This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The South Carolina Department of Consumer Affairs weighed in on the matter, arguing that a consumercreditcarddebt is subject to the SCCPC and that the collector was required to provide a right to cure notice before suing to recover the debt.

Gordon of the District Court for the District of Nevada ruled that the defendant, a debt collection law firm, lacked the necessary minimum contacts with Nevada to establish personal jurisdiction. The background: The case stemmed from a consumercreditcarddebt judgment originally obtained in Tennessee by a creditor.

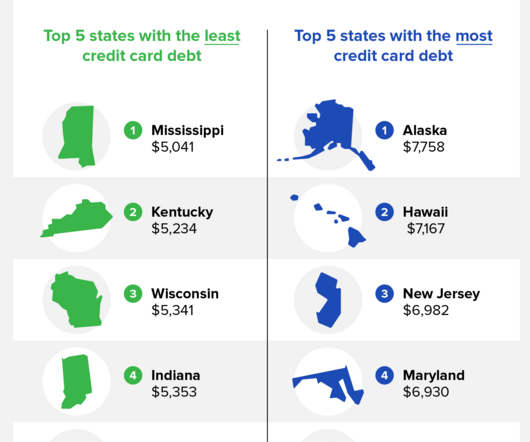

The average household creditcarddebt in America is $9,654, and the states with the largest amount of creditcarddebt are Alaska, Hawaii, and New Jersey. Between the first quarters of 2022 and 2023, The Federal Reserve Bank of New York reported that the creditcarddebt in America rose by $145 billion.

The average household creditcarddebt in America is $9,260, and the states with the largest amount of creditcarddebt are Alaska, Hawaii, and New Jersey. Between the first and final quarter of 2022 , TransUnion® reported that the average American’s creditcarddebt rose roughly $400 per person.

Today, about 61% of American households have creditcarddebt and the average creditcarddebt balance sits at $5,875. In January, overall delinquency grew with a 2.31% increase in delinquent accounts and 10.49% in delinquent balances month-over-month.

A growing number of Americans are keeping financial secrets from their loved ones, according to NerdWallet’s annual consumercreditcard report. In fact, a related NerdWallet survey […]

The Consumer Financial Protection Bureau released its fifth biennial report to Congress today on the consumercreditcard market, finding that the market’s growth over the last few years reversed course in 2020.

CFPB Looks at Medical Debt, Student Loans and So Much Data Medical debt wasnt the only focus for the Consumer Financial Protection Bureau in Q4. Moreover, many consumers, and especially those having trouble paying their monthly bills, report maxing out their cards regularly and using installment plans to cover basic necessities.

Mix in the fact that many consumers – enabled, in part, by historic levels of savings at least partly driven by government stimulus such as enhanced unemployment benefits – have shifted their focus to paying down their creditcarddebt, and the result is a greater than 10% decrease in the average creditcard balance and utilization of the U.S.

consumers took on $43 billion in additional creditcarddebt during the second quarter of this year, ending in June. That’s more than triple the average amount of new debt households have taken on in that period since after the Great Recession of 2007-08. Newly released data from WalletHub says U.S.

KNOXVILLE, Tennessee — The Federal Reserve Bank of New York has been tracking creditcarddebt since 1999. Creditcarddebt in the U.S. is at the highest level it’s been since then, with the total amount of debt in the third quarter of 2023 reaching around $1.08 trillion dollars. The post U.S.

The Consumer Financial Protection Bureau (CFPB) today filed a proposed order in federal district court against Burlington Financial Group and its owners and executives, Richard Burnham, Katherine Burnham, and Sang Yi, for allegedly deceiving consumers into hiring the company to lower or eliminate credit-carddebts and improve consumers’ credit scores. (..)

