This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The Washington State Attorney General’s office has filed a lawsuit against a collection agency, accusing it of failing to comply with state law by not disclosing consumers’ rights regarding medical debt information.

One of the toughest jobs that companies in the credit and collection industry face these days is deciphering what a consumer means when he or she sends a communication indicating that there is a potential issue with the account. The defendant has not responded to the complaint to present its side of the case. ” Read the complaint.

Demand for payment failed, and now you want to go legal with your debt collection claim. Regardless of whether you proceed with mediation, arbitration, or litigation, your collection attorney will need to choose the appropriate legal theories or causes of action to include in your New York debt collection case.

Your credit score may improve if your collection debt is reported to a new credit scoring model—FICO 9®, FICO 10®, VantageScore 3.0® If you’ve gotten behind on payments to a creditor or lender, your debt could be sent to collections after around 120 days of missed payments. In This Piece: What Is Collections Debt?

adults with debt in collections, knowing their legalrights is crucial. The Fair Debt Collection Practices Act covers third-party debt collectors — those who buy a delinquent debt from an original creditor, like a credit card company. Working with third-party debt collectors can be confusing and scary.

At the same time, however, the account owner/debtor is still responsible for the balance, and the lender/creditor can still make an effort to collect what is owed, with obvious exceptions being discharged or dischargeable bankruptcy filings. Collecting Debts After 1099-C Issuance. Charging Off” Uncollectable Debt. 1.6050P-1(b)(2)(i).

Introduction: Managing debt is an essential aspect of running a business, and effective debt collection is crucial for maintaining healthy cash flow and financial stability. Implementing proper debt collection techniques can help businesses recover outstanding payments while maintaining positive relationships with clients.

Are you facing the challenge of collecting a business debt in Queensland? In this article, we have put together essential information on navigating the regulated environment of debt collection Queensland, from understanding your legalrights to enforcing debt recovery and choosing a reliable collection agency.

When collecting a debt from you, collection agencies must adhere to federal and state rules. Fortunately, the federal Fair Debt Collection Practices Act (FDCPA) protects all states. You have rights to help you gain control over your debt collection interactions. Call or text you to collect a debt between 8 a.m.

million debt collection lawsuits were filed in 2022 alone. This is why it is important to know your legalrights and how to mitigate the effects of being sued. By being proactive and understanding your rights and protections, you can reduce the long-term consequences of a credit card lawsuit. An estimated 2.5

Two important statutes for all businesses to be aware of are the Florida Consumer Collection Practices Act (FCCPA) and the Fair Debt Collection Practices Act (FDCPA). Fair Debt Collection Practices Act. A person attempting to collect his or her “own” debt, is not a debt collector under the FDCPA. See Stanley v.

Unless you are actually a debt collection expert like Debt Recoveries Australia , there is a good chance that you have quite a few higher priorities than managing your company’s accounts receivable. You might even delegate that task out to an assistant or employee without much thought to collect debts fast. CC the CEO or CFO.

Understanding the art of debt collection can be a challenging task for any business, especially when the debtor refuses to pay despite many reminders. In such situations, engaging a collections agency becomes inevitable. Access to Documentation: Ensure that your chosen collections agency has full access to these documents.

A court may issue a charging order following a CCJ against the debtor this judgement would confirm the debt is valid and there is a legalright to enforce it. One can consider a mortgage to be somewhat similar, in terms of its legal mechanism, in that there is a legal charge placed on a persons property.

Late payments can be a significant problem for any business, and when it comes to collecting unpaid invoices the situation can become difficult. It is important to know when the best time might be to escalate an invoice from your internal collection process and hand it over to professional debt collection services.

Dealing with a collection agency can often feel like navigating a maze, especially when there seems to be a change in your account’s open date. If you’ve found yourself in this situation, you’re likely asking, “Can a collection agency change an account’s open date?”

However, in case, your all efforts to collect the debt get unsuccessful, you can take the advantage of debt collection services. Whether it’s a new client or an old one, you have the right and obligation to collect the amount you are owed. Getting angry and using abusive language against them is not the right solution.

Navigating the convoluted terrain of debt collection can be a daunting task for businesses big and small. However, understanding the crucial steps in the debt collection process can empower businesses to retrieve owed money efficiently and legally, thus enhancing their financial health.

Not knowing whether to issue warnings, take legal action or try other methods for collecting unpaid rent can make the situation even more challenging. This blog post will provide an in-depth look at when and how you can send a non-paying tenant to collections. What Steps to Take Before Sending a Tenant to Collections?

Collecting debts from debtors having assets in Massachusetts while you are in another state or a different country used to be difficult, even if you had a judgment against them. Our Experienced Collections Attorneys Knows How to Enforce Foreign Judgments in Massachusetts. They afford the debt collection lawyer attachment targets.

Bankruptcy can also stop or delay a home or mortgage foreclosure, stop collection actions, stop garnishments and lawsuits. Debt collection agencies can be thoroughly unpleasant. The company does not tell you your legalrights or tell you about free options you can take on your own. What does each one mean?

In today’s volatile marketplace, the existence of a personal guarantee may provide the only viable basis for collecting outstanding receivables from a corporate obligor experiencing financial difficulty. A provision for the recovery of collection expenses and attorney’s fees should be inserted.

