This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Senate Bill 5480, introduced in the 69th Legislature, aims to void and make unenforceable any medical debt that is reported to a consumercredit reporting agency or creditbureau.

Senate Bill 5480, introduced in the 69th Legislature, aims to void and make unenforceable any medical debt that is reported to a consumercredit reporting agency or creditbureau. More details here.

For example, in the US, 92 percent of consumers have cell phones, but just 5 percent of consumers have telco data reported in their traditional creditbureau files. Figure 1: Creditbureau coverage is greater for some types of data than others. FICO has a solution to this problem. market. .

Plus, FICO Score 10 T utilizes a consistent odds-to-score relationship as the prior FICO Score version used by the Enterprises, offering continuity and stability for lenders, investors and consumers. FICO® Score 10 T incorporates trended creditbureau data. FICO Score 10 Suite Available from All Three CreditBureaus.

Some of those laws also cover your rights as a consumer to fair debt collection practices. A few of the laws that might come into play are as follows: The Fair Credit Report Act ensures your right to an accurate consumercredit profile. It obligates companies to report truthful information on your credit report.

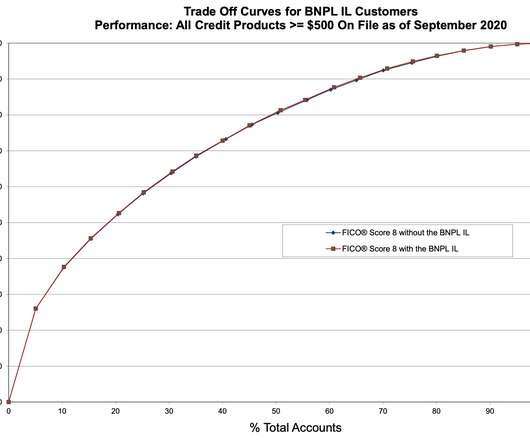

BNPL loans are cited as a potential driver of greater financial inclusion, both in terms of consumer access to the BNPL loan themselves, as well as access to credit products that could enable unbanked and underbanked consumers to establish (or re-establish) their credit histories with one or more of the Consumer Reporting Agencies (CRAs). .

All three for-profit credit reporting agencies, Experian, Equifax and Transunion compile and report consumercredit and debt payment activity and sell this consumer information to lenders seeking to grant credit. Here’s why: Who Decides Your Credit Score? Key Takeaways. Final Thoughts.

and globally -- making access to credit more efficient and objective, which has continued into the present day. FICO® Scores are dynamic and evolve as changes in consumer behavior are reflected in the underlying creditbureau data housed and managed by the three primary U.S. consumer reporting agencies (CRAs).

For example, in the US, 92 percent of consumers have cell phones, but just 5 percent of consumers have telco data reported in their traditional creditbureau files. Figure 1: Creditbureau coverage is greater for some types of data than others. FICO has a solution to this problem. market. .

FICO® Score At 716, Indicating Improvement In ConsumerCredit Behaviors Despite Pandemic. Ethan Dornhelm wrote: The FICO® Score is the lingua franca, or common language, for the credit scoring industry. It serves as a broad-based, independent standard measure of credit risk. Fewer consumers are actively seeking credit.

consumer data not present in the traditional creditbureau files) to enhance the predictiveness and inclusiveness in credit scoring. This is especially critical for the approximately 50 million consumers in the U.S. More than 200 million U.S.

Providing inaccurate information to a creditbureau. Failing to report both the favorable and unfavorable payment history of the borrower to a national consumercreditbureau at least annually if the student loan servicer regularly reports such information.

You could also: Put together a realistic debt-repayment plan Increase your income with a better-paying job, or ask your boss for a raise Ask your lenders for a lower interest rate Consider consumercredit counseling Concentrate on one debt at a time to avoid feeling overwhelmed. >> Download our free budget template to get started.

Allowing consumers to demonstrate their regular rent payments will provide a proven indicator of positive financial behavior and will be a useful complement to the FICO ® Score in mortgage lending. There are 53 million consumers who don’t have sufficient data in the traditional creditbureau files to generate a credit score today.

Find out more about free credit repair for low-income families and individuals below. Educating Yourself on ConsumerCredit Sites When it comes to free credit repair and report help, consumercredit sites are a great resource. Disputing them in writing with the creditbureau.

To further enhance flexibility and predictive power, the addition of FICO® Score 10 T incorporates trended creditbureau data. These in-depth insights can help lenders expertly manage credit risk in these uncertain times, while continuing to make competitive credit offers to consumers. .

