This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

At the same time, however, the account owner/debtor is still responsible for the balance, and the lender/creditor can still make an effort to collect what is owed, with obvious exceptions being discharged or dischargeable bankruptcy filings. Collecting Debts After 1099-C Issuance. Charging Off” Uncollectable Debt. 1.6050P-1(b)(2)(i).

Two important statutes for all businesses to be aware of are the Florida Consumer Collection Practices Act (FCCPA) and the Fair Debt Collection Practices Act (FDCPA). Fair Debt Collection Practices Act. A person attempting to collect his or her “own” debt, is not a debt collector under the FDCPA. See Stanley v.

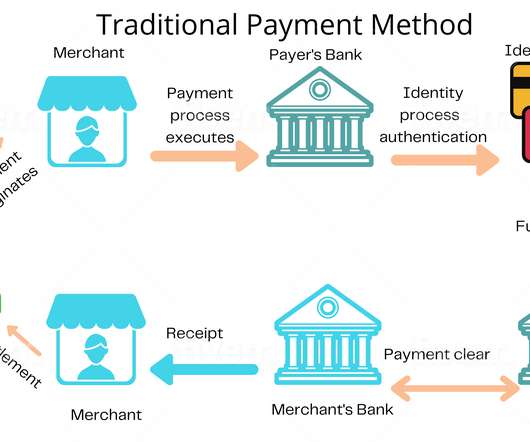

That is why a creditor must attempt to file a legal suit in which the debtor must declare all his assets under oath when asked by the judge. Debtors are legally bound to pay their liabilities like outstanding credit cards or unpaid bills etc. How do traditional payment methods work to collect payments?

The FTC filed lawsuits in September 2020 against National Landmark Logistics and Absolute FinancialServices, which operated under other names including National Landmark Service of United Recovery, Silverlake Landmark Recovery Group, Absolute FinancialServices Recovery, AFSR Global Logistics, and Tri-Star.

In late January, the Consumer Financial Protection Bureau (CFPB) released its 2022 “ List of Consumer Reporting Companies.” This list purports to give consumers “the details [they] need to take action” against companies that collect consumer information and prepare consumer reports.

In the press release announcing the issuance of the report, CFPB Director Rohit Chopra stated, “[t]uition payment plans offered by schools may look like a good option, but this report shows student borrowers can end up paying high fees, be forced to sign away their legalrights, or even have their transcript withheld by their school.”

The Florida Consumer Collection Practices Act (FCCPA) is a pro-consumer statute. Unlike the FDCPA, which only applies to debt collectors, the FCCPA applies to all persons or businesses collecting consumer debts. As such, all businesses need to be aware of the statute and the risk and potential liability associated with the statute.

In collecting consumer debts, no person shall: (9) Claim, attempt, or threaten to enforce a debt when such person knows that the debt is not legitimate, or assert the existence of some other legalright when such person knows that the right does not exist. Section 559.72(9) 9) , provides as follows: 559.72 Prohibited

Importantly, the Informational Statement also included a lengthy disclaimer which provided as follows: This statement is sent for informational purposes only and is not intended as an attempt to collect, assess, or recover a discharged debt from you, or as a demand for payment from any individual protected by the United States Bankruptcy Code.

The rules also establish a fairer process for borrowers to raise a defense to repayment, while preserving the borrowers’ day in court by preventing institutions of higher education (institutions) from forcing students to sign away their legalrights using mandatory arbitration agreements and class-action waivers.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content