This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Consumer Financial Protection Bureau has officially signaled it plans to rewrite its small business lending data collection rule, known as Section 1071, following major leadership changes earlier this year.

The good news for lenders and debt collectors is that a reported 72% of consumers have a New Years resolution to pay off debt in 2025. CFPB Looks at Medical Debt, Student Loans and So Much Data Medical debt wasnt the only focus for the Consumer Financial Protection Bureau in Q4. Whats Impacting Consumers?

If you’re a creditor or collector working with financially distressed borrowers, considering consumer situations and preferences when attempting to collect and employing digital strategies to boost engagement are more important than ever. What’s Impacting Consumers and the Industry? NPAS, Inc., to establish a concrete injury.

When account owners have an account that reflects a negative balance, the lender is faced with a myriad of options and obligations with regard to the pursuit of that debt. Lenders that charge off a debt trigger issuance of the 1099-C when their defined policy leads the lender to discontinue collection activity and discharge a debt.

Banks are accelerating their adoption of new digital debt collection tools in anticipation of a “tidal wave of consumer debt issues” when government stimulus programs end and financialinstitutions stop offering forbearance and loan deferral options. About TrueAccord.

A trade group representing non-bank financialinstitutions that provide sales-based financing to businesses has filed a lawsuit against the Consumer Financial Protection Bureau claiming it has overstepped its authority by issuing a rule regulating how lenders must collect and submit data related to small business lending activities.

THE NEW ERA OF CONSUMER LENDING In today ’ s rapidly evolving financial landscape, the significant increase in consumer lending presents new challenges for financialinstitutions, particularly in managing collections.

The debt collections sector is facing several challenges, like many other sectors across Europe. Changing customer behavior due to the deterioration of their financial circumstances have led to an uptick in debt and collections activities as well. Control their cash collections and liquidity risk.

The debt collections sector is facing several challenges, like many other sectors across Europe. Changing customer behavior due to the deterioration of their financial circumstances have led to an uptick in debt and collections activities as well. Control their cash collections and liquidity risk.

The Supervisory Highlights detail issues identified by CFPB examination teams across a wide number of segments of the consumer financial services industry. Debt Collection. The CFPB alleges some financialinstitutions do not perform robust enough investigations of errors. Auto Servicing.

Customers are becoming more sophisticated and the same goes with the solutions they expect from financialinstitutions. Challenging the status quo for debt collection. Beyond doubt, the old-style debt collections approach has long been outdated. Customer analytics-driven approach for next-generation collections.

As result of FTC lawsuit, federal court issues temporary restraining order halting scheme that sent fictitious debt collection notices to consumers nationwide As a result of a Federal Trade Commission lawsuit, a federal court hastemporarily haltedthe operations and frozen the assets of a phantom debt collection scheme and its operators.

Collection accounts are bad for your credit score. These negative marks on your credit report indicate you might not pay your bills on time—or ever, which is why lenders don’t like to see them. Collection accounts can stay on your credit report for up to 7 years. What Are Collection Accounts?

Ohad Samet, CEO and cofounder of TrueAccord Group, has been named to the inaugural debt collection advisory committee of the California Department of Financial Protection and Innovation (DFPI). I look forward to working with this group representing diverse stakeholders in the debt collection industry,” said DFPI Commissioner Manuel P.

The UK’s Financial Conduct Authority (FCA) has handed out a £26m fine following poor treatment of more than 1.5 It marks the highest fine ever issued to a lender for what it deemed a breach of consumer credit rules. As we pass the first anniversary of the pandemic’s outbreak, where does this leave lenders?

Please join Troutman Pepper Partner Chris Willis and his colleagues Lori Sommerfield, Addison Morgan, and Josh McBeain for the first installment of a special three-part series about the Consumer Financial Protection Bureau’s (CFPB) new small business lending data collection and reporting final rule — the Section 1071 rule.

Let’s take a look at how the new updates to GLBA Safeguards Rule, how these security policies are important specifically for debt collection, and what best practices your business should follow to protect consumers’ data. Ready to collect more, faster from happier customers?

The Supervisory Highlights detail issues identified by CFPB examination teams across a wide number of segments of the consumer financial services industry. Debt Collection. The CFPB alleges some financialinstitutions do not perform robust enough investigations of errors. Auto Servicing.

In that context, lenders need to have access to state-of-the-art technology to avoid major losses. All those requirements can be addressed with ML, which has started to modernise the whole debt collections lifecycle. Debt collections have always implemented a reactive approach, by trying to gather losses after a customer defaulted.

While these loans may have seemingly inviting agreements, there are some terms that offer the credit card processor speedier debt collection relief against you. Worries from the credit card processor and/or their lender that they won’t be repaid. The loan is accelerated and the lender may avail themselves of extreme remedies.

As long as data is being collected for credit reports, there’s room for mistakes. While creditors weren’t looking up someone’s history of debt and payments, many lenders did take risk-mitigation actions. The agencies might also collect negative information from local newspapers. Why does the credit repair industry exist?

04, 2024 — C&R Software (“C&R”),the world’s leading Cloud-native end-to-end software and solutions provider for the complete credit risk lifecycle and a CORA Group company, today announced the acquisition of SpringFour, the first-of-its-kind, leading financial health fintech. WARMINSTER, Pa.,

What is a “self-serve portal” in financial services and collections? Overall, these self-service solutions represent a shift towards greater consumer control over their financial health, providing an efficient way for individuals to address and manage their finances—and debts specifically—on their own terms.

However, that doesn’t mean that this acceleration has been evenly distributed across every company in the financial services industry, nor across every part of an individual financialinstitution. How would you rate yourself when it comes to your collections transformation? Capturing RFD - “Reason for Deferral”.

