This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Confessions of judgment may no longer be permitted as part of the necessary documents when buying or selling financialservices or products to consumers in New York. The proposed bill does not currently apply to commercial lenders. Therefore, it will most likely be “business as usual” for commercial lenders and the like.

The FTC’s Safeguards Rule requires nonbanking financial institutions, such as mortgage brokers, motor vehicle dealers, and payday lenders, to develop, implement, and maintain a comprehensive security program to keep their customers’ information safe. financial institutions. For more information, click here.

On March 4, the Small Business Administration (SBA) announced the next generation of the SBA’s Lender Match tool for small businesses to connect to capital through SBA’s network of approved banks and private lenders. If enacted, the bill would, among other things, prohibit medical debts from being reported on consumers’ credit reports.

On May 24, the CFPB announced that it will open the Office of Competition and Innovation as part of a new approach to help spur innovation in financialservices by promoting competition and identifying stumbling blocks for new market entrants. For more information, click here.

On July 27, the Financial Innovation and Technology for the 21st Century Act passed the House Committee on Agriculture. The bill previously passed the House Committee on FinancialServices on July 26. On July 26, the CFPB published a blog focused on consumercredit scores. For more information, click here.

Federal Activities: On September 29, the ConsumerFinancial Protection Bureau (CFPB) released its fifth biennial report to Congress on the consumercredit card market, finding that the market’s growth over the last few years reversed course in 2020. Privacy and Cybersecurity Activities. Among other provisions, S.B.

The four key trends we’re studying are: resumed foreclosure activity, extensive medical bills, the end of child tax credits and historically high inflation. Add these all together and the financial outlook for consumers, especially those in debt, is scary. And lenders are happy to lend.

The proposed rule would require lenders to assess a borrower’s ability to repay a PACE loan and would provide a framework for how these loans will be treated under the Truth in Lending Act. PACE loans, secured by a property tax lien on the borrower’s home, are often promoted as a way to finance clean energy improvements, such as solar panels.

In its report, the Taskforce makes approximately 100 recommendations to the CFPB, Congress, and state and federal regulators to strengthen consumer protection. To promote access to capital, initially, only community financial institutions can make First Draw PPP Loans on Monday, January 11, and Second Draw PPP Loans on Wednesday, January 13.

2547 was sponsored by House FinancialServices Committee Chairwoman Rep. While consumer groups praised the bill for its recourse for consumers harassed by debt collectors, CUNA and NAFCU saw the bill as complicating the legal relationship between consumers, members and lenders. The bill, H.R.

which along with the Fair Debt Collection Practices Act, Telephone Consumer Protection Act, Section 5 of the Federal Trade Commission Act, and the Truth in Lending Act, forms the foundation of federal consumer rights law in the United States. . § 1681, et seq.), and throughout the world.

A more predictive credit score means more predictable cash flows which are, in turn, more attractive to investors for all types of securitized assets (e.g., mortgages, auto loans, credit cards, etc.) offering continuity and stability for lenders, investors, and consumers.

FICO will present key insights gained from recent FICO® Resilience Index research and early lender adoption use cases across the consumercredit lifecycle at several key industry events starting later this month. To learn more, watch the recent Consumer Bankers Association webinar.

The COVID-19 pandemic cast a huge shadow on the financialservices worldwide. The FICO Blog posts last year reflected that – we wrote about everything from the impact on collections, proactive lender communications with consumers, issues with fraud, and of course, how FICO® Scores were impacted.

More specifically, the Department of FinancialServices will crack down on the “buy now, pay later” industry. Buy now, pay later services act as a lender of sorts and are currently not licensed by the state. Medical Debt Medical debt was another topic addressed in the State of the State address.

What’s more, unlike some fintech initiatives that assess risk based on cash flow data alone, the UltraFICO® Score presents the best of both worlds, combining cash flow data with traditional data from consumers’ credit files, along with the odds-to-score ratio that lenders understand. See all Posts. chevron_left Blog Home.

