This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

A District Court judge in West Virginia has denied a motion to dismiss filed by a creditunion that is facing a class-action lawsuit for violating the West Virginia ConsumerCredit and Protection Act by charging a $5 fee to make payments over the telephone, ruling the creditunion is a debt collector under the […]

The Consumer Financial Protection Bureau has agreed to end a lawsuit by joining industry groups in asking a federal judge to vacate its controversial rule banning the reporting of medical debt on consumercredit reports. If it does, the rule will be vacated, and the CFPB will be barred from enforcing it.

A federal judge has approved a motion allowing two individuals and two consumer advocacy organizations to intervene in the legal fight over the Consumer Financial Protection Bureaus rule banning medical debt from consumercredit reports.

District Court for the Eastern District of Texas granted the CFPBs unopposed motion for a 90-day stay in the litigation filed by Cornerstone CreditUnion League and Consumer Data Industry Association (the Plaintiffs). WHAT THIS MEANS, FROM AYLIX JENSEN OF MOSS & BARNETT: OnFebruary 6, the U.S. More details here.

For creditunions and smaller banks in North America, the challenge of how to compete with their bigger counterparts is a constant and pressing matter. The solution integrates Equifax ConsumerCredit Information and FICO risk decision management technology with marketing campaign automation and execution.

CFPB Looks at Medical Debt, Student Loans and So Much Data Medical debt wasnt the only focus for the Consumer Financial Protection Bureau in Q4. Then, the Bureau finalized a rule on federal oversight of digital payment apps to protect personal data, reduce fraud and stop illegal debanking.

Today, you have six years to collect monies owed from consumercredit transactions. However, a bill approved by the New York Senate seeks to shorten the time to collect consumercredit transactions to three years. Creditunion loan. Credit cards. Personal bank loans. Home equity loans.

Bankers are opposing any effort by the Consumer Financial Protection Bureau (CFPB or Bureau) to reduce or eliminate the late fee safe harbor, citing a potentially significant adverse impact on community banks and creditunions.

For creditunions and smaller banks in North America, the challenge of how to compete with their bigger counterparts is a constant and pressing matter. The solution integrates Equifax ConsumerCredit Information and FICO risk decision management technology with marketing campaign automation and execution.

These in-depth insights can help lenders expertly manage credit risk in these uncertain times, while continuing to make competitive credit offers to consumers. . We have used FICO® Scores for many years. For more information about the FICO® Score 10 Suite, please visit: [link].

Implying that high interest rates are solely a result of lack of competition, the CFPB has: (i) published a proposed rule that would amend Regulation Z to decrease the safe harbor for credit card late fees; (ii) launched an update of its credit card database; (iii) and requested public feedback on how the consumercredit card market is functioning.

Federal Activities: On December 16, the Consumer Financial Protection Bureau (CFPB) issued a series of orders to five companies offering “buy now, pay later” (BNPL) credit. The CFPB is concerned about accumulating debt, regulatory arbitrage, and data harvesting in a consumercredit market already quickly changing with technology.

The report found that roughly a quarter of consumers are still being charged these fees despite the CFPB’s hostility towards so called “junk fees,” which has led many banks and creditunions to eliminate such fees. Overdraft fees are somewhat more prevalent than NSF fees (23.6% versus 20%, respectively).

The law does not apply to banks, savings and loan associations, savings banks, thrift companies, or creditunions. Providing inaccurate information to a credit bureau. Misapplying student loan payments to the outstanding balance.

Bankers are gearing up to oppose an effort by the Consumer Financial Protection Bureau (CFPB or Bureau) to prevent an increase in allowable late charges for credit cards. In letters dated August 1, the American Bankers Association , Consumer Bankers Association, CreditUnion National Association, and National Association of Federally?Insured

Using credit irresponsibly by making late payments and maxing out credit limits can have an affect your credit negatively and lower your credit score. How Does Credit Reporting Work? The bureaus collect and store your credit information in your credit file for future reference.

Specifically, the final rule provides for the following adjustments: For open-end consumercredit plans under TILA, the threshold that triggers requirements to disclose minimum interest charges will remain unchanged at $1.00 The rule takes effect on January 1, 2022. 8% of the total loan amount for a loan amount less than $14,356.

After New York Governor Andrew Cuomo signs the ConsumerCredit Fairness Act (S.153/Thomas) 153/Thomas) into law, many creditors will need to provide significant documentation in order to file a debt collection action against their non-paying consumers.

AI also can inform credit decisions by analyzing traditional data ( i.e., data typically found in a consumers’ credit files) and alternative data. Five federal banking regulatory agencies are gathering information and comments on financial institutions’ use of artificial intelligence (AI), including machine learning.

