This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Bureaus new emphasis on tangible consumer harm, while deprioritizing areas such as medical debt and digital payments, signals a shift in enforcement priorities that may influence the regulatory landscape for many companies in the credit and collection industry.

As financialinstitutions continue to seek effective ways to communicate with consumers, text messaging (SMS) is emerging as a powerful tool to boost engagement, according to a published report. Financialinstitutions are increasingly using it as a way to build trust and create personalized consumer experiences.

The Consumer Financial Protection Bureau (CFPB)’s decision to establish supervisory powers over nonbank financialinstitutions will level the playing field and subject those companies to much-needed scrutiny, creditunion trade groups informed the agency Tuesday. Response From CreditUnion Trade Groups.

As per FTC, starting June 9, 2023 all collection agencies will be treated as financialinstitutions. This means all collection agencies must secure consumer data nearly the same way as banks. Failure to comply with GLBA can have severe consequences for the collection agency, especially the owners and/or the CEO.

We are entering a year of unknowns across the board, from potential regulatory changes to economic fluctuations to varying consumer sentiments, and theres a lot to consider as it relates to debt collection in 2025. What Does This Mean for Debt Collection? Whats Impacting Consumers? in December and the highest since May last year.

LUBBOCK, Texas (KCBD) – The grand opening for Capital Federal CreditUnion is scheduled to happen at 3 p.m. So the Lewises and a few others started a creditunion. Harper, chairman of the National CreditUnion Administration, which chartered the new creditunion. Source- site.

The first consideration that lenders (banks and creditunions alike) often face is when, and if, to conclude that the account owner does not intend to, or is not able to, clear the negative balance or loan deficiency. Charging Off” Uncollectable Debt. Ocwen Loan Servicing, LLC, 8:14-CV-3214-T-35MAP, 2015 WL 12938920, at *1 (M.D.

According to research from Equifax, the 2008 recession had an unexpected and interesting effect on creditunions. While market volume was down across the board in auto loan and bank card originations: Creditunions increased their market share by about 15% in auto loan origination. Pain points in prescreen marketing.

5 Ways CreditUnions Can Be More Resilient with AI and Analytics. Creditunions are sitting on a lot of risk right now. This COVID pandemic aftershock is about to hit the financial services industry, which means that creditunions need to pay close attention to their capital, asset quality, earnings, and liquidity.

For creditunions and smaller banks in North America, the challenge of how to compete with their bigger counterparts is a constant and pressing matter. Today’s prescreening solutions are very manual in nature, typically involving a list processing agreement with a credit bureau. Learn more about PrescreenCentral.

This filing comes just three days after CUNA and the National Association of Federally-Insured CreditUnions (NAFCU) sent a joint letter to the CFPB urging it to stay enforcement and implementation of the Final Rule for all covered financialinstitutions until after the U.S. CFPB (discussed here ).

Supreme Court’s final decision in Community Financial Services Association (CFSA) v CFPB. Given the effect of the [injunction order] on the overall distribution of compliance burdens across the financial sector, we ask that you consider broader relief.”

Tackling the Fintech Threat: A Guide for Banks and CreditUnions. What financialinstitutions need to compete with fintech threat disrupters. billion globally in 2021 – banks and creditunions are losing their status as the primary financial services providers to American consumers. by Darryl Knopp.

Where data has its own intrinsic value and where data breaches and cyberattacks are a risk for every business, the Safeguards Rule under the Gramm-Leach-Bliley Act (GLBA) provides financialinstitutions, including those in the accounts receivable management industry, with guidance on how to safeguard customer information.

04, 2024 — C&R Software (“C&R”),the world’s leading Cloud-native end-to-end software and solutions provider for the complete credit risk lifecycle and a CORA Group company, today announced the acquisition of SpringFour, the first-of-its-kind, leading financial health fintech. WARMINSTER, Pa.,

Banks and creditunions rarely see eye-to-eye, so it was no surprise when Dan Berger, president and CEO of the National Association of Federally-Insured CreditUnions, called out “greedy” bank executives responsible for recent bank failures. LONG BEACH, Calif.