On January 20, 2023, California Attorney General Rob Bonta submitted a letter to the CFPB agreeing with its preliminary determination that California’s Commercial Financing Disclosures Law (CFDL) is not preempted by TILA because the CFDL only applies to commercial financing and not to consumercredit transactions within the scope of TILA.

Wondering why DFS/Webbank showed up on your credit report? Short for Dell FinancialServices/Webbank, the entry is probably on your report because you applied for a Dell Preferred Account. Most of the time, a hard inquiry from a lender or service provider is nothing to panic over. DFS/Webbank On My Credit Report.

FICO® Resilience Index: Resilient Credit Lifecycle Strategies Are a Requirement. FICO ® Resilience Index tools that measure consumer resiliency, benefit lenders in a recessionary environment. How can lenders build, manage, and secure credit portfolios in today’s uncertain market environment? by Moma Chakraborty.

FICO® Resilience Index: Resilient Credit Lifecycle Strategies Are a Requirement. FICO ® Resilience Index tools that measure consumer resiliency, benefit lenders in a recessionary environment. How can lenders build, manage, and secure credit portfolios in today’s uncertain market environment? by Moma Chakraborty.

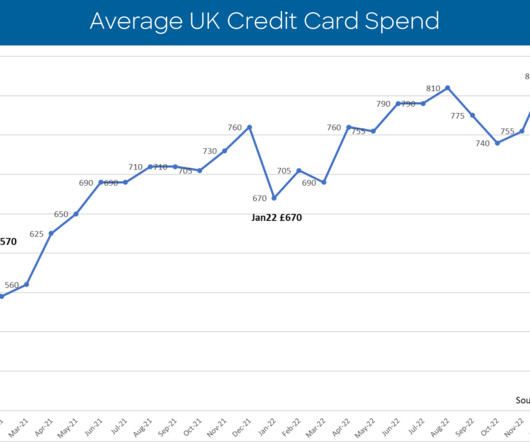

Highlights Average total sales per card down 8 percent compared to December 2022 at £755 Percentage of credit card accounts with two missed payments 13.6 percent higher than December 2022 Average balance on credit card accounts with two missed payments was 1.9 percent month on month — which could ring alarm bells for lenders.

In 2021, the financialservices world continued to grapple with the uncertainty brought on by year two of the COVID-19 pandemic. FICO® Score At 716, Indicating Improvement In ConsumerCredit Behaviors Despite Pandemic. It serves as a broad-based, independent standard measure of credit risk. Average U.S.

That’s why FICO has been focused on finding new ways to demonstrate responsible financial behavior so that lenders can confidently extend credit to more consumers. . Over the past several years, we’ve helped lenders develop on-ramps to mainstream credit using alternative data for those seeking financial inclusion.

On March 1, the ConsumerFinancial Protection Bureau (CFPB) released its “ Medical Debt Burden in the United States ” report, which questions whether consumercredit reports should include unpaid medical billing data. totaling $88 billion in medical bills in 2021. Work with other federal agencies, including the U.S.

When asked what factors were most important to them in selecting a credit score model, more than half (55%) ranked a score’s ability to predict credit risk highest on their list, followed by a score that was proven over time (32%).

Alternative credit reporting relies on different types of financial data such as utility payment history, rental payment history, and information from alternative financialservice providers, like short-term lenders allowing previously invisible consumers who were considered high-risk to have greater access to opportunities when it comes to borrowing. (..)

As a data scientist working on credit models in the late 80s, it was a mission to help replace human bias with data-driven science. in 1989, it meant lenders of all sizes could leverage the technology of scoring and open up credit to consumers that they might not have lent to in the past. Hundreds of lenders in the U.S.

More specifically, the Department of FinancialServices will crack down on the “buy now, pay later” industry. Buy now, pay later services act as a lender of sorts and are currently not licensed by the state. Medical Debt Medical debt was another topic addressed in the State of the State address.

