitia James sent letters to the largest credit card companies and major debt collectors operating in New York, warning those companies of new state regulations that prevent them from suing consumers for old debts. All three affect debt collection in D.C.;

Bill Banning Social Media Debt Collection Passes N.Y. Kathy Hochul, that if signed, would prohibit the use of social media platforms to collect debts, for creditors or the collection agents working on their behalf. Consumers can also make their online profiles private and mask their connections with others.

Bill Banning Social Media Debt Collection Passes N.Y. Kathy Hochul, that if signed, would prohibit the use of social media platforms to collect debts, for creditors or the collection agents working on their behalf. Consumers can also make their online profiles private and mask their connections with others.

Finally, we will revisit the status of COVID-19-inspired state efforts to directly regulate credit reporting, and the impact on credit reporting of pandemic-inspired state regulation of debt collection. CFPB Policy Statements on Credit Reporting. Key topics to be discussed: The “CARES” Act. Amendment to the FCRA.

The New York legislature passed many new laws in 2022, some of which directly affect New York debt collection. We reported on many of these laws including: Cutting the statute of limitations in half to collect medical and consumer debt from six years to three years. Interested in learning more about debt collection in New York?

On Tuesday, January 9, New York Governor Kathy Hochul delivered the 2024 State of the State address, discussing certain changes that will affect debt collection within the state. Hochul made it clear that the state will assist consumers in New York by adding greater consumer protections—a plan that will affect creditors and debtors alike.

The Connecticut Banking Commissioner (Commissioner), acting through the ConsumerCredit Division of the Department of Banking (the Division), conducted an investigation into the Law Offices of David M. The firm allegedly collected about $81,000 of that amount. The firm had 14 days to request a hearing, but failed to do so.

With uncertainties about how the end of various pandemic-era benefits will impact consumers, it’s more important than ever for creditors and collectors to implement strategies that consider consumer situations and preferences when attempting to collect. What’s Impacting Consumers and the Industry?

Meeting Debt Collection Challenges Amid a Squeeze on Income. In order to deal with the rising cost of living and other challenges, anyone managing collections portfolios and effective debt recovery strategies needs these capabilities. As with most walks of life it also applies to effective debt collection. by Bruce Curry.

The trio examine why this is a big deal in consumer litigation, whether courts consistently apply recent Supreme Court decisions with one another, and what considerations and implications defendants should consider when deciding whether or not to remove a case from state to federal court.

On Tuesday, January 9, New York Governor Kathy Hochul delivered the 2024 State of the State address, discussing certain changes that will affect debt collection within the state. Hochul made it clear that the state will assist consumers in New York by adding greater consumer protections—a plan that will affect creditors and debtors alike.

which along with the Fair Debt Collection Practices Act, Telephone Consumer Protection Act, Section 5 of the Federal Trade Commission Act, and the Truth in Lending Act, forms the foundation of federal consumer rights law in the United States. . § 1681, et seq.), and throughout the world.

The Report, which covers April through September of 2019, is mandated by Dodd-Frank and was released in conjunction with Director Kraninger’s testimony to the House FinancialServices Committee. Credit Reporting is a Focus of the Bureau. Debt Collection Rule – Mum is the Word. Here are a few of our key take-aways.

CreditServices Association (CSA), the voice of the UK debt collection and purchase industry, has appointed Chris Leslie as chief executive with effect from 1 August 2020. Having been closely involved in financialservices policy over recent years, I? Credit is a crucial utility in today?s

On March 1, the ConsumerFinancial Protection Bureau (CFPB) released its “ Medical Debt Burden in the United States ” report, which questions whether consumercredit reports should include unpaid medical billing data. totaling $88 billion in medical bills in 2021. Work with other federal agencies, including the U.S.

On January 20, 2023, California Attorney General Rob Bonta submitted a letter to the CFPB agreeing with its preliminary determination that California’s Commercial Financing Disclosures Law (CFDL) is not preempted by TILA because the CFDL only applies to commercial financing and not to consumercredit transactions within the scope of TILA.