University CreditUnion, September 08, 2022. 8, 2022 /PRNewswire/ — University CreditUnion (UCU) is excited to announce its newest partnership with UC San Diego. About University CreditUnion: University CreditUnion, a federally-insured financial cooperative, was founded in 1951 on UCLA’s campus by faculty and staff.

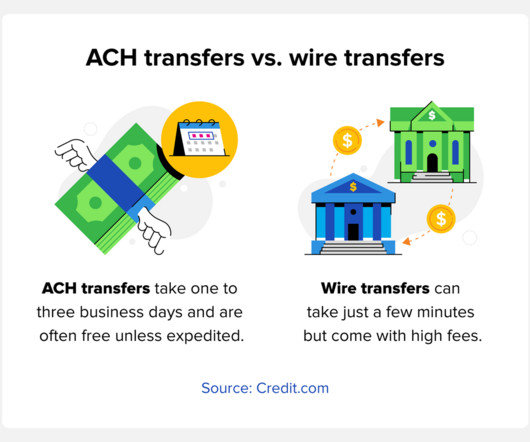

The backbone of these developments is none other than America’s Automated Clearing House (ACH) which facilitates seamless electronic transactions between banks and financialinstitutions within its network. Instant ACH transfers have gained prominence as they cater to the increasing demand for expedited financial transactions.

Businesses Exempt While the law covers most consumer agreements, some businesses are specifically exempt from this law, including: Services provided by a business under a franchise issued by a municipality or a city Any entity regulated by the Department of Financial Services (financialinstitutions, banks, creditunions, etc.)

Perhaps your own business is trying to struggle through collecting overdue payments and you are wondering if there is something more you can do. You have more important aspects of your business to run, but you may not know at what point it becomes worthwhile to bring in a collection professional. What does a collection attorney do?

On August 18, the American Financial Services Association, Consumer Bankers Association, CRE Finance Council, Equipment Leasing and Finance Association, Mortgage Bankers Association, National Association of Federally-Insured CreditUnions, Truck Renting and Leasing Association, and the U.S.

For creditunions and smaller banks in North America, the challenge of how to compete with their bigger counterparts is a constant and pressing matter. Today’s prescreening solutions are very manual in nature, typically involving a list processing agreement with a credit bureau. Learn more about PrescreenCentral.

15, 2022, the Federal FinancialInstitutions Examination Council’s (FFIEC) Task Force on Consumer Compliance adopted revised examination procedures for the Fair Debt Collection Practices Act (FDCPA) and its implementing regulation, Regulation F. A copy of the revised procedures can be accessed by clicking here. FFIEC is a U.S.

Five federal financialinstitution regulatory agencies in conjunction with the state bank and state creditunion regulators (collectively, agencies) are jointly issuing this statement to remind supervised institutions that U.S. dollar (USD) LIBOR panels will end on June 30, 2023.

Supreme Court’s final decision in Community Financial Services Association (CFSA) v. With this increased advocacy pressure now from all 50 state banking associations, it seems likely that the CFPB takes some action to “level the playing field,” either by issuing an amended regulation following public notice-and-comment, or otherwise.

Bankers are opposing any effort by the Consumer Financial Protection Bureau (CFPB or Bureau) to reduce or eliminate the late fee safe harbor, citing a potentially significant adverse impact on community banks and creditunions.

The Effective Date Fails to Consider the Impact on Small Issuers and Community FinancialInstitutions; Small issuers will have difficulty getting the attention of national networks and service providers and will be stuck at the back of the queue or cobbling together a patchwork of more regional, and potentially less reliable or scalable networks.

The Safeguards Rule requires nonbanking financialinstitutions to develop, implement, and maintain a comprehensive information security program to keep their customers’ information safe. In the letter, the SBA states: “[S]mall financialinstitutions will need to modify their methods for evaluating these.

The Recordkeeping Rule requires the collection and retention of information about payments or transmittal orders. Identity of the beneficiary’s financialinstitution. If the originator’s financialinstitution receives identifying information about the beneficiary from the originator, it must retain that information as well.

Financial services partners know that their clients are under increasing pressure to remain competitive, particularly when it comes to giving their end-customers the best experiences across the full lifecycle of engagement. It’s neither consistent nor comprehensive. Operational efficiency is poor. Case Study in Communications.