Creditcard balances reached a record-setting $866 billion in the third quarter of last year, which represents a year-over-year increase of 19%. Credit balances reached a record-setting $866 billion in the third quarter of last year – and they are expected to keep climbing, the report from TransUnion said. “We

Interest rates on creditcards have risen substantially, with average interest rates going over 20% . Given the trends for the 175 million Americans with creditcards, the CFPB estimates that outstanding creditcarddebt may continue to set records and could even hit $1 trillion.

Consumers trying to make ends meet have continued turning to creditcards and other credit types to bridge the income to expense gap. consumercreditcarddebt has increased to nearly $1 trillion. Creditcard balances jumped more than $60 billion over Q4 2022, lifting the total amount of U.S.

The report shows a slight uptick in total household debt in the second quarter of 2023, increasing by $16 billion (0.1%) to $17.06 The report is based on data from the New York Fed’s nationally representative ConsumerCredit Panel. The post Total Household Debt Reaches $17.06 trillion in the Q2 2023, marking a 4.6%

The CFPB explained that it is concerned about accumulating debt, regulatory arbitrage, and data harvesting in a consumercredit market already quickly changing with technology. The application process is quick, involving relatively little information from the consumer, and the product often comes with no interest.

Today, about 61% of American households have creditcarddebt and the average creditcarddebt balance sits at $5,875. The post How ConsumerCredit Trends Impact Debt Collection in 2024 appeared first on Collection Industry News.

It is prohibited for debt collectors to utilize unfair techniques, harass, or deceive consumers while seeking to collect consumerdebts under the federal Fair Debt Collection Practices Act (FDCPA). Consumerdebts include creditcarddebts, vehicle loans, medical costs, and school loans.

Implying that high interest rates are solely a result of lack of competition, the CFPB has: (i) published a proposed rule that would amend Regulation Z to decrease the safe harbor for creditcard late fees; (ii) launched an update of its creditcard database; (iii) and requested public feedback on how the consumercreditcard market is functioning.

Unfortunately, holiday creditcarddebt lingers far longer than leftover turkey. If you don’t—or can’t—repay holiday debt promptly, it’ll accumulate over time. Financial planning apps make life much easier, whether you’re saving or repaying holiday debt. How much debt does the average person owe? .

And that’s because it generally takes a few months for the effects of that event and the accompanying financial strain to start to show up in consumers’ credit reports, in the form of rising balances, credit seeking behavior, and eventually for some, missed payments. As of July 2020, U.S. FICO® Score over the coming months.

Rent Bureau , now owned by the credit bureau Experian, electronically compiles rental data from property management companies and individual landlords. Rental agencies and alternative credit providers use the data to screen applicants and establish consumercredit scores.

Information and data continue to be key tools at our disposal to better understand the dynamics of the last couple of years, and better navigate what lies ahead for the Canadian consumercredit environment. Average FICO® Score 10.

This is where they come into play—things like making loan and creditcard payments on time each month and maintaining a good debt usage or a credit utilization rate—the amount of debt, including creditcarddebt, you have in relation to your overall credit limit—can help you reach the credit score you’re after.

The report shows total household debt increased by $109 billion (0.6%) in Q2 2024, to $17.80 The report is based on data from the New York Fed’s nationally representative ConsumerCredit Panel. It includes a one-page summary of key takeaways and their supporting data points.

The report shows total household debt increased by $184 billion (1.1%) in the first quarter of 2024, to $17.69 The report is based on data from the New York Fed’s nationally representative ConsumerCredit Panel. The Quarterly Report also includes a one-page summary of key takeaways and their supporting data points.

News & World Report shows that more than eight in 10 Americans who have creditcarddebt are experiencing anywhere from a little to a lot of anxiety about it. Nearly 31% have at least $6,000 of creditcarddebt. have creditcarddebt of $10,000 or more.

As the federal funds rate rose, the prime rate did, as well, and creditcard rates followed suit. Why creditcarddebt keeps rising Despite the steep cost, consumers often turn to creditcards, in part because they are more accessible than other types of loans, according to Matt Schulz, chief credit analyst at LendingTree.

