This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

million Americans have student loan debt, which totals over $1.7 If you owe tens of thousands of dollars in student loan debt, you’re not alone. According to the Federal Reserve’s ConsumerCredit report, 43.5 million Americans have some form of federal or private student loan debt. 2021 37 10.2 Source: U.S.

The answer is that while the availability of this data has been increasing, it remains far below other tradeline data such as credit cards, auto loans or mortgages. For example, in the US, 92 percent of consumers have cell phones, but just 5 percent of consumers have telco data reported in their traditional creditbureau files.

According to the research from Cornerstone Advisors , these point-of-sale short-term installment loans with low credit amounts have been increasing in popularity during recent years for retail purchases like clothing, household goods, electronics, and more.

On June 14, Nevada Governor Joe Lombardo signed into law AB 332 , An Act Relating to Student Education Loans, requiring, among other things, student loan servicers to be licensed by the Commissioner of Financial Institutions and regulating certain conduct of the servicers towards borrowers. The law will take effect on January 1, 2024.

Plus, FICO Score 10 T utilizes a consistent odds-to-score relationship as the prior FICO Score version used by the Enterprises, offering continuity and stability for lenders, investors and consumers. FICO® Score 10 T incorporates trended creditbureau data. FICO Score 10 Suite Available from All Three CreditBureaus.

Some of those laws also cover your rights as a consumer to fair debt collection practices. A few of the laws that might come into play are as follows: The Fair Credit Report Act ensures your right to an accurate consumercredit profile. It obligates companies to report truthful information on your credit report.

If you want to lose the plastic altogether, think about applying for a debt consolidation loan. Go for a loan with a low interest. Then, avoid putting any more money on credit cards until you’ve paid off most of the consolidation loan. . Compare Rates on Debt Consolidation Loans. Check Your Credit Score.

and globally -- making access to credit more efficient and objective, which has continued into the present day. FICO® Scores are dynamic and evolve as changes in consumer behavior are reflected in the underlying creditbureau data housed and managed by the three primary U.S. consumer reporting agencies (CRAs).

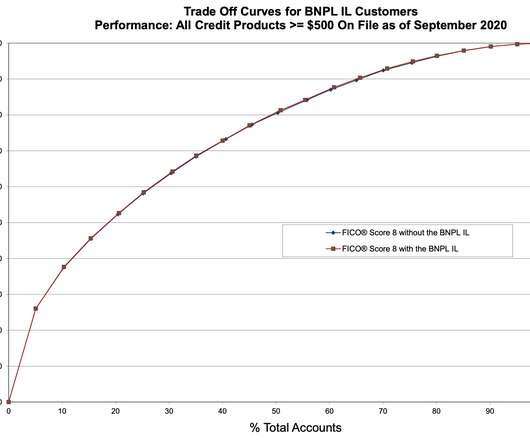

How Might Buy Now, Pay Later Loans Impact FICO® Scores? Key findings from FICO research on consumercredit files with recently opened Buy Now, Pay Later loans. consumercredit files. NicholetteLarsen@fico.com. Tue, 03/23/2021 - 22:16. by Suna Hafizogullari. expand_less Back To Top. Mon, 06/20/2022 - 15:00.

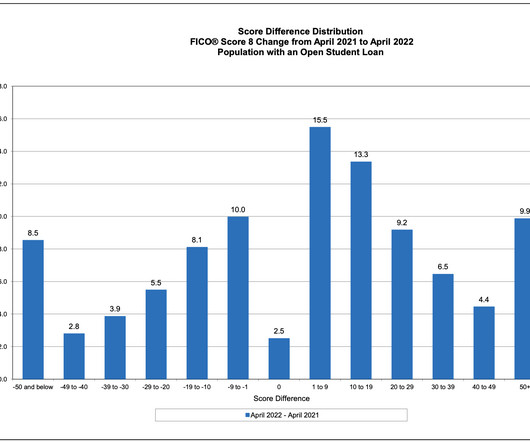

Home Blog FICO Are Student Loan Holders at Risk as Deferments Expire? Here we present results of our research into FICO® Score dynamics for holders of student loan debt between 2021 and 2022, to give an indication of key factors that seem to accompany large decreases in the FICO Scores of this population.

All three for-profit credit reporting agencies, Experian, Equifax and Transunion compile and report consumercredit and debt payment activity and sell this consumer information to lenders seeking to grant credit. Here’s why: Who Decides Your Credit Score? Amounts owed in relation to credit limits.

While there is no minimum requirement, most lenders prefer a credit score of 620 or above. A VA home loan is a mortgage backed by the Department of Veterans Affairs (VA) for service members, veterans, and their families. The purpose of VA loans is to help veterans purchase homes with lower interest rates and better terms.

The answer is that while the availability of this data has been increasing, it remains far below other tradeline data such as credit cards, auto loans or mortgages. For example, in the US, 92 percent of consumers have cell phones, but just 5 percent of consumers have telco data reported in their traditional creditbureau files.

One of the primary goals of VantageScore is to provide a model that is used the same way by all three creditbureaus. That would limit some of the disparity between your three major credit scores. So, what are the differences between an Experian credit score calculated using VantageScore and one calculated via the FICO model?

Alternative credit sources that do not report to the creditbureaus can include payments for rent, utilities, service accounts, and personal loans. Rent Bureau , now owned by the creditbureau Experian, electronically compiles rental data from property management companies and individual landlords.

Two entities that may send debt consolidation loan mailers are Symple Lending and Secure One Financial. What is a Pre-Screen Firm Offer of Credit? A Pre-Screen Firm Offer of Credit, often referred to as pre-approved credit, is a marketing strategy employed by creditors to identify potential customers for their financial products.

