This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Is it possible for an individual to sue a debt collector for violating the Fair Credit Reporting Act and Fair Debt Collection Practices Act for allegedly attempting to collect a debt that the individual believes he did not owe, when the individual took no action against the originalcreditor for placing the allegedly illegitimate debt … The post (..)

The judge determined that it followed its procedures for investigating disputes, which included contacting the originalcreditor to confirm the debts validity. The background: The plaintiff allegedly signed a housing agreement for an apartment while attending university. Learn more.

A Magistrate Court judge in New York has awarded the attorneys representing a plaintiff in a Fair Debt Collection Practices Act $11,297 in fees, after the plaintiff accepted an offer of judgment in the amount of $1,050 over a $59 debt that was owed to the originalcreditor.

A District Court judge in Illinois has granted a defendant’s motion for summary judgment in a Fair Debt Collection Practices Act case involving how the defendant, and the originalcreditor, came to be in possession of the plaintiff’s husband’s Social Security number.

More bankruptcies mean higher charge-offs for creditors and increased reliance on third-party collection agencies. With this uptick, regulatory scrutiny may rise, leading to more complaints and lawsuits under laws like the FDCPA (Fair Debt Collection Practices Act) and Regulation F due to errors in handling bankrupt debt.

If you ignore a debt collection agency, several potential consequences could affect your financial well-being and peace of mind: Persistent Contact : Debt collection agencies might persist in attempting to contact you through phone calls, letters, and possibly emails. This can be stressful and disruptive.

Judge Grants MTD in FDCPA Class Action Over Language in Letter A District Court judge in New Jersey has granted a defendant’s motion to dismiss a Fair Debt Collection Practices Act class-action lawsuit, but not on the merits as the defendant had sought. Read on to hear what the experts have to say this week. More details here.

million debt collection lawsuits were filed in 2022 alone. Failing to respond can result in default judgment, allowing the creditor to take action by seizing your assets or withholding your wages. If you find yourself being sued by a debt collector, you may wonder how to get a credit card lawsuit dismissed. An estimated 2.5

If you or someone you know has dealt with a collection agency, you know how trying it can be. Debt collection agencies have a long history of harassment and illegal practices. Can a collection agency report to a credit bureau without notifying you? It does not come into play for creditorscollecting their own debts.

The most common cases of zombie debt involve collection activities. Here’s one example of how a zombie might rise with help from a collection agency. The original lender or collection agency fails to collect within the statute of limitations. Zombie Debts and Judgments. You default on a debt.

District Court for the Southern District of California, granting summary judgment in favor of a debt collector in a Fair Debt Collections Practices Act (FDCPA) case. In doing so, it held that a collection letter, which indicated that the debtor could only dispute the underlying debt in writing, violated the FDCPA.

But it takes a lot to get to that scenario, so if you’re not there yet you still have time to learn how to protect yourself from this type of collections activity. In some cases, a spouse might have some legal protection against creditors seeking to collect money owned by their partner. Unfortunately, the answer is yes.

Can a debt collector collect after 10 years, for example? Can a debt collector collect after 10 years? Time-barred debts and your credit report What to do if you are contacted about an old debt COVID-19 and debt collections. Can a Debt Collector Collect After 10 Years? Find out in the informational guide below.

An Illinois federal district court recently denied a creditor-defendant’s motion for summary judgment in a Fair Credit Reporting Act (FCRA) case brought by a consumer who questioned why his debt was being reported twice — as both a tradeline with the originalcreditor and as a tradeline with a third-party collection agency.

When collecting a debt from you, collection agencies must adhere to federal and state rules. Fortunately, the federal Fair Debt Collection Practices Act (FDCPA) protects all states. You have rights to help you gain control over your debt collection interactions. Call or text you to collect a debt between 8 a.m.

July 22, 2021), the Eastern District of Michigan granted summary judgment in favor of a debt collector, holding that it did not violate the Fair Debt Collections Practices Act (FDCPA) by failing to report that the plaintiff disputed the debt at issue. to collect from plaintiff, Florence Burns (Burns).