12, 2019 — Katabat, a leading global supplier of debt management software solutions, has launched Easy Collect, a powerful, yet easy to deploy, mobile payment portal for lenders and debt collection agencies. Easy Collect is PCI-compliant and does not require IT support for deployment. WILMINGTON, Del.,

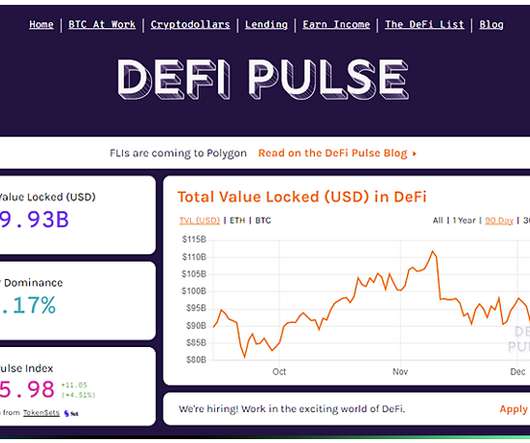

DeFi is a collective term for financial products and services that are accessible to anyone who can use Ethereum over the internet. A system that interacts buyers, sellers, borrowers, or lenders with peer-to-peer technology to access financial products or financial services bypassing middlemen such as financialinstitutions.

About TrueAccord Founded in 2013, TrueAccord’s data-driven debt collection platform is disrupting the collections industry by helping businesses collect more debt online than traditional methods. See all open positions and apply here: [link] .

Synthetic identity fraud is so dangerous because it tends to go undetected for long periods of time, as there is no individual who has had their identity stolen to realize what is happening and alert financialinstitutions. This post is the first in a series looking at the issues around both first-party and synthetic identity fraud.

Managing loan portfolios becomes a labyrinth for financialinstitutions in a financial ecosystem marked by unrelenting complexity and constant change. Consequently, financialinstitutions operate within an economy marked by contraction and sustained inflationary pressures.

On September 15, 2020, after considerable delay and pursuant to a court settlement, the Consumer Financial Protection Bureau (CFPB) released its Outline of Proposals Under Consideration and Alternatives Considered for small business lending data collection rulemaking. Implementing a period for financialinstitutions to comply.

Lenders face a myriad of challenges these days. A pooled model is a scoring model built on “pools” of historical data from many financialinstitutions. No data is required from the customer because it’s built on pools of historical data from other financialinstitutions. What Is a Pooled Model?

Incorrect Personal Information Lender Inquiries You Don’t Recognize Accounts You Never Opened Credit Utilization Goes Up Credit Score Goes Up or Down Unexpectedly Public Records You Don’t Recognize. Warning Sign 2: Lender Inquiries You Don’t Recognize. Warning Signs of Identity Theft. How Do I Check My Credit for Identity Theft?

Online lenders make it easy to compare rates and terms and find the right online personal loan for your situation. That is, the lender advances you money that you pay back with interest over a predetermined period of time. This often allows digital lenders to streamline the applications. Benefits of Online Personal Loans.

On April 18, the Consumer Financial Protection Bureau (CFPB or Bureau) published a blog post , scrutinizing the practice of withholding transcripts from students with delinquent accounts and who are attending an institute of higher education. As recently as December 2021, U.S.

22-(R22-011) , concluding earned wage access (EWA) products that are fully non-recourse and no-interest are not “consumer lender loans” under Arizona law. Thus, those who make, procure, or advertise EWA products are not required to be licensed as a “consumer lender” by Arizona’s Department of Insurance and FinancialInstitutions.

I am reporting a potentially fraudulent credit collection and reporting issue,” said a third. The firm, Capio Asset Servicing, came under investigation last year as part of Operation Corrupt Collector, an enforcement sweep of the debt-collection industry by federal and state officials. who represents debtors in collection cases.

Please join Troutman Pepper Partner Chris Willis and his colleagues Lori Sommerfield and Caleb Rosenberg for the second installment of a special three-part series about the Consumer Financial Protection Bureau’s (CFPB) new small business lending data collection and reporting final rule — the Section 1071 rule.

Origination is just the initial phase of the long and complex mortgage lifecycle, which begins with a lender qualifying a borrower and then providing the funds used to purchase a new property or refinance an existing property. The lender then holds the mortgage on its balance sheet or sells the mortgage on the secondary market to investors.

Digital collections tools and self-service platforms are on the rise and have empowered lenders to work more efficiently with their customers. Due to the limited agents' experience and financial literacy, customers usually don't get a proper explanation for the plans they are proposed to follow.

Perhaps your own business is trying to struggle through collecting overdue payments and you are wondering if there is something more you can do. You have more important aspects of your business to run, but you may not know at what point it becomes worthwhile to bring in a collection professional. What does a collection attorney do?

Meanwhile, the Consumer Financial Protection Bureau (CFPB) has been busy, with new rules impacting lenders and collectors across the spectrum. Read on for our take on what’s impacting consumer finances, how consumers are reacting and what else you should be considering as it relates to debt collection in 2024.

Customers are becoming more sophisticated and the same goes with the solutions they expect from financialinstitutions. Challenging the status quo for debt collection. Beyond doubt, the old-style debt collections approach has long been outdated. Customer analytics-driven approach for next-generation collections.

The Consumer Financial Protection Bureau (CFPB)’s decision to establish supervisory powers over nonbank financialinstitutions will level the playing field and subject those companies to much-needed scrutiny, credit union trade groups informed the agency Tuesday. Source: site. Background.

On October 24, the Federal Reserve Board (Fed), the Federal Deposit Insurance Corporation (FDIC), and the Office of the Comptroller of the Currency (OCC) (collectively, the agencies) finally issued their long-awaited final rule modernizing how they assess lenders’ compliance under the Community Reinvestment Act (CRA).

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content