This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Senate Bill 5480, introduced in the 69th Legislature, aims to void and make unenforceable any medical debt that is reported to a consumercredit reporting agency or credit bureau. Failing to pay a debt and being subject to foreclosure, eviction, and litigation is understandably difficult for consumers.

Chase was one of 13 financial institution censured for robo-signing documents in support of debt collection suits and foreclosure. The banks’ actions harmed many consumers’ credit, and the banks had to pay billions to borrowers. But robo-signing wasn’t just happening within Chase.

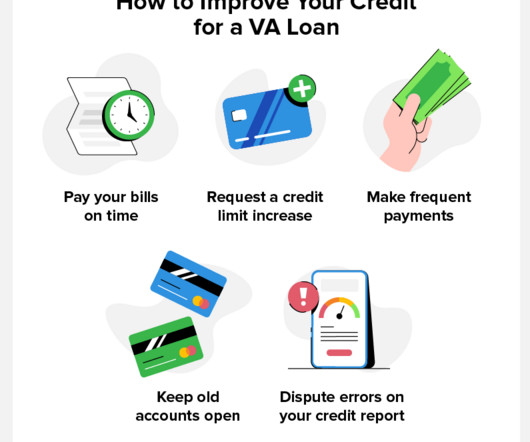

Table of Contents: What Is the Minimum Credit Score for a VA Loan? Compensating Factors Your Lender May Take Into Account Other VA Loan Requirements How to Get a VA Loan After Bankruptcy or Foreclosure Who Qualifies for a VA Loan? Here’s an overview of how to get a loan after foreclosure or bankruptcy.

The four key trends we’re studying are: resumed foreclosure activity, extensive medical bills, the end of child tax credits and historically high inflation. Add these all together and the financial outlook for consumers, especially those in debt, is scary. But there are silver linings, as well. million U.S.

In a letter sent to the leaders of the House and Senate , CUNA President/CEO Jim Nussle stated his objections to section 403 of the bill, which would amend the Fair Credit Reporting Act to prohibit credit scoring models from treating certain medical debt information on consumers’ credit report as a negative factor.

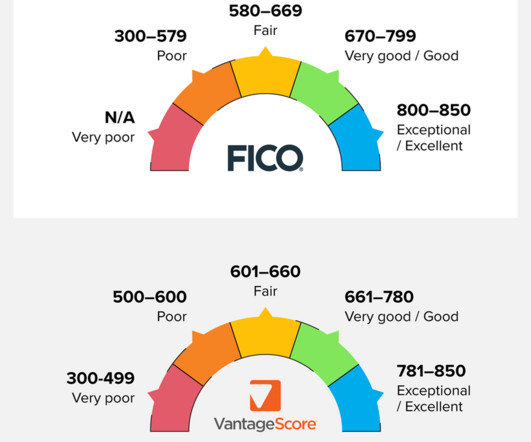

For example, your mortgage credit score vs. consumercredit score may differ if you have late mortgage payments or a foreclosure on your credit report. The most common version is the FICO 8 model, but they also have industry-specific scores for when you’re looking to take out a loan for a vehicle or a mortgage.

In addition, the department has stepped up measures to expose and track emerging scams, field and respond to a large increase in consumer complaints and inquiries, connect struggling consumers with available resources, and to work with licensees to ensure compliance with state and federal laws enacted to protect homeowners from foreclosures.

The report is based on data from the New York Fed’s nationally representative ConsumerCredit Panel. Credit card balances increased by $45 billion, from $986 billion in Q1 2023 to a series high of $1.03 About 39,000 individuals had new foreclosure notations on their credit reports, a very small increase from the first quarter.

This applies to unpaid debts such as: Unsecured debts: These are debts not tied to a specific asset, like credit card debt, medical bills, or personal loans. Overdue child support or alimony payments Unpaid taxes Federal laws, like the ConsumerCredit Protection Act (CCPA) , limit the amount of your wages that can be garnished.

If you’re stressing out about dealing with Fairway, you may want to look into working with a credit repair company. Credit repair companies are expertly trained and well-equipped to handle a variety of consumercredit issues, including confronting debt collectors. Foreclosure. Charge-offs. Hard inquiries.

On July 26, the CFPB published a blog focused on consumercredit scores. On July 25, a large credit reporting agency revealed to investors in regulatory filings that it’s facing a probe by the CFPB. For more information, click here. As part of the introduced public resolution, Councilmember Robert C.

Depending on the extent of your credit problems, your best bet might be to work with a credit repair specialist. Credit repair companies are pros at disputing inaccuracies and getting them deleted from consumers’ credit reports. Even more, they can assist you with challenging credit problems like: Bankruptcy.

Depending on the extent of your credit problems, your best bet might be to work with a credit repair specialist. Credit repair companies are pros at disputing inaccuracies and getting them deleted from consumers’ credit reports. Even more, they can assist you with challenging credit problems like: Bankruptcy.

While you may have applied for a loan from a popular lender or bank, their name isn’t necessarily the one that will appear on your credit report. Instead, banks, lenders, and other financial institutions turn to consumercredit reporting companies like CBCInnovis to vet applicants. Foreclosures. Charge offs.

