This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Consumer Financial Protection Bureau this morning announced the release of its final rule prohibiting the inclusion of medical debt on consumercredit reports. This rule is expected to remove $49 billion in medical debt from credit reports, impacting approximately 15 million consumers.

One of the most important reasons is that it allows them to obtain additional credit such as a mortgage or an automobile loan with much more ease. Having a bad credit rating can get in the way of a consumer’s life decisions. Maybe they’re paying a higher percentage for a new auto loan.

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York , leading to a shift in consumer spending for 2024. And we’re seeing consumers often need help to organize the different debts.”

With inflation proving more sticky than policymakers had hoped and uncertainty around how the new administrations policies might affect it, it may take longer for people to see lower interest rates on their mortgages, car loans and credit card balances, which could prove challenging to household budgets. Whats Impacting Consumers?

On November 17, the Consumer Financial Protection Bureau (CFPB) announced it is seeking public comment on its proposal to develop a new data set to better monitor the auto loan market. Because student loans are largely administered by the federal government, we know more about them too.

A collections notice shows up, a debt collector starts calling or you find a negative report on your credit history, but you know you paid the account in question. Can you sue a company for sending you to collections for money you didn’t owe? How Does the Law Protect Your Rights Regarding CreditCollections and Reporting?

“Amounts owed” comprises some 30% of the overall FICO® Score calculation and is heavily weighted towards credit card balances and utilization so the observed reduction in credit card debt is helping to drive scores upwards. Fewer consumers are actively seeking credit. There has been a 12.1% The Other Side of the Coin.

Today, you have six years to collect monies owed from consumercredit transactions. However, a bill approved by the New York Senate seeks to shorten the time to collectconsumercredit transactions to three years. Personal bank loans. Credit union loan. Credit cards.

If you have begun receiving calls from a company called Wilshire ConsumerCredit, you are probably feeling overwhelmed by their advances. They are a third-party debt collector and auto loan financer out of California. We can help you remove their collection account from your credit report. Ask Lex Law for Help.

When collecting a debt from you, collection agencies must adhere to federal and state rules. Fortunately, the federal Fair Debt Collection Practices Act (FDCPA) protects all states. You have rights to help you gain control over your debt collection interactions. Call or text you to collect a debt between 8 a.m.

Managing compliance and regulations in collections can be challenging for lenders in the UK. Stay tuned for insights that could make a significant difference in your approach to debt collection. They oversee debt collecting companies to ensure fair treatment of customers.

According to the research from Cornerstone Advisors , these point-of-sale short-term installment loans with low credit amounts have been increasing in popularity during recent years for retail purchases like clothing, household goods, electronics, and more.

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York, leading to a shift in consumer spending for 2024. And we’re seeing consumers often need help to organize the different debts.”

Bill Banning Social Media Debt Collection Passes N.Y. Kathy Hochul, that if signed, would prohibit the use of social media platforms to collect debts, for creditors or the collection agents working on their behalf. Consumers can also make their online profiles private and mask their connections with others.

Bill Banning Social Media Debt Collection Passes N.Y. Kathy Hochul, that if signed, would prohibit the use of social media platforms to collect debts, for creditors or the collection agents working on their behalf. Consumers can also make their online profiles private and mask their connections with others.

With uncertainties about how the end of various pandemic-era benefits will impact consumers, it’s more important than ever for creditors and collectors to implement strategies that consider consumer situations and preferences when attempting to collect. What’s Impacting Consumers and the Industry?

Judge Rules Debt Collection Lawsuit Waives Arbitration Clause A District Court judge in Maryland has denied a defendant’s motion to compel arbitration in a Fair Debt Collection Practices Act case, ruling that the defendant waived its right to arbitrate by engaging in prior litigation. More details here.

Are collections accounts weighing heavily on your credit report? While missing a payment on one of your accounts might seem like a minor offense, it can have major consequences on your credit. If you’ve fallen behind on any of your accounts, you could find Fairway Collections on your credit report.

