This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The investing information provided on this page is for educational purposes only. Three major consumer companies have been involved in separate credit reporting issues recently. The article Money News: 3 Companies Commit Major ConsumerCredit Blunders originally appeared on NerdWallet. Email: hal@nerdwallet.com.

When we launched FICO’s “Score A Better Future” program in October 2018, our main goal was to continue to expand consumercredit access through financial education. These free events are designed to demystify credit and give consumers the tools – including non-profit credit counseling – to take control of their financial health.

“Amounts owed” comprises some 30% of the overall FICO® Score calculation and is heavily weighted towards credit card balances and utilization so the observed reduction in credit card debt is helping to drive scores upwards. Fewer consumers are actively seeking credit. There has been a 12.1% The Other Side of the Coin.

Organization: American ConsumerCredit Counseling. Mission statement: “ACCC strives to empower consumers to regain control over the quality of their lives through financial education, counseling and debt management,” says Katie Ross, executive vice president of. Anna Helhoski writes for NerdWallet. Twitter: @AnnaHelhoski.

CFPB Looks at Medical Debt, Student Loans and So Much Data Medical debt wasnt the only focus for the Consumer Financial Protection Bureau in Q4. and was broad-based across income and education groups. Additionally, the average perceived probability of missing a minimum debt payment over the next three months increased to 14.2%

On November 13, the Consumer Financial Protection Bureau (CFPB) and the Federal Reserve Board (Fed) announced increased dollar thresholds used to determine whether certain consumercredit and lease transactions in 2024 are exempt from Regulation Z (Truth in Lending) and Regulation M (Consumer Leasing).

According to the Federal Reserve’s ConsumerCredit report, 43.5 Not only can you not declare bankruptcy on many forms of student loan debt, but it can also harm your credit. Department of Education shows how many Americans have debt by federal loan type. At the end of 2022, the Federal Reserve reported that roughly 43.5

So credit repair, consumercredit and credit bureaus—they’re all tied together. To understand why they’re so important, you might want to learn a bit more about the history of credit scores and repair. Luckily, we’ve compiled everything you need to know about the history of the credit repair industry.

District Court for the Middle District of Alabama joined a growing number of courts dismissing FCRA claims based upon a furnisher’s alleged failure to remove an “account in dispute” notation from consumercredit reports. In Griffin v. Experian Information Solutions, Inc. , 1:20-cv-801-RAH-SMD, 2021 WL 3782141 (M.D.

Find out more about free credit repair for low-income families and individuals below. Educating Yourself on ConsumerCredit Sites When it comes to free credit repair and report help, consumercredit sites are a great resource. The Consumer Financial Protection Bureau.

“The most important thing for us is to deliver value to the consumer. The hardest working Americans at the core of our mission need a product that puts them first, and provides more than an educational score.” It does this by tapping into five key features that make ExtraCredit stand out among other credit tools.

Khan Academy is an educational platform that has been around for many years. edX is a renowned educational platform with numerous world-class universities providing free courses on it. Like edX, Coursera is a popular educational platform with top universities offering courses. . #1 Khan Academy’s Personal Finance Course.

CFPB Director Rohit Chopra explained the decision to undertake the review at the time by stating, “Schools that offer students loans to attend their classes have a lot of power over their students’ education and financial future. Students who cannot obtain transcripts can be locked out of future higher education and certain job opportunities.

ConsumerCredit Act 1974 : This act regulates consumercredit and related services. It provides rights to consumers and outlines the responsibilities of lenders. Internal Training and Education To ensure adherence to compliance standards, continuous internal training and education are paramount.

On June 14, Nevada Governor Joe Lombardo signed into law AB 332 , An Act Relating to Student Education Loans, requiring, among other things, student loan servicers to be licensed by the Commissioner of Financial Institutions and regulating certain conduct of the servicers towards borrowers. Providing inaccurate information to a credit bureau.

The passing of the ConsumerCredit Fairness Act , which requires creditors attach a list of additional documents to the pleading when filing suit within New York to recover monies owed as a result of consumercredit transactions. Laws or Bills Introduced in 2022 That Affect Debt Collection in New York.

And that’s because it generally takes a few months for the effects of that event and the accompanying financial strain to start to show up in consumers’ credit reports, such as in the form of rising balances, credit seeking behavior, and eventually for some, missed payments. consumers decreased on a year-over-year basis.

– Come July 1, 2022, paid medical collection debt won’t be used for credit scores and unpaid medical debt won’t appear for a full year, according to the three main credit reporting agencies (NCRAs) – Equifax, Experian and TransUnion. The move follows months of industry research.

AI also can inform credit decisions by analyzing traditional data ( i.e., data typically found in a consumers’ credit files) and alternative data. For example, financial institutions use chatbots and virtual assistants to mimic live employees and automate routine customer interactions.

Back in 2013, we reported the New York State General Assembly’s passage of the ConsumerCredit Fairness Act , which introduced new requirements for debt collection litigation against consumers. The shortening of the statute of limitations cut the time to sue in half, from 6 years from the date of service to 3 years.

On May 26, the CFPB issued a blog post regarding credit reporting disputes and requirements that furnishers must satisfy when handling a dispute. For more information, click here.

On December 1, the Federal Reserve Board and the CFPB announced the dollar thresholds that determine exemption of certain consumercredit and lease transactions in 2022, from Regulation Z (Truth in Lending) and Regulation M (Consumer Leasing). For more information, click here. For more information, click here.

Instead, I suggest you do what you can to educate yourself about your options. Credit Counselor. A credit counselor is certified and trained in consumercredit, money and debt management, and budgeting. Here are 9 terms you may have heard of, but need to know more about. FDCPA ( Fair Debt Collection Practices Act).