Government launches consultation on reform of ConsumerCredit Act. HM Treasury has issued a consultation seeking stakeholder views on reform of the ConsumerCredit Act 1974 (CCA). HM Treasury has issued a consultation seeking stakeholder views on reform of the ConsumerCredit Act 1974 (CCA).

Despite objections from CUNA and NAFCU, the House of Representatives passed the Comprehensive Debt Collection Improvement Act on Thursday. 2547 was sponsored by House FinancialServices Committee Chairwoman Rep. In the letter, Nussle stated, “Lenders rely on complete and accurate credit reports when underwriting loans.

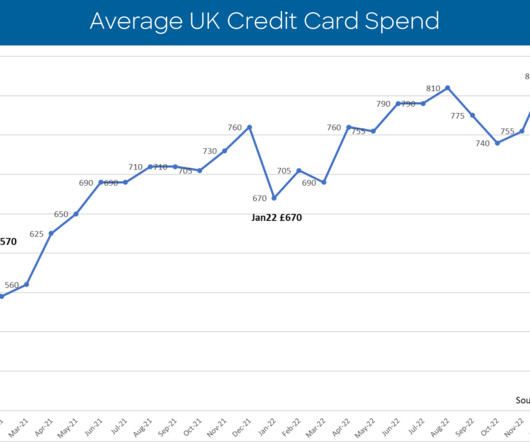

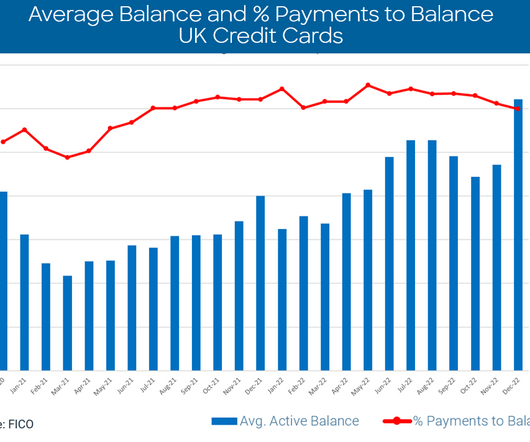

Highlights Average total sales per card down 8 percent compared to December 2022 at £755 Percentage of credit card accounts with two missed payments 13.6 percent higher than December 2022 Average balance on credit card accounts with two missed payments was 1.9 percent Average balances across all accounts dropped by 0.6

He has over 30 years’ experience working in senior roles across the technology, financialservices and publishing industries and has a passion for using technology and pioneering approaches to drive outstanding business growth and customer retention. Tomas Klinger, decision science and data director at Home Credit (previous winner).

With average consumer total spend at its highest and late payments rising significantly month-on-month and year-on-year, financial institutions will be particularly concerned as the focus on Consumer Duty heightens.

The Taskforce, comprised of five members, was established in January 2020 and was charged with examining the consumerfinancialservices environment and developing recommendations for improvement. Volume I of the report outlined the history and present landscape of a wide variety of consumer protection laws presently in place.

Flexibility to create tailored credit offerings With FICO® Score 10 T’s greater performance precision, lenders and investors have the flexibility to create tailored credit offerings. The updated model reflects the evolving credit landscape and credit behavior to help better inform a higher level of consumercredit risk prediction.

What’s more, unlike some fintech initiatives that assess risk based on cash flow data alone, the UltraFICO® Score presents the best of both worlds, combining cash flow data with traditional data from consumers’ credit files, along with the odds-to-score ratio that lenders understand.

Key issues highlighted in joint statement The dialogue aims to facilitate better policy coordination and exchange of insights and experience on a range of financialconsumer protection issues, some of which are outlined below.

Each and every one of those consumers chose to open a credit card account because of the safety, convenience and significant benefits that come with today’s credit cards,” said an American Bankers Association spokesperson after the blog post was published.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content