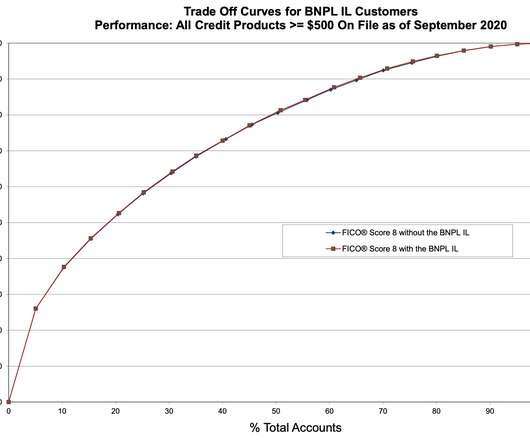

How Might Buy Now, Pay Later Loans Impact FICO® Scores? Key findings from FICO research on consumercredit files with recently opened Buy Now, Pay Later loans. consumercredit files. NicholetteLarsen@fico.com. Tue, 03/23/2021 - 22:16. by Suna Hafizogullari. expand_less Back To Top. Mon, 06/20/2022 - 15:00.

On September 29, the Consumer Financial Protection Bureau (CFPB or Bureau) released a special edition of its Supervisory Highlights , focusing on student loan servicing. It’s time to open up the books on institutional student lending to ensure all students with private student loans are not harmed by illegal practices.”.

Early in the COVID-19 pandemic, FICO data scientists discovered that the FICO® Resilience Index was a strong predictor of the likelihood that consumers were receiving loan accommodations such as payment deferrals and forbearances following implementation of the CARES Act. .

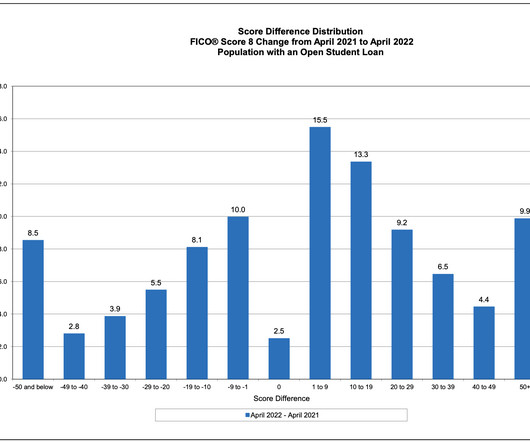

Home Blog FICO Are Student Loan Holders at Risk as Deferments Expire? Here we present results of our research into FICO® Score dynamics for holders of student loan debt between 2021 and 2022, to give an indication of key factors that seem to accompany large decreases in the FICO Scores of this population.

Read on for our take on what’s impacting consumer finances, how consumers are reacting and what else you should be considering as it relates to debt collection in 2024. What’s Impacting Consumers? trillion, according to the Federal Reserve Bank of New York’s latest Quarterly Report on Household Debt and Credit.

Why does the credit repair industry exist? As long as data is being collected for credit reports, there’s room for mistakes. They could be the difference in someone qualifying for different credit lines or not. So credit repair, consumercredit and credit bureaus—they’re all tied together.

And another factor might make the increases more painful for some consumers: The pause on federal student loan payments ended Sept. Student loan balances have already begun accruing interest again, and soon, borrowers will be expected to start making regular payments.

It marks the highest fine ever issued to a lender for what it deemed a breach of consumercredit rules. But more tellingly, the penalty related to the mistreatment of business and personal customers who fell behind on credit card and loan payments between 2014 and 2018 – well before many of us had even heard of COVID-19.

On Tuesday, January 9, New York Governor Kathy Hochul delivered the 2024 State of the State address, discussing certain changes that will affect debt collection within the state. Hochul made it clear that the state will assist consumers in New York by adding greater consumer protections—a plan that will affect creditors and debtors alike.

When you borrow money, whether through a revolving account, like credit cards , or an installment account, like an auto loan or student loan , the information is gathered by the credit bureaus. The data the bureaus keep in your credit files is the date used to calculate your credit scores.

