This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For example, in the US, 92 percent of consumers have cell phones, but just 5 percent of consumers have telco data reported in their traditional creditbureau files. Figure 1: Creditbureau coverage is greater for some types of data than others. FICO has a solution to this problem.

Score 10 T gives mortgage lenders the flexibility and predictive power to make more precise lending decisions. It is FICO’s most powerful score to-date and gives mortgage lenders unparalleled flexibility and predictive power while preserving the trusted and proven FICO Score minimum scoring criteria. FICO Admin. by James Wehmann.

Some of those laws also cover your rights as a consumer to fair debt collection practices. A few of the laws that might come into play are as follows: The Fair Credit Report Act ensures your right to an accurate consumercredit profile. It obligates companies to report truthful information on your credit report.

As BNPL loans become a more commonplace form of credit used by consumers, these loans could also become an important factor in consumercredit reports, and by extension, in the FICO ® Scores based on those credit reports. Our Initial Insights from the First FICO-Conducted BNPL Research Study.

and globally -- making access to credit more efficient and objective, which has continued into the present day. FICO® Scores are dynamic and evolve as changes in consumer behavior are reflected in the underlying creditbureau data housed and managed by the three primary U.S. consumer reporting agencies (CRAs).

Rent, home payments, utilities such as gas, water, electric, and even things like cable or other on-time payment history can be used by creditbureaus to create a reliable credit score from which they can underwrite credit. What lenders use alternative credit data to grant credit?

All three for-profit credit reporting agencies, Experian, Equifax and Transunion compile and report consumercredit and debt payment activity and sell this consumer information to lenders seeking to grant credit. Here’s why: Who Decides Your Credit Score? Key Takeaways. Final Thoughts.

For example, in the US, 92 percent of consumers have cell phones, but just 5 percent of consumers have telco data reported in their traditional creditbureau files. Figure 1: Creditbureau coverage is greater for some types of data than others. FICO has a solution to this problem.

FICO® Score At 716, Indicating Improvement In ConsumerCredit Behaviors Despite Pandemic. Ethan Dornhelm wrote: The FICO® Score is the lingua franca, or common language, for the credit scoring industry. It serves as a broad-based, independent standard measure of credit risk. Fewer consumers are actively seeking credit.

Find out more about free credit repair for low-income families and individuals below. As of early 2023, you could still get your free credit report once a week with each of the bureaus, though this option may end at any time. Request the report in writing after being denied credit. Get your credit score via your lender.

The FICO® Score 10 Suite outperforms all previous FICO Scores, giving lenders unparalleled predictive power to make more precise lending decisions. With the FICO® Score 10 Suite, lenders gain up to a ten percent predictive lift over previous FICO Score models.

Then, avoid putting any more money on credit cards until you’ve paid off most of the consolidation loan. . First, call all your lenders and tell them what’s going on. According to creditbureau Experian’s 2019 ConsumerCredit Review , we are accumulating debt at an average of 3% per year.

consumer data not present in the traditional creditbureau files) to enhance the predictiveness and inclusiveness in credit scoring. This is especially critical for the approximately 50 million consumers in the U.S. More than 200 million U.S.

Allowing consumers to demonstrate their regular rent payments will provide a proven indicator of positive financial behavior and will be a useful complement to the FICO ® Score in mortgage lending. There are 53 million consumers who don’t have sufficient data in the traditional creditbureau files to generate a credit score today.

One of the primary goals of VantageScore is to provide a model that is used the same way by all three creditbureaus. That would limit some of the disparity between your three major credit scores. So, what are the differences between an Experian credit score calculated using VantageScore and one calculated via the FICO model?

While the FICO® Score has been trusted by consumers, lenders and investors for decades, the data that goes into a FICO® Score can be as recent as a payment reported by your lender today. . How frequently the data is updated depends on where it resides: CreditBureau Data. How current is the data in my FICO Score?

That’s why FICO has been focused on finding new ways to demonstrate responsible financial behavior so that lenders can confidently extend credit to more consumers. . Over the past several years, we’ve helped lenders develop on-ramps to mainstream credit using alternative data for those seeking financial inclusion.

And while some of our clients’ business lines benefit from the very latest innovations, others such as mortgage continue to find that older versions of the FICO® Score – even some that were first developed decades ago – meet their needs for credit risk assessment. We also recognize that our scores serve many different purposes.

The FICO Blog posts last year reflected that – we wrote about everything from the impact on collections, proactive lender communications with consumers, issues with fraud, and of course, how FICO® Scores were impacted. We hope that what readers learned helped instill confidence in keeping credit flowing during uncertain times.

And that’s because it generally takes a few months for the effects of that event and the accompanying financial strain to start to show up in consumers’ credit reports, such as in the form of rising balances, credit seeking behavior, and eventually for some, missed payments. consumers decreased on a year-over-year basis.

Saxon Shirley Fri, 05/20/2022 - 06:06 by FICO expand_less Back To Top Tue, 02/07/2023 - 19:10 As the independent standard in credit scoring, FICO® Scores are the leading credit scores used extensively across the lending ecosystem. million previously “unscorable” consumer files. Read the full post 3.

Information and data continue to be key tools at our disposal to better understand the dynamics of the last couple of years, and better navigate what lies ahead for the Canadian consumercredit environment. Comparing Canadian creditbureau data between April 2021 to April 2020, we saw a notable decrease in missed payments.

“ Pre-Screen Firm Offer of Credit ” might sound like jargon, but understanding its implications is crucial for anyone navigating the realm of credit and debt consolidation. What is a Pre-Screen Firm Offer of Credit? These criteria could include factors like credit score, income level, and debt-to-income ratio.