Rent Bureau , now owned by the creditbureau Experian, electronically compiles rental data from property management companies and individual landlords. Rental agencies and alternative credit providers use the data to screen applicants and establish consumercredit scores.

In fact, while other credit scoring models may generate a credit score based on stale credit information , our minimum scoring criteria requires that at least one credit account has updated information reported in the last six months. How frequently the data is updated depends on where it resides: CreditBureau Data.

One of the primary goals of VantageScore is to provide a model that is used the same way by all three creditbureaus. That would limit some of the disparity between your three major credit scores. So, what are the differences between an Experian credit score calculated using VantageScore and one calculated via the FICO model?

Renting a home, apartment or town house can affect your credit in a number of ways. It’s increasingly common for credit reporting agencies to include positive rental history in consumercredit reports. Having good credit can help you rent an apartment, and paying rent on time can help you build good credit.

On March 23, the CFPB released two reports, New Data on the Characteristics of Mortgage Borrowers During the COVID-19 Pandemic and Emergency Savings and Financial Security : Insights from the Making Ends Meet Survey and ConsumerCredit Panel.

Information and data continue to be key tools at our disposal to better understand the dynamics of the last couple of years, and better navigate what lies ahead for the Canadian consumercredit environment. Comparing Canadian creditbureau data between April 2021 to April 2020, we saw a notable decrease in missed payments.

And that’s because it generally takes a few months for the effects of that event and the accompanying financial strain to start to show up in consumers’ credit reports, such as in the form of rising balances, credit seeking behavior, and eventually for some, missed payments. consumers decreased on a year-over-year basis.

Saxon Shirley Fri, 05/20/2022 - 06:06 by FICO expand_less Back To Top Tue, 02/07/2023 - 19:10 As the independent standard in credit scoring, FICO® Scores are the leading credit scores used extensively across the lending ecosystem. million previously “unscorable” consumer files. Read the full post 3.

And while some of our clients’ business lines benefit from the very latest innovations, others such as mortgage continue to find that older versions of the FICO® Score – even some that were first developed decades ago – meet their needs for credit risk assessment. We also recognize that our scores serve many different purposes.

However, there are other institutions that uses the acronym CBNA on credit reports. Here are some other establishments that CBNA could stand for: CreditBureau of North America: The CreditBureau of North America is a collection agency that collects unpaid debts on behalf of third-party companies. Conclusion.

Today’s prescreening solutions are very manual in nature, typically involving a list processing agreement with a creditbureau. The solution integrates Equifax ConsumerCredit Information and FICO risk decision management technology with marketing campaign automation and execution.

Today’s prescreening solutions are very manual in nature, typically involving a list processing agreement with a creditbureau. The solution integrates Equifax ConsumerCredit Information and FICO risk decision management technology with marketing campaign automation and execution.

Over the past several years, we’ve helped lenders develop on-ramps to mainstream credit using alternative data for those seeking financial inclusion. Our research finds that alternative data sources that demonstrate a consumer’s ability to manage their finances are predictive of consumercredit risk.

Key findings from FICO research on consumercredit files with recently opened Buy Now, Pay Later loans. market: BNPL reporting approach: How a BNPL lender reports these accounts to a creditbureau can materially influence the impact these loans ultimately have on the FICO® Score. consumercredit files.

Personal loans and credit card debt reached record levels in 2022 due to financial pressures brought on by high inflation and climbing interest rates, according to third-quarter data from a consumercredit reporting agency.

If you’re among them, be sure to dispute the misinformation with the creditbureau in question (here’s how). Your credit score will likely thank you for it. Open a New Account.

The CFPB said it was concerned about accumulating debt, regulatory arbitrage and data harvesting in a consumercredit market already quickly changing with technology, as GOBaningRates previously reported.

Despite these industry trends, yesterday’s report using data from the CFPB’s Making Ends Meet survey and creditbureau data from the ConsumerCredit Panel found that more than a quarter (26.5%) of consumers reside in households that were charged an overdraft or NSF fee in the past year.