FICO® Score At 716, Indicating Improvement In ConsumerCredit Behaviors Despite Pandemic. Ethan Dornhelm wrote: The FICO® Score is the lingua franca, or common language, for the credit scoring industry. It serves as a broad-based, independent standard measure of credit risk. Fewer consumers are actively seeking credit.

To further enhance flexibility and predictive power, the addition of FICO® Score 10 T incorporates trended creditbureau data. These in-depth insights can help lenders expertly manage credit risk in these uncertain times, while continuing to make competitive credit offers to consumers. .

While the FICO® Score has been trusted by consumers, lenders and investors for decades, the data that goes into a FICO® Score can be as recent as a payment reported by your lender today. . How frequently the data is updated depends on where it resides: CreditBureau Data. are billed on a monthly cycle. Alternative Data.

Saxon Shirley Fri, 05/20/2022 - 06:06 by FICO expand_less Back To Top Tue, 02/07/2023 - 19:10 As the independent standard in credit scoring, FICO® Scores are the leading credit scores used extensively across the lending ecosystem. million previously “unscorable” consumer files.

Your credit history and scores can impact your entire life. Whether or not you can get a loan—and at what interest—often depends on your credit. Credit can also play a role in whether you can rent the apartment you want, get a credit card for use in daily life or enjoy a great deal on car insurance.

On March 23, the CFPB released two reports, New Data on the Characteristics of Mortgage Borrowers During the COVID-19 Pandemic and Emergency Savings and Financial Security : Insights from the Making Ends Meet Survey and ConsumerCredit Panel. The report also found that single borrower loans were approximately 1.6

Credit Risk and FICO Score Trends? And that’s because it generally takes a few months for the effects of that event and the accompanying financial strain to start to show up in consumers’ credit reports, such as in the form of rising balances, credit seeking behavior, and eventually for some, missed payments.

Renting a home, apartment or town house can affect your credit in a number of ways. It’s increasingly common for credit reporting agencies to include positive rental history in consumercredit reports. Having good credit can help you rent an apartment, and paying rent on time can help you build good credit.

Sure, credit-scoring models are complicated (all that algorithm-ing and such). But, when you get right down to it, the secret sauce to building good credit is actually pretty straightforward: Take a whole bunch of on-time loan payments, keep a pinch of debt, stir in some new accounts, and let the thing bake.

Information and data continue to be key tools at our disposal to better understand the dynamics of the last couple of years, and better navigate what lies ahead for the Canadian consumercredit environment. Comparing Canadian creditbureau data between April 2021 to April 2020, we saw a notable decrease in missed payments.

In our top post, Vice President and General Manager of Scores, Sally Taylor explained the new FICO Resilience Index, designed to provide lenders with a more precise assessment of consumercredit risk and consumers with demonstrated talent for weathering economic storms greater access to credit.

While these are not reported on credit reports yet, they are still loans. The CFPB said it was concerned about accumulating debt, regulatory arbitrage and data harvesting in a consumercredit market already quickly changing with technology, as GOBaningRates previously reported.

However, there are other institutions that uses the acronym CBNA on credit reports. Here are some other establishments that CBNA could stand for: CreditBureau of North America: The CreditBureau of North America is a collection agency that collects unpaid debts on behalf of third-party companies. Conclusion.

Credit card balances reached a record-setting $866 billion in the third quarter of last year, which represents a year-over-year increase of 19%. Credit balances reached a record-setting $866 billion in the third quarter of last year – and they are expected to keep climbing, the report from TransUnion said.

On May 1, the CFPB proposed a rule to implement a congressional mandate to establish consumer protections for residential property assessed clean energy (PACE) loans. PACE loans, secured by a property tax lien on the borrower’s home, are often promoted as a way to finance clean energy improvements, such as solar panels.

Over the past several years, we’ve helped lenders develop on-ramps to mainstream credit using alternative data for those seeking financial inclusion. Our research finds that alternative data sources that demonstrate a consumer’s ability to manage their finances are predictive of consumercredit risk.

If you are overwhelmed by dealing with negative entries on your credit report, we suggest you ask a professional credit repair company for help. How Does a Macys DSNB Hard Inquiry Affect Your Credit Report? Any time you apply for new credit, like a card, loan, or line of credit, the lender might run a hard credit check.

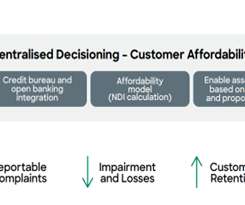

Triggered in part by the US housing market collapse and an unprecedented number of loan defaults, the crisis uncovered a shocking level of unrestrained lending and excessive risk taking. But a crucial challenge to existing affordability assessments has been the huge spike in ‘buy now, pay later’ loans (BNPL).

RentGrow On Your Credit Report. RentGrow is an agency that obtains consumercredit reports for landlords. Soft inquiries can be prompted by: Credit score check. Pre-qualification for a loan or credit card. These inquiries don’t do any damage to your score and don’t get added to your credit report.

Both of these factors are considered somewhat invisible to the typical creditbureau. billion increase on impaired loans. We expect an increased need for digital-led payment plans and a higher demand for loan modification, so the longer-term financial impacts can be worked through.

We break this down in our article: “ What Exactly is Credit Repair & How it Works,” but the short answer is that credit repair is the process of reviewing, disputing, and negotiating negative items on your credit report that may negatively impact the credit risk tier you’re in and the loans and interest rates you qualify for.

A collection account will lower your credit score and can generally stay on your credit report for up to seven years. Often, a collection entry will even keep you from getting a mortgage or securing an auto loan, which is why it’s important to do all you can to remove collections from your credit report quickly.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content