Experian reports that the lowest FICO credit score is 300, but no one really stays at such a low score once some financial history has been established. If you’re not in the habit of checking your credit score every month, you can hire a credit monitoring company to do the tracking for you. And that’s encouraging to think about.

The Consumer Financial Protection Bureau issued a request for information to examine the impact of the rules that implement the Credit Card Accountability Responsibility and Disclosure Act of 2009.

There are some exceptions: The Military Lending Act caps interest for active duty servicemembers and dependents at 36% for consumercredit. Federally chartered creditunions have an 18% limit. Eight trade groups representing lenders such as banks and creditunions wrote a letter to Sen. For example, Sen.

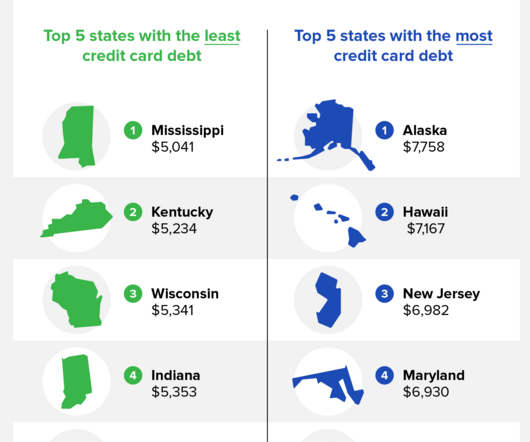

Here are the standout findings of various debt statistics: The average American household has over $9,000 in credit card debt. WalletHub ) Mississippi has the least credit card debt at $5,259 per person. Credit Karma ) Alaska has the most credit card debt on average at $8,139.

The revamped survey will mean that dominant credit card issuers will be more transparent by requiring them to publish average interest rates based on credit score ranges. Small banks and creditunions will also now have a chance to have their prices displayed next to those of the largest ones.

This will not only help you compare your own credit card balance to the national average, but you’ll also see if you’re getting a good deal with your current cards. How many credit cards carry a balance? The APR is the amount of interest consumers pay for their purchases, and the following table is broken down by credit card type.

The insured creditor and its affiliates do not maintain an escrow account for consumercredit transactions secured by real property or a dwelling, other than: Escrow accounts established after consummation as an accommodation to distressed consumers to assist such consumers in avoiding default or foreclosure, or.

The legislation would benefit banks and creditunions with assets under $15 billion. On October 23, lawmakers in the House of Representatives introduced a bill to exclude Paycheck Protection Program (PPP) loans from regulators’ calculations of the asset size of smaller banks. For more information, click here.

On October 11, the Consumer Financial Protection Bureau (CFPB) issued an advisory opinion concerning consumers’ requests for information regarding their accounts with large banks and creditunions. For more information, click here. For more information, click here. For more information, click here.

In a letter sent to the leaders of the House and Senate , CUNA President/CEO Jim Nussle stated his objections to section 403 of the bill, which would amend the Fair Credit Reporting Act to prohibit credit scoring models from treating certain medical debt information on consumers’ credit report as a negative factor.

Consumers can reach the DFPI at (866) 275-2677 or Ask.DFPI@dfpi.ca.gov. The post California DFPI Continues To Expand Consumer Protection Efforts During The COVID-19 Pandemic appeared first on Collection Industry News.

The DFPI licenses and regulates state-chartered banks and creditunions, commodities and investment advisers, money transmitters, the offer and sale of securities and franchises, broker-dealers, nonbank installment lenders, payday lenders, mortgage lenders and servicers, escrow companies, Property Assessed Clean Energy (PACE) program administrators, (..)

Two trade groups the Consumer Data Industry Association (CDIA) and the Cornerstone CreditUnion League yesterday filed a lawsuit in the District Court for the Eastern District of Texas against the Consumer Financial Protection Bureau over its new rule prohibiting the inclusion of most medical debts on consumercredit reports.

A federal judge has granted a 90-day stay on the Consumer Financial Protection Bureaus new rule that would bar credit reporting agencies from including medical debt on consumercredit reports.

Covered institutions include banks, savings associations, creditunions, and mortgage companies. As the most comprehensive publicly available information on mortgage market activity, HMDA data is used by industry, consumer groups, regulators, and others to assess potential fair lending risks and for other purposes.

On June 8, the board of governors for the Federal Reserve (the Fed), Consumer Financial Protection Bureau (CFPB), Federal Deposit Insurance Corporation (FDIC), National CreditUnion Administration (NCUA), and the OCC requested public comment on proposed guidance addressing reconsiderations of value (ROV) for residential real estate transactions.

Among the changes discussed by Governor Hochul in her State of the State Address is a plan to amend the state’s ConsumerCredit Fairness Act to cover medical debt. The proposals will modify the cost and delivery of care so that no New Yorker will not “have to choose between their health and their financial security.”

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content