22-(R22-011) , concluding earned wage access (EWA) products that are fully non-recourse and no-interest are not “consumer lender loans” under Arizona law. Thus, those who make, procure, or advertise EWA products are not required to be licensed as a “consumer lender” by Arizona’s Department of Insurance and Financial Institutions.

After New York Governor Andrew Cuomo signs the ConsumerCredit Fairness Act (S.153/Thomas) 153/Thomas) into law, many creditors will need to provide significant documentation in order to file a debt collection action against their non-paying consumers. The New Consumer Debt Collection Requirements.

It gathers credit reports from the three major credit bureaus and analyzes anonymous consumer data to generate a scoring model specific to each bureau. VantageScore, on the other hand, uses a combined set of consumercredit files, also obtained from the three major credit bureaus, to come up with a single formula.

The Consumer Financial Protection Bureau has issued a series of orders to five companies offering “buy now, pay later” credit. The orders to collect information on the risks and benefits of these fast-growing loans went to Affirm, Afterpay, Klarna, PayPal, and Zip.

Halloween is right around the corner, so we decided to round up something spectacularly scary: medical debt collection horror stories! This isn’t the first time we’ve featured examples of bad apples, but we wanted to focus on the medical debt collection industry in particular this time. Why is that?

Two entities that may send debt consolidation loan mailers are Symple Lending and Secure One Financial. What is a Pre-Screen Firm Offer of Credit? A Pre-Screen Firm Offer of Credit, often referred to as pre-approved credit, is a marketing strategy employed by creditors to identify potential customers for their financial products.

Across EMEA, most countries have now moved past the peaks of the COVID-19 driven lockdowns and restrictions, but the challenges of debt collection in the pandemic remain. There are other factors that will now further stress consumers, including the effect of sanctions from the current crisis in the Ukraine. .

Individuals, like you or I, have a credit history which determines our eligibility for home and car loans, ability to rent an apartment, obtain insurance, find a job and even maintain long-term romantic relationships. This doesn’t mean they have a bad credit history, because some of them may pay all their bills on time.

As the independent standard in credit scoring, FICO® Scores are the leading credit scores used extensively across the lending ecosystem ranging from originations, underwriting and account management to collections and asset-backed securitization. Ethan has a B.S. in management science/operations research from UC San Diego.

The next natural question is: how much of this data is available at the three nationwide credit bureaus? The answer is that while the availability of this data has been increasing, it remains far below other tradeline data such as credit cards, auto loans or mortgages.

improvements in predictive power enable FICO® Score 10 T to help mortgage lenders safely avoid unexpected credit risk and better control default rates, while making more loans to more consumers. . FICO Score 10 Suite Available from All Three Credit Bureaus.

They provide a service to you and then bill you, similar to a credit extension. The company, creditor or collection agency has legal ways to pursue payment. The judgment creditor can then use that court judgment to try to collect money from you. The ConsumerCredit Protection Act caps these types of garnishments.

In addition, the Symposium welcomes discussion over the recent decision by the Uniform Law Commission to address debt collection efforts by third-party debt collectors or buyers based on default judgments. Selected papers are due after the Symposium on June 4, 2021.

Saxon Shirley Fri, 05/20/2022 - 06:06 by FICO expand_less Back To Top Tue, 02/07/2023 - 19:10 As the independent standard in credit scoring, FICO® Scores are the leading credit scores used extensively across the lending ecosystem. million previously “unscorable” consumer files.

The insured creditor and its affiliates do not maintain an escrow account for consumercredit transactions secured by real property or a dwelling, other than: Escrow accounts established after consummation as an accommodation to distressed consumers to assist such consumers in avoiding default or foreclosure, or.

There are several key consumer laws that collectors should be concerned with when engaging in debt collection practices. These laws aim to protect consumers from unfair, deceptive, or abusive practices. Here are some important consumer laws that collectors should be familiar with: 1.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content