Medical collections are a particularly difficult field - they demand tact, human dignity, and effective collection tactics all at the same time. Nearly half of all medical collection complaints filed with the CFPB in 2014 regarded continued attempts to collect a debt not owed.

A recent federal district court opinion highlights the potential pitfalls associated with renewals of unsatisfied default judgments. serves as a reminder that judgmentcreditors must still tread carefully when seeking to collect on, or revive, judgments from yesteryear. The case, Sarah Pitera v.

The Act amends provisions of New York’s Civil Practice Law and Rules, commonly referred to as the CPLR, and the Judiciary Law to require originalcreditors and third-party debt collectors to include certain information and documents when filing and prosecuting debt collection actions.

July 22, 2021), the Eastern District of Michigan granted summary judgment in favor of a debt collector, holding that it did not violate the Fair Debt Collections Practices Act (FDCPA) by failing to report that the plaintiff disputed the debt at issue. to collect from plaintiff, Florence Burns (Burns).

Court of Appeals for the Third Circuit recently held that a debt collector did not violate the federal Fair Debt Collection Practices Act (FDCPA) when it sent a consumer a collection letter inviting her to “eliminate further collection action” by calling the company, when in fact only written communication could legally stop collection activity.

15 provides the Private Student Loan Collections Reform Act, which is contained in Sections 1788.200 to 1788.211. Section 1788.205 provides that, in an action brought by a private education lender or private education loan collector to collect a private education loan, the complaint must allege specified information. Title 1.6C.15

Portfolio Recovery Associates, LLC, is a collection agency that buys old debts from lenders and companies that have been unable to collect the debt themselves. In other words, when the originalcreditor has been unsuccessful in collecting on a debt, it will write off the debt as a loss. Ask Lex Law for Help.

On January 11, the Consumer Financial Protection Bureau (CFPB) announced it reached a settlement with law firm Forster & Garbus, LLP in its lawsuit over alleged illegal debt collection practices. In doing so, the CFPB alleged (similar to its previous actions involving the law firms Frederick J.

It’s important to respond to any communications and document each step of the process when resolving your outstanding debt through a debt collection attorney. Because of their involvement in collecting money you owe a creditor, you may be contacted via a phone call or a letter from a debt collection attorney.

Whatever you’re dealing with, late payments, collections, charge-offs, or foreclosures, the following techniques can clean up your credit quickly. Collection). Write a letter to the originalcreditor or collection agency and ask them to remove the negative entry from your credit history as an act of goodwill.

The collection letter from the debt collector included a request for repayment of principal and interest. The defendant argued that it relied on information provided by the originalcreditor, based on which it should be entitled to the bona fide error (BFE) defense.

Key Takeaways: Zombie debt arises based on collection agencies. It may be possible to settle zombie debt with your originalcreditor. The Fair Debt Collection Practices Act (FDCPA) helps protect you from harassment. Collection activities are the most common causes of a zombie debt outbreak.

Is there a law in NYC that protects consumers and debtors from debt collecting agencies, businesses, and their attorneys? In this case, you should uphold your consumer rights to ensure ethical practices during the debt collection process. Consumers must be aware that the debt they are being collected for is valid.

The debt collector may select one of five reference dates as the itemization date: 1) the last statement date; 2) the charge-off date; 3) the last payment date; 4) the transaction date; or 5) the judgment date; and. The final rule follows a related final rule on debt collection practices issued by the CFPB in November 2020.

district judge in Arkansas recently granted the defendant McKendra Adams’s (Adams) motion to dismiss for lack of standing involving an alleged violation of the Fair Debt Collection Practices Act (FDCPA). Adams , a U.S. The case began when Cheatham defaulted on a car loan and surrendered the vehicle, which was sold at auction.