In letters dated August 1, the American Bankers Association , Consumer Bankers Association, CreditUnion National Association, and National Association of Federally?Insured Insured CreditUnions (Associations), as well as the Bank Policy Institute , expressed their collective displeasure with the idea.

A bank, creditunion, or other financialinstitution often approves the loan based on creditworthiness of the borrower, their credit history, and their perceived ability to repay. However, the lender may still put your account into collections and take legal action to recoup the debt.

A pooled model is a scoring model built on “pools” of historical data from many financialinstitutions. This makes them an ideal solution for banks and creditunions that don’t have enough data to create their own custom models but still want the flexibility to grow their portfolios responsibly. What Are the Options?

For banks, creditunions, and other lenders, the sudden shift to digital-only interactions has introduced a variety of internal and external challenges, as well as some opportunities. In fact, the main attrition driver for financialinstitutions is a poor banking app. Creating an AI Structure.

Now, let’s explore another example to see how pooled models can improve bad capture rates across home equity, installment, and revolving credit lines. Bad Capture CreditUnion: BEFORE. This creditunion wanted to increase their approval rates but not at the expense of increasing their overall risk.

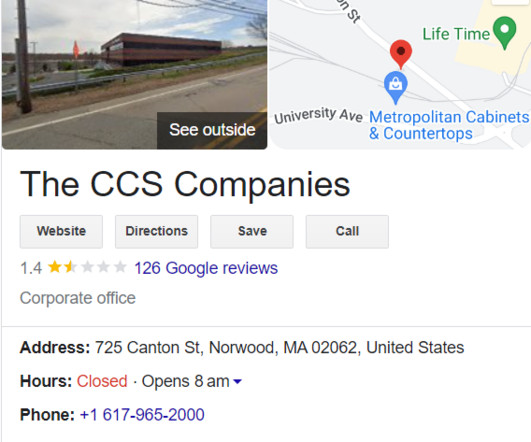

Dealing with debt collection agencies can be unpleasant, and CCS Offices are no different. It’s common for debt collectors to purchase and sell debts, resulting in the possibility of multiple collection accounts from the same debt appearing on your credit report. Who are CCS Offices?

Creditunion and banking trade groups sent a joint letter to CFPB Director Rohit Chopra on Thursday to ask for additional data collection, development and analysis before making new overdraft policy recommendations. Source- site. What occasions or needs typically prompt overdraft use.

Financialinstitutions should view this digital transformation surge as an opportunity to embrace intelligent technology that helps enable exceptional customer experiences and valuable outcomes. Financialinstitutions have access to a lot of data – from customers themselves, third-party organizations, meta data, and many other sources.

The first indicated that in 2019 alone, overdraft and other nonsufficient fund fees generated over $15 billion in revenue for consumer banks, with large banks (those with assets over $10 million), collecting three-quarters of the total revenue reported. 3] See Consumer Prot. 1, 2021), [link].

Depending on the bank or financialinstitution, there may be a fee for sending money to an account at a different bank using an ACH credit transfer. Can ACH Transfers Hurt My Credit Score? ACH transactions can’t hurt your credit score directly, but it is possible to acquire fees from your bank.

On October 24, the Federal Reserve Board (Fed), the Federal Deposit Insurance Corporation (FDIC), and the Office of the Comptroller of the Currency (OCC) (collectively, the agencies) finally issued their long-awaited final rule modernizing how they assess lenders’ compliance under the Community Reinvestment Act (CRA).

The bank-customer relationship is on very different footing than it was several years ago, and it requires a new way of thinking from financialinstitutions. These days, financialinstitutions are competing on much more than pricing and terms. The banks and creditunions that can be more human will flourish.

The Consumer Financial Protection Bureau (CFPB) has released a report detailing the fees and terms of banking products marketed to college students in partnership with their schools. The CFPB has released a report to Congress on college banking and credit card agreements. Department of Education. Key Takeaways.

The legislation would benefit banks and creditunions with assets under $15 billion. It requires federal regulators to exclude PPP loans from asset-size calculations for the purpose of determining capital ratios, deposit insurance premiums, and other asset thresholds at those financialinstitutions.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content