This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

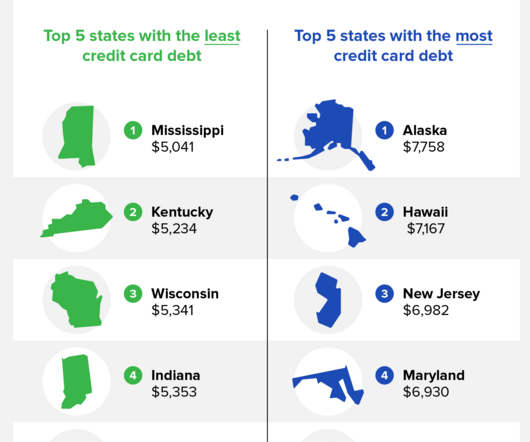

The average household creditcarddebt in America is $9,654, and the states with the largest amount of creditcarddebt are Alaska, Hawaii, and New Jersey. Between the first quarters of 2022 and 2023, The Federal Reserve Bank of New York reported that the creditcarddebt in America rose by $145 billion.

The average household creditcarddebt in America is $9,260, and the states with the largest amount of creditcarddebt are Alaska, Hawaii, and New Jersey. Between the first and final quarter of 2022 , TransUnion® reported that the average American’s creditcarddebt rose roughly $400 per person.

Interest rates on creditcards have risen substantially, with average interest rates going over 20% . Given the trends for the 175 million Americans with creditcards, the CFPB estimates that outstanding creditcarddebt may continue to set records and could even hit $1 trillion.

Implying that high interest rates are solely a result of lack of competition, the CFPB has: (i) published a proposed rule that would amend Regulation Z to decrease the safe harbor for creditcard late fees; (ii) launched an update of its creditcard database; (iii) and requested public feedback on how the consumercreditcard market is functioning.

This is where they come into play—things like making loan and creditcard payments on time each month and maintaining a good debt usage or a credit utilization rate—the amount of debt, including creditcarddebt, you have in relation to your overall credit limit—can help you reach the credit score you’re after.

CFPB Looks at Medical Debt, Student Loans and So Much Data Medical debt wasnt the only focus for the Consumer Financial Protection Bureau in Q4. Moreover, many consumers, and especially those having trouble paying their monthly bills, report maxing out their cards regularly and using installment plans to cover basic necessities.

Some lawmakers and regulators are calling for interest rate caps and lower fees on creditcards as debt levels march higher. Total creditcarddebt topped $1 trillion in the second quarter of 2023 for the first time ever. Federally chartered creditunions have an 18% limit. For example, Sen.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content