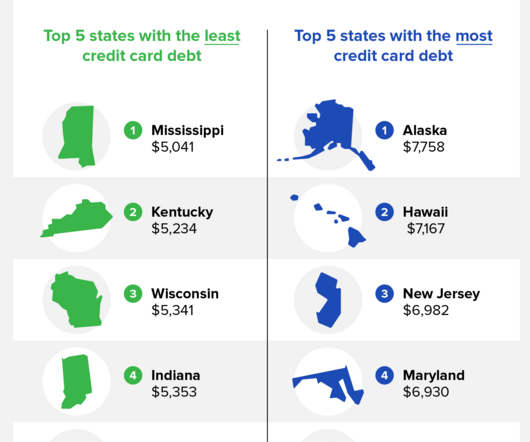

Here are the standout findings of various debt statistics: The average American household has over $9,000 in credit card debt. WalletHub ) Mississippi has the least credit card debt at $5,259 per person. Credit Karma ) Alaska has the most credit card debt on average at $8,139. Virginia $7,174 6. Connecticut $7,032 7.

A Pre-Screen Firm Offer of Credit, often referred to as pre-approved credit, is a marketing strategy employed by creditors to identify potential customers for their financial products. This process involves a preliminary screening of consumercredit reports to determine if individuals meet specific criteria set by the lender.

5 percent decrease, and some states were able to continue keeping their debt low, according to Credit Karma’s report. This will not only help you compare your own credit card balance to the national average, but you’ll also see if you’re getting a good deal with your current cards. How many credit cards carry a balance?

According to the Federal Reserve’s ConsumerCredit report, 43.5 Not only can you not declare bankruptcy on many forms of student loan debt, but it can also harm your credit. The creditbureau Experian® shows the average student loan balance increased 91 percent between 2009 and 2022. As of September 2022, the U.S.

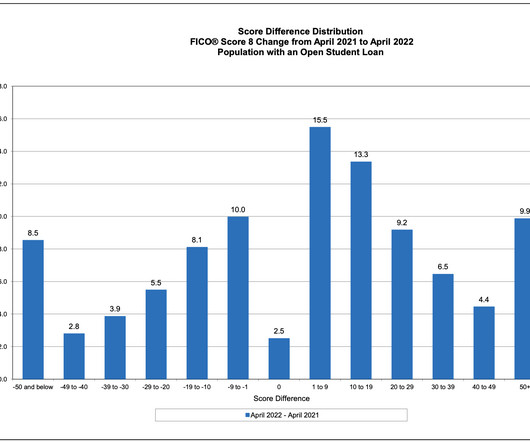

Our analysis looked at depersonalized consumercredit reports from a nationally representative creditbureau sample of consumers who had one or more open student loans as of April 2021 and we observed their credit score change as of April 2022.

In our top post, Vice President and General Manager of Scores, Sally Taylor explained the new FICO Resilience Index, designed to provide lenders with a more precise assessment of consumercredit risk and consumers with demonstrated talent for weathering economic storms greater access to credit.

From there, you should file a dispute with the creditbureau(s). The Fair Credit Reporting Act requires bureaus to handle disputes with a 30-day investigation. They’re pros at getting inaccurate hard inquires removed from consumercredit reports.

Among other things, the bill prohibits student loan servicers from: (1) directly or indirectly employing any scheme, device, or artifice to defraud or mislead student loan borrowers; (2) engaging in any unfair or deceptive practice toward any person or misrepresent or omit any material information involving the servicing of a student education loan, (..)

RentGrow On Your Credit Report. RentGrow is an agency that obtains consumercredit reports for landlords. Both RentGrow and the creditbureaus should help you get the inaccurate entry off your report. Hard credit inquiries can impact any one of your credit scores, or all three of them.

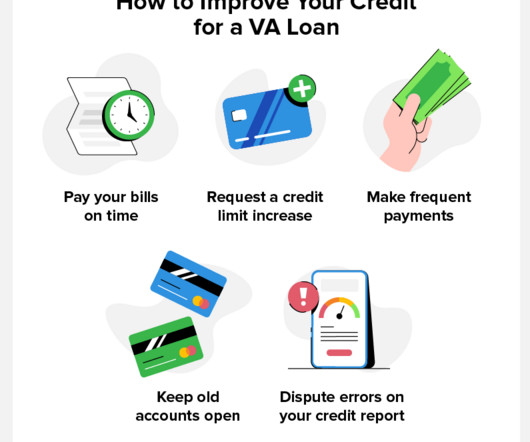

Dispute errors on your credit report: Get a copy of your credit report and check for inaccurate information. If you find an error, file a dispute with the relevant creditbureau. By checking your credit score, you can gauge your chances of getting approved for a VA loan.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content