Lenders and service providers turn to companies like ACRAnet in order to obtain consumercredit reports to aid them in their approval process. National Consumer Reporting Association. They deal with more than just hard inquiries, too, helping people to rebuild their credit in the aftermath of: Bankruptcy. Foreclosure.

The insured creditor and its affiliates do not maintain an escrow account for consumercredit transactions secured by real property or a dwelling, other than: Escrow accounts established after consummation as an accommodation to distressed consumers to assist such consumers in avoiding default or foreclosure, or.

There are several excellent credit repair companies that are experts at disputing inaccuracies and improving consumers’ credit scores. Foreclosure. Credit repair specialists can help you get to the bottom of your credit problems so you can improve your score quickly. Charge-offs. Debt collectors.

They’re pros at getting inaccurate hard inquires removed from consumercredit reports. A credit repair company is also a great asset if you’re facing any of the following: Bankruptcy. Foreclosure. Charge offs. Debt collections. Late payment history.

Data Facts is a credit reporting company that is primarily used by employers to vet applicants. They run background checks on prospective employees, accessing documents like consumercredit reports to assess their financial responsibility. They will take the necessary steps to get faulty entries off your credit report.

RentGrow On Your Credit Report. RentGrow is an agency that obtains consumercredit reports for landlords. Whether your biggest concern is a hard inquiry or you’re battling lots of credit problems, they’ll have your back. Here are a few of the credit issues they can help out with: Bad payment history. Foreclosure.

Citi is a popular bank that provides credit cards for a wide range of retail stores like The Home Depot. With The Home Depot, in particular, Citi offers four credit options: ConsumerCredit Card. When you apply for any one of these cards, loans, or credit accounts, you authorize Citibank to run a hard credit check.

a revolving line of credit for financing Dell products. The account offers rewards when you purchase products from Dell using the credit, along with interest-free financing on several products. When DFS/Webbank shows up on consumercredit reports, it’s most likely because an application was submitted, leading to a hard inquiry.

Whether you’re anxious just thinking about calling the credit bureaus to dispute a hard inquiry or you simply don’t have the time, you might want to leave it to the pros. Credit repair companies specialize in disputing inaccuracies on consumercredit reports, getting fraudulent entries deleted quickly. Foreclosure.

File a Dispute with the Credit Bureaus. The Fair Credit Reporting Act requires credit bureaus to investigate questionable entries on consumercredit reports. They’ll then have 30 days to look into the inquiry and remove it if it is evident that you didn’t consent to the credit check. Collections-stage debt.

File a Dispute with the Credit Bureaus. The Fair Credit Reporting Act requires credit bureaus to investigate questionable entries on consumercredit reports. They’ll then have 30 days to look into the inquiry and remove it if it is evident that you didn’t consent to the credit check. Collections-stage debt.

You need to know, when you have a score on a consumer that you're getting a solid indication of credit risk, you need to know that you're not putting the consumer at greater risk of a foreclosure because a score used in a credit decision for a mortgage or auto loan, was based on a small amount of data, or stale data.

The legislation prevents any potential gap in the law and protects homeowners from foreclosures as they continue to await approvals and payments from the Department of Housing and Community Development (DHCD). For more information, click here. On October 11, B25-0449 was signed by Mayor Muriel Bowser (D). For more information, click here.

On January 25, the Consumer Financial Protection Bureau (CFPB) released a blog post on consumercredit score transitions during the COVID-19 pandemic. On January 24, the CFPB issued a request for information, seeking public input on how the consumercredit market is functioning. For more information, click here.

Senate Committee on Banking held a full committee hearing, titled “Oversight of the Credit Reporting Agencies.” Chairman Sherrod Brown (D-OH) described consumercredit reports as “riddled with errors.” Brown argued that medical debt “correlates with illness,” not with credit risk. On April 27, the U.S.

In June 2020, the CFPB proposed amendments to Regulation Z to address the anticipated expiration of the London Inter-Bank Offered Rate (LIBOR)—a commonly-used index for calculating the interest rate on variable-rate consumercredit products. The Bureau expects to issue a final rule in January 2022.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. The eviction moratorium law is part of New York state’s COVID-19 Emergency Eviction and Foreclosure Prevention Act of 2020.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. Please click here to visit this new interactive tool: [link]. For more information, click here.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. In reviewing the market for potential consumer harm, the report presents the latest research on consumer card use, cost, and availability.

Is there a Credco credit inquiry on your credit report? Credco is an unfamiliar name to most consumers, but that doesn’t mean it isn’t legit. Short for CoreLogic Credco, it is a consumercredit reporting company. These companies can assist you with a range of credit problems, such as: Bankruptcies.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. You may access this interactive tool at [link].

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. House of Representatives that seeks to amend the Fair Credit Reporting Act to exclude COVID-19-related evictions from consumers’ credit reports.

Our bank and loan servicing clients also face novel challenges affecting their industry due to COVID-19, particularly the ever-changing rules and regulations concerning evictions and foreclosures. On June 30, the CFPB released a blog post regarding trends of commercial reporting on consumercredit.

On August 27, 2020, the Federal Housing Finance Agency announces it would extend the eviction moratoriums on single-family foreclosures and real estate owned (REO) properties from August 31, 2020 to December 31, 2020. The moratorium only applies to Enterprise-backed, single-family mortgages. For more information, click here.

We organize all of the trending information in your field so you don't have to. Join 19,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content