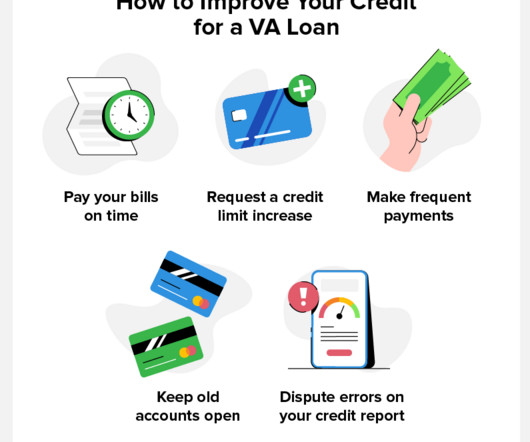

While there is no minimum requirement, most lenders prefer a credit score of 620 or above. While VA loans are typically easier to get approval for than conventional loans, private lenders still have certain requirements you must meet. One of these requirements is typically a good credit score.

The CFPB said it was concerned about accumulating debt, regulatory arbitrage and data harvesting in a consumercredit market already quickly changing with technology, as GOBaningRates previously reported. CNBC explains that multiple transactions made with different BNPL loans appear as different tradelines on your credit report.

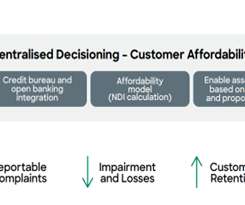

It is one of the biggest challenges lenders face over the next few years. Lenders could no longer base decisions simply on a customer’s history of repaying. Lenders have refined and improved their affordability models over the years in adherence to regulatory requirements. Affordability is top of mind.

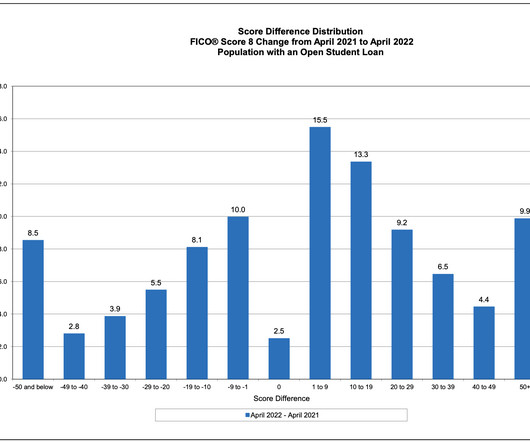

Our analysis looked at depersonalized consumercredit reports from a nationally representative creditbureau sample of consumers who had one or more open student loans as of April 2021 and we observed their credit score change as of April 2022.

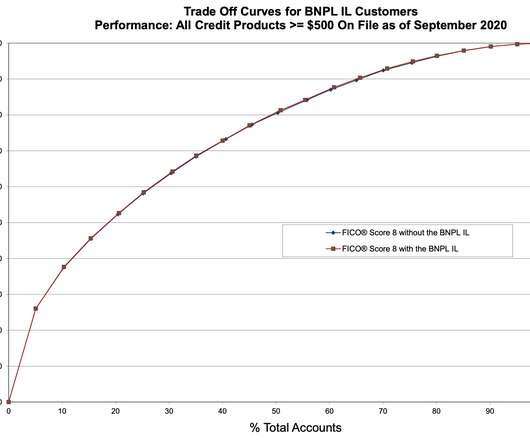

Key findings from FICO research on consumercredit files with recently opened Buy Now, Pay Later loans. market: BNPL reporting approach: How a BNPL lender reports these accounts to a creditbureau can materially influence the impact these loans ultimately have on the FICO® Score. consumercredit files.

RentGrow On Your Credit Report. RentGrow is an agency that obtains consumercredit reports for landlords. These inquiries don’t do any damage to your score and don’t get added to your credit report. A word of caution: While one credit inquiry is nothing to fret over, try not to stack up too many. Hard Inquiries.

If you are overwhelmed by dealing with negative entries on your credit report, we suggest you ask a professional credit repair company for help. How Does a Macys DSNB Hard Inquiry Affect Your Credit Report? Any time you apply for new credit, like a card, loan, or line of credit, the lender might run a hard credit check.

The proposed rule would require lenders to assess a borrower’s ability to repay a PACE loan and would provide a framework for how these loans will be treated under the Truth in Lending Act. PACE loans, secured by a property tax lien on the borrower’s home, are often promoted as a way to finance clean energy improvements, such as solar panels.

Both of these factors are considered somewhat invisible to the typical creditbureau. Four UK tier 1 lenders have announced an expected £20.2 Can you protect consumers’ credit ratings during a crisis to enable access to credit? Over the same period, we have seen a significant growth in BNPL borrowing.

Developed by FICO in partnership with LexisNexis Risk Solutions and Equifax, this innovative score utilizes alternative data—data not included in the traditional creditbureau file. The inclusion of this alternative data leads to a more reliable estimate of consumercredit risk and helps score more than 26.5

Then kindly ask the debt collector to remove collections from your credit report out of goodwill. With some newer scoring models of FICO and VantageScore, they ignore a collection marked as “paid”, though many lenders still utilize older formulas that will still weigh a paid collection account against you.

Since you are more of a participant in the process, you’ll have a better understanding of your individual situation when you reach out to a credit repair company. A good credit repair agency should start out by determining exactly which items they can help you with. What can credit repair companies not do? This isn’t true.

The three major credit bureausTransUnion, Equifax and Experiankeep records regarding peoples credit history. Find out more about what information a creditbureau might have on file for you, how they get it, and how you can see it below. In This Piece What Are the Three CreditBureaus?

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content