Creditcard borrowing rose in November to its highest monthly level since 2004 according to latest Bank of England data. billion in all forms of consumercredit, an increase on the £700m borrowed in October, of which £1.2 Net borrowing of mortgage debt by individuals increased from £3.6 billion to £4.4

This is why many people engage the services of a debt relief agency. TransUnion calculates that paying off $5,000 of creditcarddebt at the minimum rate costs $10,000 in interest. The fees you can expect to pay for Freedom Debt Relief’s services range from 15–25%. National Debt Relief vs. Freedom Debt Relief.

All three for-profit credit reporting agencies, Experian, Equifax and Transunion compile and report consumercredit and debt payment activity and sell this consumer information to lenders seeking to grant credit. Here’s why: Who Decides Your Credit Score? Key Takeaways.

“We did have a crisis,” said Brian Riley, director of credit advisory services at Mercator Advisory Group, “but because of the support that was given, it really kept the market for consumercredit steady.”. He added that card issuers behaved “a lot more rationally” in comparison with the 2007-2009 crisis.

And that’s because it generally takes a few months for the effects of that event and the accompanying financial strain to start to show up in consumers’ credit reports, in the form of rising balances, credit seeking behavior, and eventually for some, missed payments. As of July 2020, U.S. FICO® Score over the coming months.

Using the CFPB’s Making Ends Meet survey and consumercredit data, CFPB researchers found that financial conditions faced by renters and homeowners were divergent before the pandemic. “We must amplify and protect the modest gains renters made during the pandemic to ensure this nation’s full and equitable recovery from COVID-19.”.

A periodic survey by Bankrate found that 47% of cardholders carried debt from month to month in mid-2023, up from 39% at the end of 2021. The average card customer holds $6,088 in debt, according to a TransUnion report for the third quarter of 2023, up from $5,474 at the same time in 2022.

Americans borrowed a lot more money in May, according to new data from the Federal Reserve’s ConsumerCredit Report released in July. There was a 10% increase in credit use on a seasonally adjusted annual basis in May 2021. In May 2021, the total outstanding balance of consumercredit hit $4.25

“Amounts Owed” comprises some 30% of the overall FICO® Score calculation and is heavily weighted towards creditcard balances and utilization -- so the observed increase in creditcarddebt levels is contributing to the average score leveling off. Ethan has a B.S. See all Posts. chevron_left Blog Home. Average U.S.

This applies to unpaid debts such as: Unsecured debts: These are debts not tied to a specific asset, like creditcarddebt, medical bills, or personal loans. This includes creditcarddebt, medical bills, personal loans, and certain finance company charges.

Against this background, AG Bonta made recommendations to the agencies on how to protect consumers from harm in their use of medical payment products, including: The agencies should designate medical creditcarddebt as medical debt, not consumerdebt, to ensure consumers receive the appropriate statutory protections.

Circuit Court of Appeals ruled that the Fair Credit Reporting Act does not require consumercredit agencies to further investigate when a borrower disputes a debt collector’s ownership of their debt. Attorneys for the borrowers and credit agencies did not immediately reply to requests for comment on Friday.

On December 1, the Federal Reserve Board and the CFPB announced the dollar thresholds that determine exemption of certain consumercredit and lease transactions in 2022, from Regulation Z (Truth in Lending) and Regulation M (Consumer Leasing). For more information, click here. For more information, click here.

FICO® Score At 716, Indicating Improvement In ConsumerCredit Behaviors Despite Pandemic. Ethan Dornhelm wrote: The FICO® Score is the lingua franca, or common language, for the credit scoring industry. It serves as a broad-based, independent standard measure of credit risk. Fewer consumers are actively seeking credit.

Check out your credit score today! Credit.com provides consumerscredit monitoring solutions with a team dedicated to helping simplify the confusing world of credit. Find the resources and tools you need to help give your credit what it needs and ease the path to financial wellbeing. About Credit.com.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content