This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

CRE Loans: The Next Time Bomb Nearly $1 trillion in CRE loans are due in 2025 alone. Creditors increasingly rely on court action for high-balance debts, but delays and debtor insolvency remain obstacles. Key Commercial Debt Statistics (20202025) $21.55 trillion in non-financial business debt by Q4 2024 (up 27% since 2019) $1.8

In an adversary proceeding, the collective owners of the Makaha Valley Country Club , golf courses, surrounding undeveloped land, and other related assets (the “Owners”) avoided obligations undertaken in connection with a loan extension provided by Tianjin Dinghui Hongjun Equity Investment Partnership (the “Lenders”).

[i] Section 1102 of the CARES Act allows parties to apply for loans under the Paycheck Protection Program (“PPP”), which may be forgiven under certain circumstances. [ii] xii] Pursuant to certain regulations, the Administrator excluded debtors in bankruptcy cases from the program.

As a result, loan borrowers with floating rates, also referred to as adjustable or variable rates, face higher monthly payments due to increased interest expenses. These exposures involve borrowers who have extended their loan terms and are now at risk of facing difficulties meeting their obligations.

An article titled “Avoiding Fraudulent Transfer Claims from Loan Workouts” written by Partner Hanna Lahr and Associate James Roberts was published in the Risk and Compliance section of the ABA Banking Journal.

The petition date is the date on which a debtor files a chapter 11 bankruptcy proceeding. The debtor is required to serve all known creditors with notice of the commencement of the chapter 11 case. In order to participate in the distribution of the debtor’s assets to satisfy pre-petition claims, a creditor must have a valid claim.

What’s worse—and which often comes as a big surprise—is when a business gets sued by the debtor or bankruptcy trustee seeking to recover payments made by the debtor before the bankruptcy. The SBRA created a new “subchapter V” to Chapter 11 of the Bankruptcy Code , which provides small business debtors an easier path through bankruptcy.

The decision vacates a 2021 Southern District of New York ruling, which held that the lenders were not on constructive notice of the mistake and could rely on the discharge-for-value doctrine to retain the funds. billion loan to Revlon, Inc., Citibank administered a $1.8 funded by a group of lenders.

ii] Consequently, the designation of a debtor as a SARE may have significant ramifications in a case. million constructionloan from Evertrust Bank (“Evertrust”) to build a hotel. [v] v] Because Evertrust refused to fund $4 million on the loan, The Source Hotel halted construction. [vi]

If you’re owed money by a bankrupt debtor, you likely have to file a claim. A creditor must take care to ensure that the claim amount listed on the debtor’s schedules is accurate and the claim is scheduled against the right debtor (in cases involving more than one debtor entity). Do You Have to File a Claim? Walton, Jr.’s

In evaluating the Texas Business & Commerce Code and title 11 of the United States Code (the “Bankruptcy Code”), the United States Bankruptcy Court for the Southern District of Texas, in In Re Burts Construction, Inc., In 2017, Allegiance Bank loaned Burts Construction, Inc. the “Debtor”) $1.5 1] In re Burts Constr.,

Persistent Contact: Debt collectors may contact debtors through phone calls, emails, letters, or even personal visits. Consider a Payment Plan: Many debt collectors are open to negotiating payment plans that are manageable for the debtor. Over time, these can accumulate, significantly increasing the total amount owed.

(“Acis LP”) is a Delaware limited partnership investment adviser and collateralized loan obligation (“CLO”) manager. [4] 5] Acis was named as an alleged debtor in an involuntary petition for relief under chapter 11 of the Bankruptcy Code. [6] 4] Highland Capital Management L.P. 24]. Gandy ( In re Gandy), 299 F.3d

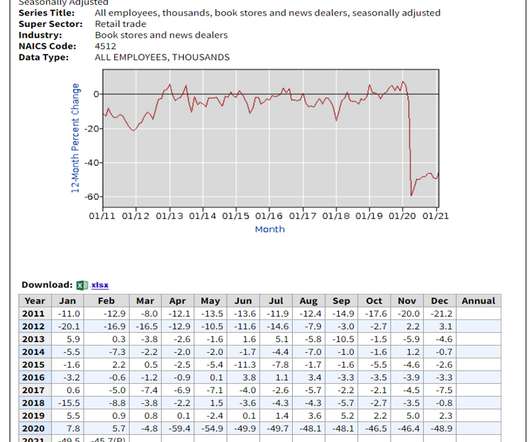

Even industries that were doing well, such as commercial construction, transportation, biopharmaceutical research and development, found themselves forced to completely overhaul their operations at an unprecedented cost. drop from 2019. Source: US Bureau of Labor Statistics. They are, by no means, exceptions.

Financial institutions, servicers, lenders, and debt collectors must stay up-to-date on evolving federal and state laws stemming from the COVID-19 pandemic, as such laws impact all facets of consumer loan servicing and debt collection. In March of 2020, Burr published an article discussing the global pandemic’s impact on collection practices.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. For more information, click here. On May 13, the U.S. 248, which limits a collection agency’s ability to collect on medical debt.

LLC ), the United States Court of Appeals for the Ninth Circuit found that thepresumption that a debtor has the requisite mens rea the intent to defraud his creditorswas properly inferred from the mere fact that he operated a business entity that met the objective elements of a Ponzi scheme. [1] Rund ( In re Epd Inv. 1] Jerrold S.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content