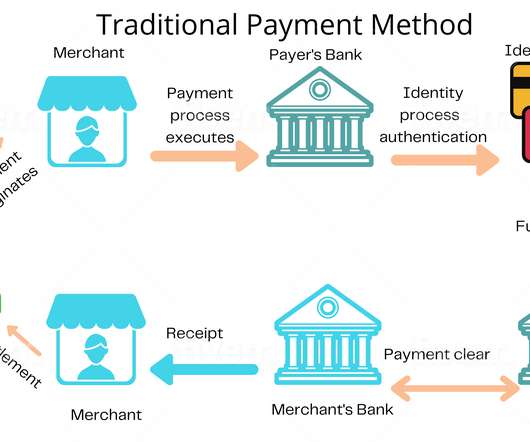

That is why a creditor must attempt to file a legal suit in which the debtor must declare all his assets under oath when asked by the judge. Debtors are legally bound to pay their liabilities like outstanding credit cards or unpaid bills etc. How do traditional payment methods work to collect payments?

When consumers returned the calls, the defendants falsely represented themselves as being from a mediation or law firm, threatened legal action, and used personal information to convince consumers that the threats were real. The FTC is sending checks to 1,625 consumers, who will receive $334.38

Even if the credit card company sides with you, the merchant may not—and they may try to collect. What happens when you dispute a charge Can a merchant try to collect Tips for avoiding future issues. Can a Merchant Try to Collect the Money from You After a Chargeback? In This Piece. What Happens When You Dispute a Charge.

The Florida Consumer Collection Practices Act (FCCPA) is a pro-consumer statute. Unlike the FDCPA, which only applies to debt collectors, the FCCPA applies to all persons or businesses collecting consumer debts. As such, all businesses need to be aware of the statute and the risk and potential liability associated with the statute.

This list purports to give consumers “the details [they] need to take action” against companies that collect consumer information and prepare consumer reports. In late January, the Consumer Financial Protection Bureau (CFPB) released its 2022 “ List of Consumer Reporting Companies.”

Columbia Debt Recovery , a Washington district court awarded each plaintiff $30,000 in emotional distress damages under the Fair Debt Collection Practices Act (FDCPA), $120 in treble actual damages under the Washington Collection Agency Act (WCAA) and the Washington Consumer Protection Act (WCPA), and $2,000 in statutory damages under the FDCPA.

From a legal perspective, the term “NIL” generally refers to an individual’s legalright to control the usage of their name, image, or likeness. Student athletes are also generally prohibited from receiving NIL compensation in exchange for attending a specific university.

In 2010, the defendant purchased the account and placed it with a law firm for collection. Instead, the offending conduct was misrepresenting “that it had the legalright to collect on the account when it lacked the proper license to do so.”

In the press release announcing the issuance of the report, CFPB Director Rohit Chopra stated, “[t]uition payment plans offered by schools may look like a good option, but this report shows student borrowers can end up paying high fees, be forced to sign away their legalrights, or even have their transcript withheld by their school.”

All too often, commercial debt collection becomes a negotiation. This could be more money, faster payments, avoiding court, or if necessary, the final outcome in court and the subsequent judgment collection process. One of the most common issues we see is no provision for the imposition of collection fees on the customer.

Last week, the CFPB issued a Consent Order against a New Jersey based debt-collection agency (Agency) over allegations that the Agency regularly violated the FDCPA and the CFPA in the course of their collection activity.

With an unprecedented number of Americans filing for unemployment, debt collection has been harder than ever for collectors who are attempting to work from home, and business isn’t going to get any better on account of those $1,200 stimulus checks, especially here in California. Money Collected Must Be Returned.

In collecting consumer debts, no person shall: (9) Claim, attempt, or threaten to enforce a debt when such person knows that the debt is not legitimate, or assert the existence of some other legalright when such person knows that the right does not exist. Section 559.72(9) 9) , provides as follows: 559.72 Prohibited

Even if the credit card company sides with you, the merchant may not—and they may try to collect the chargeback funds. The Truth in Lending Act is the federal law that gives consumers the legalright to dispute credit card charges if there is a billing error, as outlined in the Federal Reserve’s Consumer Compliance Outlook.

Because the borrower missed a payment, you are now indebted and liable to the bank for the loan amount plus interest as well as late charges, additional default interest at a pre-determined amount, and often bank attorneys’ fees or costs of collection. Being Pursued as the Guarantor.

While the underlying agreement or contract may seem straightforward, you need to do a thorough evaluation to make sure you aren’t waiving your legalrights by signing the contract. Have questions about defending a debt collection case? The post Are You Waiving Your Rights by Signing a Contract? Let us help.

If you are a victim of debt collector harassment, it’s important to know the debt collection laws, and consider your options for debt relief. Debt Collection Laws: What Can Debt Collectors Do? Debt collectors have a legalright to pursue the collection of personal debt within the bounds of the law.

If you don’t pay your credit card, it can lead to late fees, increased interest rates, being sent to collections, and damage to your credit. It could also result in legal action being taken against you. Collections A charge-off doesn’t make your debt magically disappear.

Quasi in rem: Quasi in rem judgments consider the legalrights of individuals and not necessarily all parties involved. Law enforcement may seize things like valuable collections or jewelry to be sold at auction. The judgment creditor can then use that court judgment to try to collect money from you. Property levies.

Importantly, the Informational Statement also included a lengthy disclaimer which provided as follows: This statement is sent for informational purposes only and is not intended as an attempt to collect, assess, or recover a discharged debt from you, or as a demand for payment from any individual protected by the United States Bankruptcy Code.

Evicting tenants in violation of the CDC, state, or local moratoria, or evicting or threatening to evict them without apprising them of their legalrights under such moratoria, may violate prohibitions against deceptive and unfair practices, including under the Fair Debt Collection Practices Act and the Federal Trade Commission Act.

In either case, you’re within your legalrights to seek validation for any inquiries on your report. Collections-stage debt. Dispute the Inquiry with ACRAnet and the Bureaus. Sometimes, reporting mix-ups can lead to credit inquiries. In other instances, identity fraud is to blame. Charge offs. Foreclosure.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content