This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York , leading to a shift in consumer spending for 2024. If there’s one thing we’ve learned from our consumer interactions, including the 16.5

We are entering a year of unknowns across the board, from potential regulatory changes to economic fluctuations to varying consumer sentiments, and theres a lot to consider as it relates to debt collection in 2025. Whats Impacting Consumers? What Does This Mean for Debt Collection?

“Amounts owed” comprises some 30% of the overall FICO® Score calculation and is heavily weighted towards credit card balances and utilization so the observed reduction in credit card debt is helping to drive scores upwards. Fewer consumers are actively seeking credit. There has been a 12.1% The Other Side of the Coin.

Judge Rules Debt Collection Lawsuit Waives Arbitration Clause A District Court judge in Maryland has denied a defendant’s motion to compel arbitration in a Fair Debt Collection Practices Act case, ruling that the defendant waived its right to arbitrate by engaging in prior litigation. More details here.

Bottom line: households took on more debt at the end of last year and we’re seeing loans increasingly going bad, according to data from the Federal Reserve Bank of New York, leading to a shift in consumer spending for 2024. If there’s one thing we’ve learned from our consumer interactions, including the 16.5

BNPL loans are cited as a potential driver of greater financial inclusion, both in terms of consumer access to the BNPL loan themselves, as well as access to credit products that could enable unbanked and underbanked consumers to establish (or re-establish) their credit histories with one or more of the Consumer Reporting Agencies (CRAs). .

With uncertainties about how the end of various pandemic-era benefits will impact consumers, it’s more important than ever for creditors and collectors to implement strategies that consider consumer situations and preferences when attempting to collect. What’s Impacting Consumers and the Industry?

Add these all together and the financial outlook for consumers, especially those in debt, is scary. For one, the consumercredit market is looking strong with signs of expansion, specifically, originations for credit cards and personalloans are increasing. But there are silver linings, as well.

There are several key consumer laws that collectors should be concerned with when engaging in debt collection practices. These laws aim to protect consumers from unfair, deceptive, or abusive practices. Here are some important consumer laws that collectors should be familiar with: 1.

TransUnion ( NYSE: TRU ) confirmed that consumercredit activity keeps rising from the COVID-19 pandemic lows, but some areas like automobile loans (subprime) performance have lagged. Matt Komos , VP of Research and Consulting at TransUnion, stated: “On the surface, the consumercredit market is performing quite well.

The just recently released Federal Reserve ConsumerCredit-G.19 consumercredit outstanding has reached historic levels; outstanding consumercredit is now at $4.7 In August, consumercredit increased at a seasonally adjusted annual rate of 8.3 19 report shows that U.S. The post U.S.

FICO® Score 10 and 10 T provide a precise assessment of consumercredit risk on all credit product lines, including mortgages, auto loans, credit cards and personalloans.

As the independent standard in credit scoring, FICO® Scores are the leading credit scores used extensively across the lending ecosystem ranging from originations, underwriting and account management to collections and asset-backed securitization. Ethan has a B.S. in management science/operations research from UC San Diego.

In reality, its impact would extend far beyond payday lenders to the broader consumercredit market to cover affordable small dollar loans (including “accommodation” loans) that depository institutions are being encouraged to offer, credit cards, personalloans, and overdraft lines of credit,” the letter reads. “As

The automatic stay protects from most collection efforts. This goes beyond reasonable attempts to collect a debt and crosses the line into intimidation, abuse, or coercion. The Fair Debt Collection Practices Act (FDCPA) is a federal law in the United States that protects consumers from creditor harassment.

Credit card balances reached a record-setting $866 billion in the third quarter of last year, which represents a year-over-year increase of 19%. Credit balances reached a record-setting $866 billion in the third quarter of last year – and they are expected to keep climbing, the report from TransUnion said.

We found that FICO® Resilience Index continues to be a strong predictor of the presence of loan accommodations in place as of October 2020 – representing a mix of “long haul” accommodations by mortgage lenders and newer short-term accommodations allowed on bankcard, auto finance and personalloan accounts.

Information and data continue to be key tools at our disposal to better understand the dynamics of the last couple of years, and better navigate what lies ahead for the Canadian consumercredit environment. In this post, we have been citing trends and insights based on the latest FICO® Score for the Canadian market – FICO® Score 10.

A hike in the federal interest rate prompts a jump in the Bank Prime Loan Rate ( prime rate ), the credit rate that banks offer to their most credit-worthy customers and off of which they base other forms of consumercredit like mortgages and consumerloans. We all knew this was coming.

Credit Card, PersonalLoan Delinquencies Expected to Surge in 2023. The company’s 2023 ConsumerCredit Forecast released Wednesday projects serious credit card delinquencies will climb to 2.6% TransUnion said delinquency rates for those categories have not reached that level since 2010.

Still, consumercredit scores have remained high, helped by a strong labor market and cooling inflation, along with the removal of certain medical collections data from consumercredit files, recent reports show. The post Credit card balances spiked in the third quarter to a $1.08 trillion record.

How Might Buy Now, Pay Later Loans Impact FICO® Scores? Key findings from FICO research on consumercredit files with recently opened Buy Now, Pay Later loans. consumercredit files. But on the other hand, adding positive BNPL payment data in the consumercredit file could help the FICO® Score.

Fico XD helps young adults, immigrants, and those with past credit challenges that resulted in closing all credit accounts. In the last 30 years, the Fair Isaac and Company, better known as FICO, changed the way the lenders evaluate consumer applications.

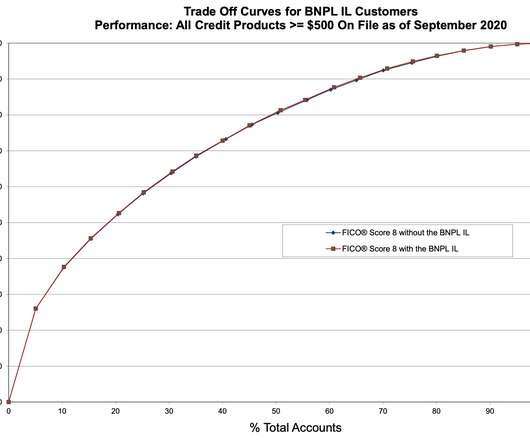

auto, mortgage, personalloan) and lifecycles (e.g., In other words, even as the relationship between odds of repayment and score has shifted, the score has retained its powerful ability to distinguish repayment likelihood between low and high scoring consumers. originations).

The DFPI is aggressively exercising its new authority to regulate a large group of newly covered financial services, including debt collectors, credit reporting and credit repair agencies, debt relief agencies and others.

Citi also offers personalloans, lines of credit, and mortgages, which can prompt a hard inquiry. If you are overwhelmed by dealing with negative entries on your credit report, we suggest you ask a professional credit repair company for help. File a Dispute with the Credit Bureaus. Collections-stage debt.

Citi also offers personalloans, lines of credit, and mortgages which can prompt a hard inquiry. If you are overwhelmed by dealing with negative entries on your credit report, we suggest you ask a professional credit repair company for help. File a Dispute with the Credit Bureaus. Collections-stage debt.

A collection account will lower your credit score and can generally stay on your credit report for up to seven years. Often, a collection entry will even keep you from getting a mortgage or securing an auto loan, which is why it’s important to do all you can to remove collections from your credit report quickly.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content