The ConsumerCredit Protection Act caps these types of garnishments. Educate yourself on smart ways to pay debt collectors , and consider using the services of a debt management agency. When your employer receives the proper legal notice, they must withhold a percentage of your wages. The lessor of these two amounts applies.

Regardless of this uncertainty, FICO’s mission is clear: to help lenders understand the credit risk that each borrower represents and make better-informed lending decisions and to educate and empower consumers. FICO® Score at 716, Indicating Improvement in ConsumerCredit Behaviors Despite Pandemic. See all Posts.

Rent Bureau , now owned by the credit bureau Experian, electronically compiles rental data from property management companies and individual landlords. Rental agencies and alternative credit providers use the data to screen applicants and establish consumercredit scores.

It gathers credit reports from the three major credit bureaus and analyzes anonymous consumer data to generate a scoring model specific to each bureau. VantageScore, on the other hand, uses a combined set of consumercredit files, also obtained from the three major credit bureaus, to come up with a single formula.

Though you may be unfamiliar with Fairway, the agency collects on a wide range of consumer debts, including the following: Health insurance billing and follow-up. Education loans, tuition, fines and fees. Credit cards. Self-pay collections. Parking tickets. Government fines and fees. Utility bills. Checking and savings.

TransUnion ( NYSE: TRU ) confirmed that consumercredit activity keeps rising from the COVID-19 pandemic lows, but some areas like automobile loans (subprime) performance have lagged. Matt Komos , VP of Research and Consulting at TransUnion, stated: “On the surface, the consumercredit market is performing quite well.

All three for-profit credit reporting agencies, Experian, Equifax and Transunion compile and report consumercredit and debt payment activity and sell this consumer information to lenders seeking to grant credit. Here’s why: Who Decides Your Credit Score? Key Takeaways.

The DFPI investigations resulted in 49 public enforcement actions, $975,000 in restitution to consumers, $547,500 in penalties, and included several “first of its kind” actions for the DFPI in debt collection, student debt relief, earned wage access, and private post-secondary education financing. Regulatory Activities.

Credit when it's offered responsibly is a social good. For many, it creates an opportunity to improve their life circumstances; to get an education, to buy a car to get to work, or to own a home. Through myFICO we also offer score simulators, which provides another level of educational information. Plus, in many U.S.

Other recommendations address, among other things, the use of alternative data; suggested changes to the Bureau’s internal organization; competition in the consumer financial marketplace, including with respect to the cost of credit, the effect and burden of state licensure requirements, and settlement servicing prices; consumercredit reporting, including (..)

What’s more, unlike some fintech initiatives that assess risk based on cash flow data alone, the UltraFICO® Score presents the best of both worlds, combining cash flow data with traditional data from consumers’ credit files, along with the odds-to-score ratio that lenders understand.

The Taskforce Report uses five interrelated principles that serve as the foundation for proposed systematic changes to the current legal and regulatory framework: consumer protection, information and education, competition and innovation, regulatory modernization and flexibility, and inclusion and access.

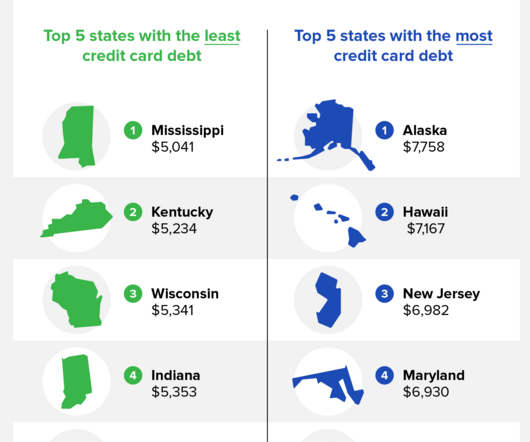

Here are the standout findings of various debt statistics: The average American household has over $9,000 in credit card debt. WalletHub ) Mississippi has the least credit card debt at $5,259 per person. Credit Karma ) Alaska has the most credit card debt on average at $8,139.

Among other things, Moody underscored the (1) Senior Protection Team – an intra-agency group of experts who work together to fight fraud and assist seniors; (2) Seniors vs. Crime Program – a program that uses volunteer retired citizens to educate Floridians on consumer fraud and to assist in select consumer investigations; and (3) Scams at Glance Program (..)

Here’s what you need to know: Key Regulations to Consider: The ConsumerCredit Act: This act regulates credit agreements and includes provisions that debt collectors must adhere to, ensuring fairness and transparency in all dealings.

The Taskforce issued over 100 recommendations, of which seven were directly focused on improving consumercredit reporting and the Fair Credit Reporting Act (“FCRA”) and consumercredit reporting generally. The Bureau should assess periodically the accuracy and completeness of consumercredit reports.

The department’s objective in drafting these new rules is to include all education financing products used to finance a student’s higher education, including income share agreements and installment contracts, within the definition of student loans subject to state law. For more information, click here.

The report raises questions about whether some marketing deals between colleges and financial institutions comply with Department of Education rules. For more information, click here. For more information, click here.

On July 26, the CFPB published a blog focused on consumercredit scores. On July 25, a large credit reporting agency revealed to investors in regulatory filings that it’s facing a probe by the CFPB. For more information, click here. For more information, click here.

Federal Activities: On December 16, the Consumer Financial Protection Bureau (CFPB) issued a series of orders to five companies offering “buy now, pay later” (BNPL) credit. The CFPB is concerned about accumulating debt, regulatory arbitrage, and data harvesting in a consumercredit market already quickly changing with technology.

This will not only help you compare your own credit card balance to the national average, but you’ll also see if you’re getting a good deal with your current cards. How many credit cards carry a balance? To begin managing your credit and your debt, sign up for a free credit report card and check out ExtraCredit.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content