If you fall into hard times, the inability to pay off your credit card bills or student loans can result in your debts being transferred to a debt collection agency. In fact, they are a multifaceted company that can be a part of the debt collection process in the early stages (pre-charge of recovery) or the post-collection stage.

A debt collector is free to collect during the thirty-day period as long as it does not overshadow or contradict the consumer’s thirty-day rights. Whether easy or difficult, the Act mandates that the debt collector cease its collection efforts until the required information has been mailed to the consumer.

Keep in mind that a creditor writing off your unpaid debt as a loss doesn’t mean you don’t owe the debt. Your creditor may sell your charged-off debt to a collection agency for pennies on the dollar. The collection agency may then attempt to collect the debt anew.

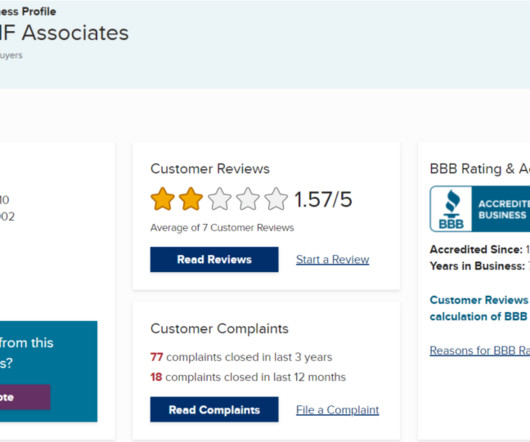

Like all other debt collectors, DNF Associates, LLC depends on multiple sources of information to pursue debt collection. They can request a default judgment from the court if they contact you and you fail to respond within 20 days. Typically, DNF Associates purchase these debts for as low as 10% of the original amount owed.

While many consumers are able to manage their debt load and stay current on their accounts, many businesses are finding themselves with uncollected debt and no proven collection strategy. Before you can collect on any debt, you need to validate the debt in accordance with the Fair Debt Collection Practices Act.

Enloe On December 18, 2020, the CFPB published the remainder of its Final Debt Collection Rule (the “Rule”) highlighting its crown jewel - the provisions centering around debt validation notices. of the Rule prohibits legal actions or threats of legal actions against a consumer to collect time-barred debts. By Caren D. Section 1006.2(c)

Sometimes, that debt gets out of hand and businesses find themselves on the receiving end of calls from commercial debt collection agencies. Here’s everything businesses need to know about commercial debt collection agencies and how to manage communication without disrupting day-to-day operations. How Long Can a Debt be Pursued?

In 2010, the defendant purchased the account and placed it with a law firm for collection. The trial court granted summary judgment to the defendant on all claims finding that because the defendant was not a consumer lender it was not required to obtain the license at issue.

Here’s some bedrock—debt collectors can call numbers supplied by the consumer to an originalcreditor as part of a credit transaction. Defendant moved for summary judgment and court granted. Either way, it never hurts to have a court decide that consent passed from a creditor to a debt collector. Back to Amadasun.

In Preston , the debt collector sent a collection letter that was inside of an envelope, which itself was inside another envelope. Creditor ID Claims—A Mixed Bag. Justice Barrett sat on two different panels that reviewed the issue of whether the debt collector sufficiently identified the creditor to whom the debt is owed. .”

The juxtaposition of Sections 1692e and 1692g continues to be a battle ground for the consumer bar and collection industry. Section 1692e prohibits false, deceptive or misleading representations in connection with the collection of a debt. In Powers v. Capital Mgmt Servs.,

Regulations around debt collection are strict, and experts from no cure no pay debt collection UK are here to help you navigate these waters. In this post, we will explore the rights and regulations governing debt collection in the UK. ” If you’re based in the UK, the answer may surprise you. or after 9 p.m.,

Section 1692g requires that within five days of the “initial communication with a consumer in connection with the collection of any debt” a collector must send the consumer a written notice containing, inter alia , the amount of the debt, and the name of the creditor to whom the debt is owed. See 15 U.S.C. 1692g(a)(1), (2).

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content