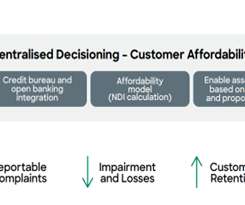

It is one of the biggest challenges lenders face over the next few years. Lenders could no longer base decisions simply on a customer’s history of repaying. Lenders have refined and improved their affordability models over the years in adherence to regulatory requirements. Affordability is top of mind.

Meanwhile, eyes are on the Big Apple as the New York Department of FinancialServices (DFS) and the New York City Department of Consumer and Worker Protection are simultaneously engaged in amending their consumer debt collection rules. consumercredit card debt has increased to nearly $1 trillion.

A hike in the federal interest rate prompts a jump in the Bank Prime Loan Rate ( prime rate ), the credit rate that banks offer to their most credit-worthy customers and off of which they base other forms of consumercredit like mortgages and consumer loans. Key Factor 3: Rising Delinquencies.

He has over 30 years’ experience working in senior roles across the technology, financialservices and publishing industries and has a passion for using technology and pioneering approaches to drive outstanding business growth and customer retention. Tomas Klinger, decision science and data director at Home Credit (previous winner).

In its complaint, the FTC cites representations made to consumers on IT Media Solutions’ network of websites, which assured consumers that their information only would be shared with “trusted lenders, lending partners and financialservices providers.” Consent Order Requirements and Penalties.

Instead, the orders are focused on the CRAs’ marketing of credit related reporting services. According to the Consent Orders, the CRAs marketed and sold consumerscredit scores and credit related products. Equifax Order, ¶ 23; see also TransUnion Order, ¶ 29.

1987 (i)(6) (“The term “consumercredit” … does not include a loan procured in the course of purchasing a car or other personal property, when that loan is offered for the express purpose of financing the purchase and is secured by the car or personal property procured.”). No court order is required. We have the experience to assist.

Earlier this month, a district court for the Eastern District of Michigan dismissed on its own initiative a Fair Credit Reporting Act (FCRA) claim brought by a consumer alleging inaccurate reporting of her charged-off vehicle loan. Americredit FinancialServices, Inc. The court’s opinion in Shelton v.

SACRAMENTO – More than a year into the COVID-19 pandemic, the California Department of Financial Protection and Innovation (DFPI) continues to expand efforts to protect consumers from financial impacts of the lethal virus that has ravaged the state’s economy and killed more than 53,000 Californians.

The CFPB also released several reports shining a light on factors that may influence fair access to credit, including how medical debt affects tens of millions of consumers’ credit profiles, how people in under-resourced rural areas struggle to access financialservices, and the challenges faced by justice-involved individuals and families.

Using the CFPB’s Making Ends Meet survey and consumercredit data, CFPB researchers found that financial conditions faced by renters and homeowners were divergent before the pandemic. During the pandemic, renters’ financial conditions, on average, appeared to improve as much as or more than those of homeowners.

In 2021, the Office of Financial Technology and Innovation (OFTI) met with dozens of companies, venture capitalists, lawyers, industry advocacy groups, federal and state financial regulators, consumer advocacy groups, and academics to better understand stakeholder perspectives on what constitutes responsible innovation in financialservices.

It directly relates to research undertaken in 2010 when empirical evidence showed that economic victims have very different risk profiles and often respond very differently when they’re struggling to service personal debt. Prior to the 2008 global financial crisis, the average RtFG of consumercredit customers having reached charge-off was 2.5

On January 25, the ConsumerFinancial Protection Bureau (CFPB) released a blog post on consumercredit score transitions during the COVID-19 pandemic. On January 24, the CFPB issued a request for information, seeking public input on how the consumercredit market is functioning.

On June 6, Colorado Governor Jared Polis signed HB 23-1229, which amends the state’s Uniform ConsumerCredit Code (UCCC). These amendments will become effective on July 1, 2024, and will govern consumercredit transactions occurring after that date. For more information, click here.

Federal Activities: On April 14, the ConsumerFinancial Protection Bureau (CFPB or Bureau) published a report titled, “ Student Loan Borrowers Potentially At-Risk when Payment Suspension Ends.” For more information, click here.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content